North Avoca is a relaxed coastal suburb on the Central Coast of New South Wales, known for its leafy streets, beachside lifestyle, and a strong mix of classic Australian homes. It's also a suburb where home insurance premiums can vary significantly — making it well worth understanding exactly what drives your quote before you sign on the dotted line.

In this article, we break down a real home and contents insurance quote for a 3-bedroom, 1-bathroom free standing home in North Avoca (postcode 2260), comparing it against suburb, state, and national benchmarks to help you make a more informed decision.

---

Is This Quote Fair?

The annual premium for this property came in at $3,918 per year (or $375/month), covering a building sum insured of $444,000 and $50,000 worth of contents. Both the building and contents excess are set at $2,000.

Our price rating for this quote is FAIR — Around Average.

When stacked against the 18 quotes we've collected for the North Avoca area, this premium sits comfortably between the suburb's 25th percentile ($3,784/yr) and the 75th percentile ($5,374/yr). In other words, it's not the cheapest quote available in the suburb, but it's far from the most expensive either. Homeowners who've been quoted above $5,374 are likely paying a meaningful premium above what's typical for the area.

A "Fair" rating means you're in reasonable territory — but there's still room to shop around, particularly if you can adjust your excess, review your sum insured, or bundle additional features.

---

How North Avoca Compares

Understanding your quote in isolation only tells part of the story. Here's how North Avoca sits relative to broader benchmarks:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| North Avoca (2260) | $4,586/yr | $4,547/yr |

| NSW | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

| Central Coast LGA | $8,387/yr | — |

A few things stand out here. The NSW state average of $9,528 looks alarming at first glance, but the median of $3,770 tells a more grounded story — a small number of very high-risk or high-value properties are pulling the average upward significantly. The same pattern holds nationally, where the average ($5,347) is nearly double the median ($2,764).

For North Avoca specifically, the suburb average and median are closely aligned at around $4,547–$4,586, which suggests a relatively consistent risk profile across the area — without the extreme outliers seen at the state level.

At $3,918, this quote sits below the North Avoca suburb average, which is a positive sign. You can explore more suburb-level data on our North Avoca insurance stats page, or compare against NSW state-wide figures and national benchmarks.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on how insurers price the risk. Here's what's most relevant:

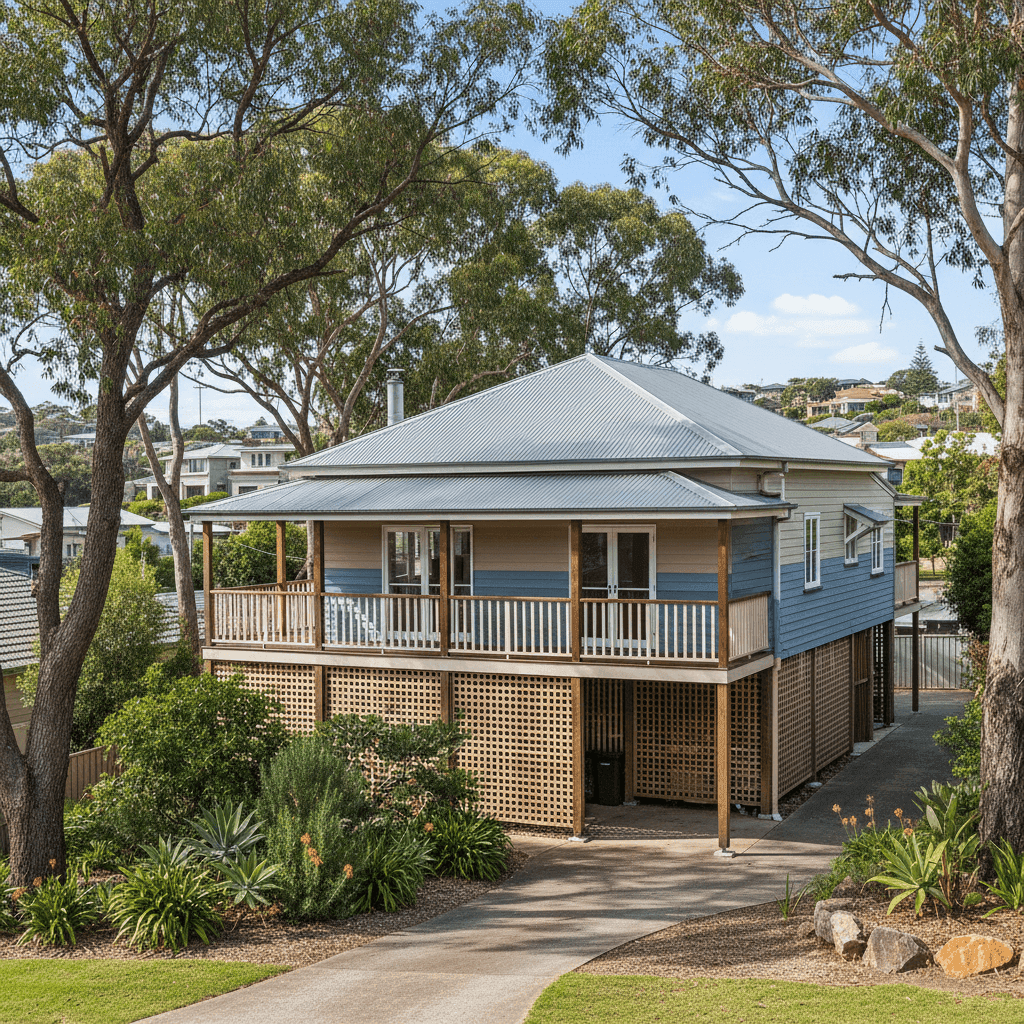

Weatherboard Timber Walls

Weatherboard construction is common in older Australian homes and carries a higher fire risk than brick or rendered masonry. Insurers typically price this in, as timber is more susceptible to fire spread and can be more costly to repair or replace after storm or impact damage.

Steel / Colorbond Roof

On the positive side, a Colorbond steel roof is generally viewed favourably by insurers. It's durable, low-maintenance, and performs well in high-wind conditions — all of which can help moderate your premium compared to older roofing materials like terracotta tiles or asbestos sheeting.

Elevated on Poles (At Least 1 Metre)

This is a significant factor. Homes elevated by at least one metre on poles — a classic Queenslander-style design — are more exposed to wind uplift, and the subfloor structure introduces additional complexity in the event of storm or flood damage. However, elevation can also reduce flood inundation risk in low-lying areas, so the net effect depends on the specific site.

1987 Construction

A home built in 1987 sits in a middle ground — old enough to potentially have ageing materials and systems, but recent enough to have been built under more modern building codes than pre-1970s homes. Insurers may factor in the age of the roof, plumbing, and electrical systems.

Ducted Climate Control

The presence of ducted climate control adds to the replacement value of the home's fixtures and fittings, which is reflected in the building sum insured. It's worth ensuring your $444,000 sum insured adequately accounts for the cost of reinstating this system.

Standard Fittings Quality

Standard fittings (as opposed to premium or high-end) generally keep premiums more moderate, as the cost to repair or replace fixtures is lower than for prestige finishes.

---

Tips for Homeowners in North Avoca

1. Review Your Building Sum Insured Annually

Construction costs on the Central Coast have risen sharply in recent years. A sum insured of $444,000 for a 105 sqm weatherboard home on poles may be adequate today, but it's worth recalculating each year using an independent building cost estimator. Being underinsured at claim time can leave you significantly out of pocket.

2. Consider a Higher Excess to Reduce Your Premium

Both the building and contents excess on this policy are set at $2,000. If you have the financial buffer to absorb a higher out-of-pocket cost in the event of a claim, increasing your excess to $3,000 or $5,000 could noticeably reduce your annual premium.

3. Don't Overlook Maintenance of Your Elevated Structure

Insurers can decline or reduce claims where damage is attributable to poor maintenance. For a home on poles, this means regularly inspecting the subfloor stumps, bearers, and joists for rot, pest damage, or structural movement. Keeping records of maintenance can also support your position if a claim is ever disputed.

4. Shop Around at Renewal

Insurance loyalty rarely pays. Insurers frequently offer their best rates to new customers, meaning long-standing policyholders can end up paying above-market premiums. Use a comparison tool like CoverClub to benchmark your renewal quote each year — it only takes a few minutes and could save you hundreds.

---

Compare Your Quote Today

Whether you're a first-time buyer in North Avoca or you've owned your home for decades, it pays to know where your premium sits relative to the market. CoverClub makes it easy to compare home and contents insurance quotes in one place, with real data from your suburb to help you judge whether you're getting a fair deal.