Nudgee is a well-established suburb in Brisbane's north, sitting roughly 13 kilometres from the CBD and bordered by the Nudgee Beach wetlands. It's a popular choice for families looking for a quiet, leafy lifestyle with easy access to the airport and major motorways. For owners of a free-standing home in this area, understanding what drives your home and contents insurance premium — and whether you're paying a fair price — is an important part of managing household finances.

This article breaks down a recent home and contents insurance quote for a four-bedroom, two-bathroom brick veneer home in Nudgee (postcode 4014), compares it against local, state, and national benchmarks, and offers practical tips to help you get the best value cover.

---

Is This Quote Fair?

The quote in question comes in at $3,082 per year (or $301 per month) for combined home and contents cover, with a building sum insured of $1,000,000 and contents valued at $145,000. Both the building and contents excess are set at $500.

Our price rating for this quote is FAIR — Around Average. That might sound underwhelming at first glance, but context matters enormously here. When you stack this premium against what others in Nudgee are actually paying, the picture becomes quite positive.

The suburb average for Nudgee sits at $6,375 per year, with a median of $5,535. This quote at $3,082 comes in well below both figures — meaning the homeowner is paying significantly less than most of their neighbours for comparable cover. It also sits comfortably above the 25th percentile of $2,335, which suggests the pricing is competitive without being suspiciously cheap.

In short, "around average" at a national level actually translates to a genuinely good outcome locally.

---

How Nudgee Compares

To fully appreciate this quote, it helps to see how Nudgee's insurance costs sit within the broader landscape.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Nudgee (4014) | $6,375/yr | $5,535/yr |

| Brisbane LGA | $4,485/yr | — |

| Queensland | $4,547/yr | $3,931/yr |

| National | $2,965/yr | $2,716/yr |

A few things stand out immediately. Nudgee's average premium of $6,375 is substantially higher than both the Queensland state average of $4,547 and the national average of $2,965. This reflects the elevated risk profile that insurers assign to many Brisbane-area suburbs — factors like proximity to waterways, storm and flood exposure, and the general cost of rebuilding in South East Queensland all push premiums upward.

The wide spread between Nudgee's 25th percentile ($2,335) and 75th percentile ($9,567) is also telling. It suggests a significant variation in what homeowners are paying, likely driven by differences in sum insured, cover type, individual risk factors, and the insurer chosen. This kind of spread underscores why comparing quotes is so valuable — the difference between the cheapest and most expensive options in this suburb can be enormous.

At $3,082, this quote sits below the Brisbane LGA average, below the Queensland state average, and only modestly above the national average — a strong result for a suburb where premiums can run very high.

---

Property Features That Affect Your Premium

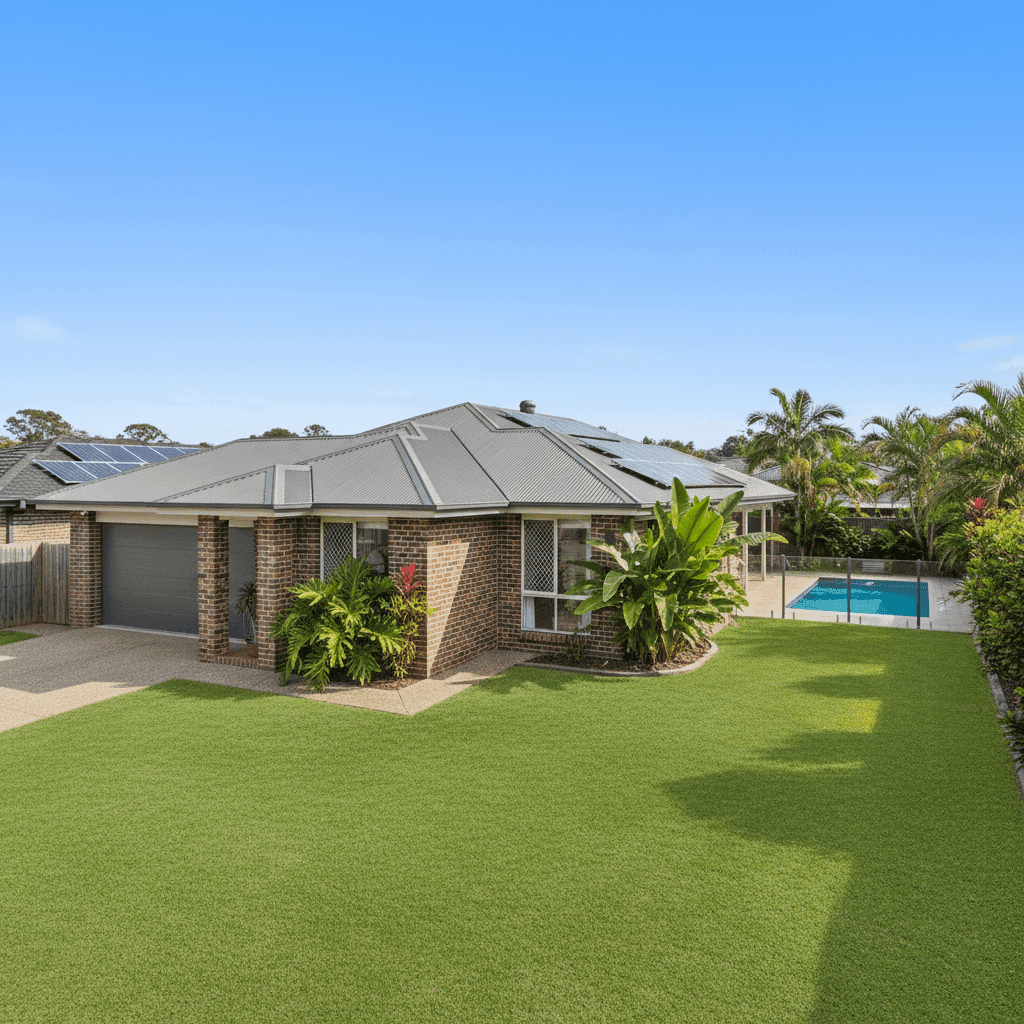

Several characteristics of this property have a direct bearing on the premium calculated.

Brick veneer construction is generally viewed favourably by insurers. It offers solid structural integrity and good fire resistance compared to timber-framed weatherboard homes, which can contribute to more competitive building premiums.

Colorbond steel roofing is another positive signal. It's durable, low-maintenance, and performs well in storms — a key consideration in Queensland where severe weather events are common. Insurers tend to price Colorbond roofs more competitively than older tile roofs, which can crack and leak.

Slab foundation reduces the risk of subsidence and pest-related structural damage compared to raised or suspended floors, which is another factor that can keep premiums in check.

Timber and laminate flooring does carry some considerations — these materials can be more susceptible to water damage than tiles, which may marginally influence contents and building claims risk. However, the impact on premium is typically modest.

Solar panels add value to the property but also represent an insurable asset. Homeowners should confirm with their insurer whether panels are covered under the building sum insured or require separate listing, as this varies between policies.

The swimming pool is a notable feature. Pools can increase liability exposure and may add to the overall sum insured for the building. It's worth reviewing your policy to ensure the pool, fencing, and associated equipment (pumps, filters, heating) are adequately covered.

The 214 sqm building size and standard fittings quality keep the rebuild cost estimate reasonable, which is reflected in the $1,000,000 sum insured — a figure that provides a solid buffer for a modern Brisbane home without excessive over-insurance.

---

Tips for Homeowners in Nudgee

1. Review your sum insured annually Construction costs in South East Queensland have risen significantly over recent years. The $1,000,000 building sum insured on this quote is a healthy figure, but it's worth using a building cost calculator each year to ensure your cover keeps pace with actual rebuild costs. Being underinsured at claim time can be a costly mistake.

2. Confirm solar panel and pool coverage As noted above, these features need to be explicitly accounted for in your policy. Ask your insurer directly whether your solar system is included in the building sum insured and whether the pool structure and equipment are covered. If not, you may need to adjust your sum insured or add specific items.

3. Compare quotes before renewal The wide premium range in Nudgee — from $2,335 at the 25th percentile to $9,567 at the 75th — shows that insurers price this suburb very differently. Don't simply auto-renew each year. Running a fresh comparison at CoverClub takes only a few minutes and could save you thousands.

4. Consider your excess level strategically Both excesses on this policy are set at $500, which is fairly standard. Opting for a higher excess (say, $1,000 or $2,000) can meaningfully reduce your annual premium. If you have a solid emergency fund and are unlikely to make small claims, a higher excess is often a smart trade-off.

---

Compare Your Home Insurance Today

Whether you're a long-time Nudgee resident or new to the area, it pays to make sure you're getting competitive cover at a fair price. CoverClub makes it easy to compare home and contents insurance quotes from multiple insurers in minutes — all tailored to your specific property and circumstances.

Get your personalised quote at CoverClub and see how your current premium stacks up against the market. You might be surprised at what's available.