If you own a free standing home in Nyngan, NSW 2825, you already know that insuring a property in regional New South Wales comes with its own set of considerations — from older construction materials to the realities of rural living. This article breaks down a real home and contents insurance quote for a three-bedroom, one-bathroom home in Nyngan, examines whether it represents fair value, and offers practical guidance for local homeowners looking to make the most of their cover.

---

Is This Quote Fair?

The quote in question comes in at $10,538 per year (or $1,010/month) for combined home and contents insurance, covering a building sum insured of $652,000 and $50,000 in contents. Both the building and contents excess are set at $2,000.

Our price rating for this quote is EXPENSIVE — above average. That assessment is backed up by the numbers: the suburb average for Nyngan sits at $9,014/yr, and the suburb median is $9,152/yr. This quote lands above the 75th percentile for the area ($10,332/yr), meaning it's pricier than at least three-quarters of comparable quotes we've seen in the postcode.

That said, "expensive" doesn't automatically mean "wrong." Several property-specific factors — which we'll explore below — can legitimately push a premium higher. The key question is whether those factors fully justify the gap, or whether there's room to shop around.

---

How Nyngan Compares

To put this quote in proper context, it helps to zoom out and look at the broader insurance landscape. You can explore full benchmark data on the Nyngan suburb stats page, the NSW state stats page, and national insurance stats.

| Benchmark | Average Premium |

|---|---|

| Nyngan (suburb average) | $9,014/yr |

| Nyngan (suburb median) | $9,152/yr |

| Nyngan (25th percentile) | $7,821/yr |

| Nyngan (75th percentile) | $10,332/yr |

| LGA — Warren | $6,331/yr |

| NSW state average | $9,528/yr |

| NSW state median | $3,770/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

A few things stand out here. First, Nyngan's suburb average of $9,014/yr is notably higher than both the NSW state median ($3,770/yr) and the national median ($2,764/yr). This tells us that insuring a home in Nyngan is genuinely more expensive than in many other parts of the country — it's not just this one quote that's elevated. Regional NSW properties, particularly older homes, tend to attract higher premiums due to rebuild costs, limited local trades, and specific risk profiles.

Second, the LGA average for Warren ($6,331/yr) is considerably lower than Nyngan's suburb average, which suggests that even within the same local government area, premiums can vary significantly depending on the specific postcode and property characteristics.

This quote, at $10,538/yr, sits above the suburb's 75th percentile — so while Nyngan is broadly an expensive area to insure, this particular quote is on the higher end even by local standards.

---

Property Features That Affect Your Premium

Several characteristics of this property are worth examining closely, as they each have a meaningful influence on what insurers charge.

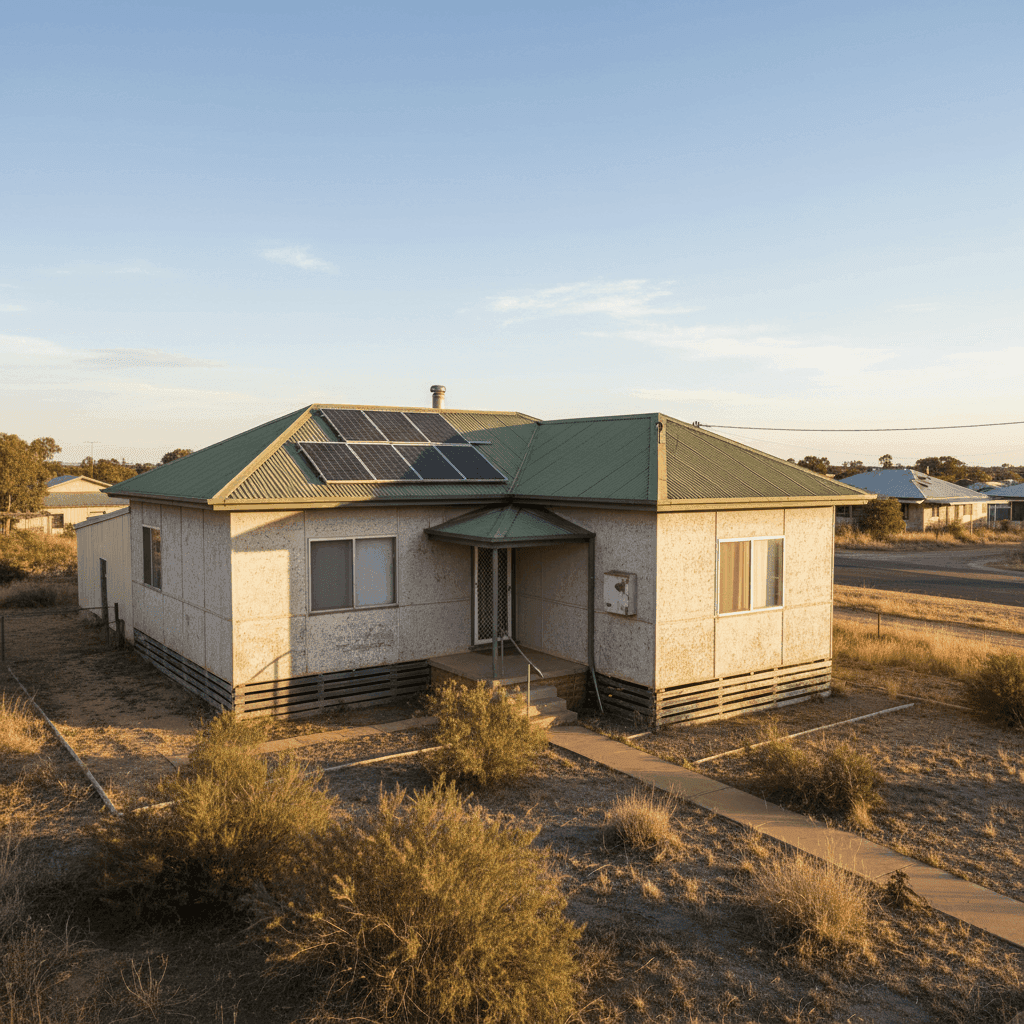

Fibro Asbestos External Walls

This is arguably the single biggest premium driver for this property. Homes with fibro asbestos (fibrous cement sheeting containing asbestos) are significantly more expensive to insure because any repair or rebuild work must comply with strict asbestos handling and disposal regulations. Licensed contractors, specialised equipment, and regulatory compliance all add substantially to rebuild costs — and insurers price accordingly.

Age of Construction (1969)

Built in 1969, this home is over 55 years old. Older homes tend to have ageing plumbing, wiring, and structural elements that increase the likelihood of a claim. They also often require non-standard materials or techniques to repair, which can push up the cost of any work carried out.

Stump Foundation

Homes on stumps (also called pier or post foundations) can be more vulnerable to certain types of damage, including subsidence, pest ingress, and flooding underneath the structure. Insurers factor this into their risk assessment, particularly in regional areas where soil conditions and drainage can vary.

Timber/Laminate Flooring

Timber floors — especially in older homes on stumps — can be susceptible to moisture damage, warping, and termite activity. This adds a layer of risk that insurers consider when calculating premiums.

Solar Panels

This property has solar panels installed, which adds to the overall replacement cost of the building and can slightly increase premiums. On the upside, some insurers view solar panels positively as a sign of a well-maintained, modern-minded property.

Ducted Climate Control

Ducted air conditioning systems are expensive to replace and can be a source of claims (e.g., electrical faults, storm damage). Their presence typically increases the building sum insured and, by extension, the premium.

Building Sum Insured: $652,000

The sum insured of $652,000 is relatively high for a 130 sqm home in regional NSW, but it's important to remember that sum insured reflects the cost to rebuild, not the market value of the property. Given the fibro asbestos construction and the associated remediation costs, a higher sum insured is arguably prudent here.

---

Tips for Homeowners in Nyngan

1. Get Multiple Quotes — Every Year

With a premium above the local 75th percentile, this is a clear case where shopping around could pay dividends. Insurers price risk differently, and a quote that's expensive with one provider may be quite competitive with another. Use CoverClub's quote comparison tool to see what else is available for your property.

2. Review Your Sum Insured Carefully

Make sure your building sum insured accurately reflects the cost to rebuild — including demolition, asbestos removal, and professional fees. Being underinsured can leave you seriously out of pocket after a major claim, but being significantly overinsured means you're paying more than necessary. Consider getting a professional building valuation to find the right number.

3. Ask About Asbestos-Specific Cover

Not all policies treat asbestos removal costs the same way. When comparing quotes, ask insurers directly how they handle asbestos-containing materials in a claim scenario — specifically whether removal and disposal costs are included in the building sum insured or treated separately. This can make a significant difference to your actual cover.

4. Consider Increasing Your Excess

Both the building and contents excess on this policy are set at $2,000. If you have the financial capacity to absorb a higher excess in the event of a claim, increasing this amount can reduce your annual premium. Just make sure the saving is meaningful before making the switch.

---

Compare Your Options with CoverClub

Whether this quote is the right fit depends on your full circumstances — but one thing is clear: at above the 75th percentile for Nyngan, it's worth exploring your options. At CoverClub, you can compare home and contents insurance quotes for your Nyngan property in minutes, with full transparency on pricing and cover details. Don't pay more than you need to — start comparing today.