North Mackay is a well-established residential suburb sitting on the northern fringe of Mackay, in Queensland's tropical north. Homes here tend to be a mix of older character properties and more modern builds — and insuring them comes with its own set of considerations, particularly given the region's exposure to severe weather. This article takes a close look at a home and contents insurance quote for a 3-bedroom, free-standing home in North Mackay (postcode 4740), breaks down whether the premium is competitive, and offers practical advice for local homeowners looking to get better value from their cover.

---

Is This Quote Fair?

The quote in question comes in at $5,184 per year (or $497 per month) for combined home and contents insurance, with a building sum insured of $445,000 and contents valued at $50,000. The building excess sits at $2,000 and the contents excess at $1,000.

Based on our pricing data, this quote is rated Expensive — above average for the North Mackay area. Here's the context:

- The suburb average premium in North Mackay is $3,682/yr, and the median is $3,407/yr

- This quote is approximately 41% above the suburb average and 52% above the suburb median

- It falls above the 75th percentile for the suburb ($4,820/yr), meaning it's pricier than roughly three-quarters of comparable quotes in the area

That said, "expensive" doesn't necessarily mean unjustified. Several property-specific factors — which we'll explore below — can legitimately push premiums higher. The key question is whether this particular property's risk profile warrants the additional cost, or whether shopping around could yield meaningful savings.

---

How North Mackay Compares

To put this quote in broader perspective, it helps to look at suburb-level data for North Mackay, Queensland-wide figures, and national benchmarks.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| North Mackay (suburb) | $3,682/yr | $3,407/yr |

| Mackay LGA | $8,458/yr | — |

| Queensland (state) | $9,129/yr | $3,903/yr |

| Australia (national) | $5,347/yr | $2,764/yr |

A few things stand out here. The Mackay LGA average of $8,458/yr is dramatically higher than the suburb average — this is likely driven by high-risk properties in flood-prone or cyclone-exposed pockets of the region pulling the average up. The Queensland state average of $9,129/yr is similarly elevated, reflecting the significant weather risk across much of the state.

Interestingly, the quote of $5,184/yr sits below both the LGA and state averages, which suggests it's not wildly out of line for the broader region — even if it's above the North Mackay suburb median. Compared to the national average of $5,347/yr, this quote is actually slightly below par, which provides some reassurance that the pricing isn't completely out of step with broader market conditions.

The suburb sample size of 94 quotes gives us a reasonably solid basis for comparison, though individual property characteristics can still cause significant variation.

---

Property Features That Affect Your Premium

Several aspects of this property are worth examining through the lens of insurance risk:

Cyclone Risk Area

This is arguably the most significant factor. North Mackay sits within a designated cyclone risk zone, and insurers price this in heavily. Cyclone cover typically adds a substantial loading to premiums — and in some cases, a separate cyclone excess applies on top of the standard excess. Homeowners should confirm whether their policy includes cyclone damage and what the specific excess conditions are.

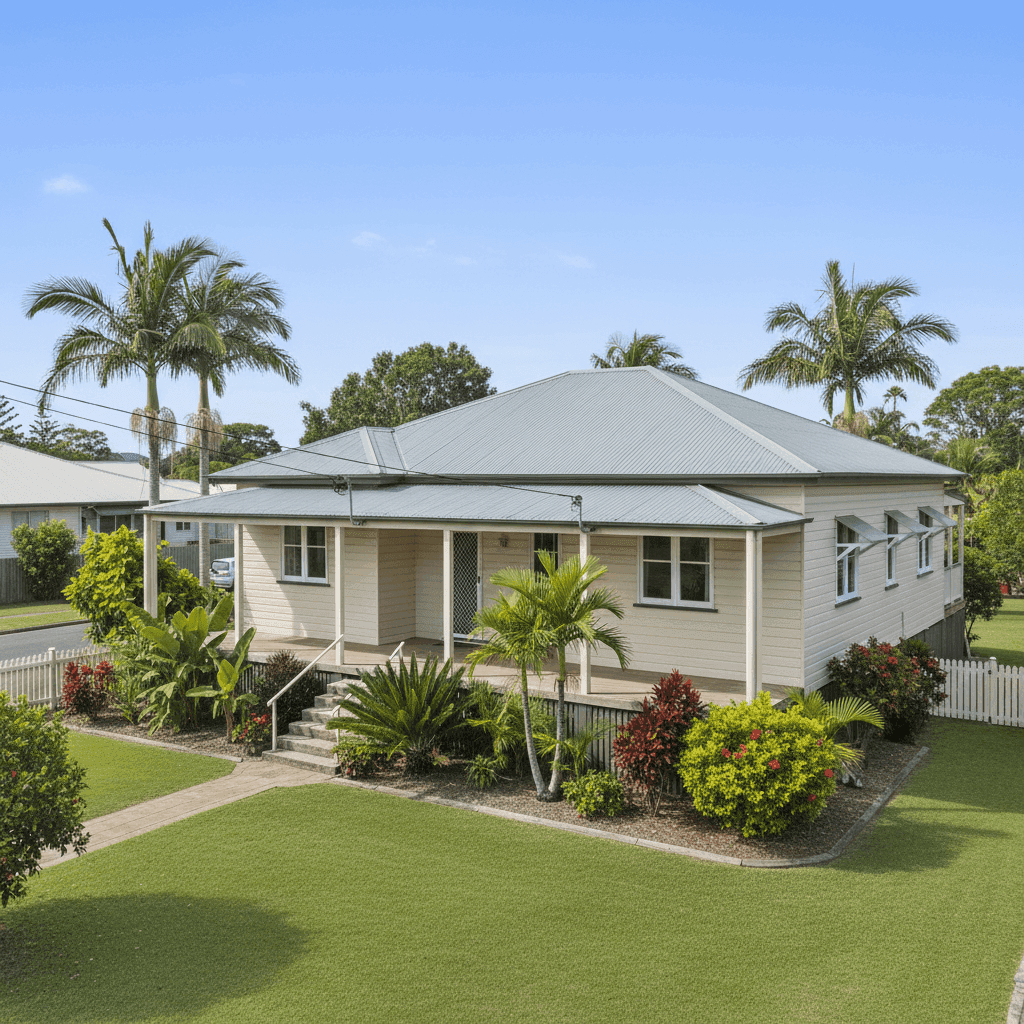

Weatherboard Timber Walls

External walls constructed from weatherboard timber are generally considered higher risk by insurers compared to brick or rendered masonry. Timber is more susceptible to fire, termite damage, and deterioration over time — all of which factor into underwriting decisions. Older weatherboard homes in cyclone-prone areas can attract notable premium loadings.

Age of Construction (1966)

At nearly 60 years old, this property pre-dates many modern building codes, including those introduced after major cyclone events. Older homes may have less robust structural connections (such as roof-to-wall tie-downs) and may use materials that are harder or more expensive to source and replace. This age factor can meaningfully influence both the sum insured and the premium.

Steel/Colorbond Roof

On the positive side, a steel Colorbond roof is generally well-regarded by insurers. It's durable, fire-resistant, and performs reasonably well in high-wind conditions compared to older roofing materials like fibrous cement or terracotta tiles. This may help moderate the premium slightly.

Slab Foundation & Timber/Laminate Flooring

A concrete slab foundation is a neutral-to-positive risk factor. However, combined with timber or laminate flooring, there is some exposure to damage from water ingress — particularly relevant in a region prone to heavy rainfall and storm surge. Homeowners should check whether their policy covers gradual water damage versus sudden storm-related flooding.

Building Size & Sum Insured

At 130 sqm with a building sum insured of $445,000, the per-square-metre replacement cost works out to approximately $3,423/sqm — which is on the higher end but not unreasonable for a regional Queensland market with elevated construction costs and the complexities of an older weatherboard build.

---

Tips for Homeowners in North Mackay

1. Review Your Cyclone Excess Carefully

Many policies in cyclone-prone areas apply a separate, higher excess for cyclone-related claims — sometimes 1–2% of the sum insured, which on a $445,000 building could mean an out-of-pocket cost of $4,450–$8,900. Make sure you understand this before selecting a policy, and factor it into your comparison.

2. Consider Increasing Your Excess to Lower Your Premium

The current building excess of $2,000 is moderate. Opting for a higher excess (say, $3,000–$5,000) can reduce your annual premium noticeably. This strategy works well if you have an emergency fund to cover a larger excess in the event of a claim.

3. Get Multiple Quotes — Especially for Older Timber Homes

Insurers vary significantly in how they price weatherboard construction and older homes. Some specialise in heritage or character properties and may offer more competitive rates. Using a comparison platform like CoverClub to run multiple quotes simultaneously is one of the most effective ways to find a better deal without sacrificing cover quality.

4. Assess Whether Your Sum Insured Is Accurate

Over-insurance is a common and costly mistake. If the $445,000 building sum insured is higher than what it would actually cost to rebuild the home (accounting for demolition, materials, and labour at current rates), you may be paying more than necessary. A quantity surveyor or online building cost calculator can help you arrive at a more accurate figure.

---

Compare Your Options with CoverClub

Whether you're renewing your existing policy or shopping for cover for the first time, it pays to compare. CoverClub makes it easy for Australian homeowners to benchmark their premiums against real local data and get quotes from multiple insurers in one place. Start your comparison today and see whether you can do better than the current market rate for your North Mackay home.