If you own a free standing home in Oakdale, NSW 2570, you already know the appeal — a semi-rural lifestyle on the south-western fringe of Greater Sydney, with the green hills of the Wollondilly region as your backdrop. But with that lifestyle comes the practical reality of protecting your most valuable asset. Home and contents insurance is one of those non-negotiables, and understanding whether you're paying a fair price can save you hundreds of dollars a year.

In this article, we analyse a real home and contents insurance quote for a 5-bedroom, 2-bathroom free standing home in Oakdale — and break down exactly what's driving the premium.

---

Is This Quote Fair?

The quote in question comes in at $4,406 per year (or $415 per month) for a combined home and contents policy. The building is insured for $1,300,000, with $100,000 in contents cover. Both the building and contents carry a $2,000 excess.

Our price rating for this quote is FAIR — Around Average.

That assessment holds up when you dig into the data. The suburb median premium in Oakdale sits at $3,681 per year, meaning this quote is modestly above the midpoint for the area — but well within the normal range. The suburb's 75th percentile is $6,869 per year, so there's a significant portion of Oakdale homeowners paying considerably more. At $4,406, this policy sits comfortably between the median and the upper quartile, which is a reasonable position given the property's size, features, and sum insured.

It's also worth noting that the $1,300,000 building sum insured is a substantial figure — higher coverage naturally pushes premiums upward, so comparing on price alone without accounting for coverage level can be misleading.

---

How Oakdale Compares

Context is everything when evaluating an insurance premium. Here's how this quote stacks up across different benchmarks:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Oakdale (2570) | $6,127/yr | $3,681/yr |

| NSW | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

| Wollondilly LGA | $2,297/yr | — |

A few things stand out here. The NSW state average of $9,528 per year is dramatically higher than the median of $3,770 — a classic sign that a small number of very expensive policies (likely in high-risk flood, bushfire, or coastal areas) are pulling the average upward. The same dynamic plays out nationally, where the national average of $5,347 is nearly double the national median of $2,764.

For Oakdale specifically, the suburb-level data tells a similar story — the local average of $6,127 is skewed by outlier premiums, while the median of $3,681 gives a more grounded picture of what most homeowners are actually paying.

Interestingly, the Wollondilly LGA average of $2,297 is notably lower than the Oakdale suburb average. This suggests that Oakdale properties — perhaps due to specific risk factors like localised flooding or bushfire proximity — may attract slightly higher premiums than other parts of the wider LGA.

At $4,406, this quote beats the NSW average by a wide margin and sits only modestly above the suburb median, making it a competitive outcome for a well-featured property.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on what insurers charge. Understanding them helps you anticipate costs and potentially negotiate better terms.

Brick Veneer Walls & Colorbond Roof

Brick veneer construction is generally viewed favourably by insurers — it's durable, fire-resistant, and relatively low-maintenance compared to weatherboard or cladding. A steel Colorbond roof is similarly well-regarded; it's resistant to embers, handles heavy rain well, and has a long lifespan. Together, these materials typically attract more competitive premiums than timber-framed or older tiled roofs.

Slab Foundation

A concrete slab foundation is standard in this era of construction (the home was built in 1980) and presents minimal risk of subsidence or termite ingress via the subfloor — both of which can be costly concerns for insurers. This is a positive factor for pricing.

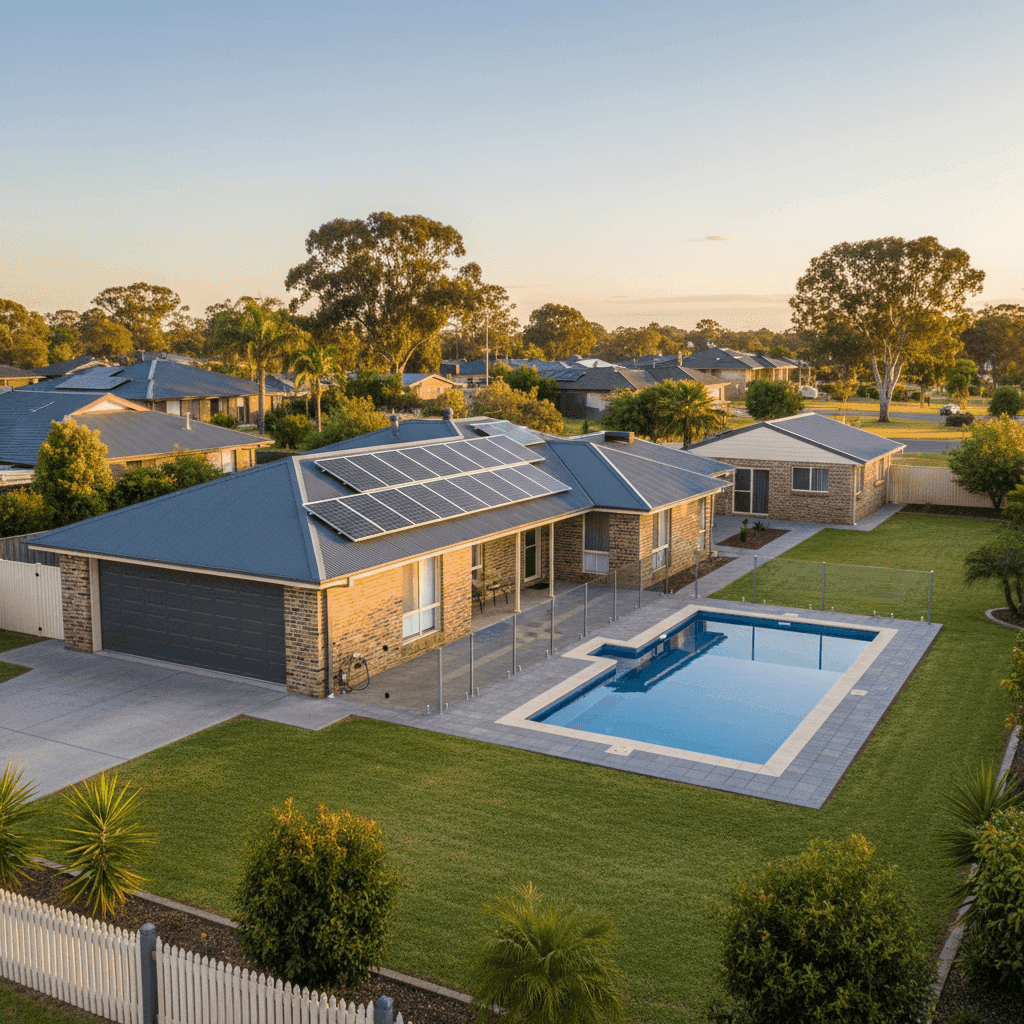

Pool, Solar Panels & Ducted Climate Control

These three features add real value to the property but also increase the replacement cost and complexity of a claim. A swimming pool adds liability exposure and increases the building sum insured. Solar panels — particularly older systems — can be expensive to replace and may require specialist labour. Ducted climate control is a significant fixed installation that adds to rebuilding costs. All three contribute to the higher-than-median sum insured of $1.3 million and are reflected in the premium.

Granny Flat

The presence of a granny flat on the property meaningfully increases the insurable value of the building. Whether it's used for extended family, as a rental, or simply as extra space, it adds floor area, fixtures, and infrastructure that must be covered in the event of a total loss. This is a key driver of the elevated building sum insured.

Vinyl Flooring & Standard Fittings

Vinyl flooring and standard-grade fittings keep replacement costs more predictable than premium finishes like hardwood floors or stone benchtops. This helps moderate the contents and building valuation somewhat, even for a larger home.

Property Age

At over 40 years old, the home predates modern building codes in several respects. Insurers factor in the age of a property when assessing risk — older homes can have ageing plumbing, electrical systems, and structural elements that increase the likelihood of claims. This is a modest upward pressure on premiums.

---

Tips for Homeowners in Oakdale

1. Review your building sum insured carefully A $1,300,000 sum insured is substantial, and while it's important not to be underinsured, over-insuring also costs money. Use a professional building cost estimator or engage a quantity surveyor to confirm your rebuild cost — especially given the granny flat and additional features. Many insurers offer online calculators as a starting point.

2. Ask about bundling discounts Combining home and contents under a single policy (as this quote does) often attracts a discount. If your current insurer doesn't offer one, it's worth asking — or shopping around with platforms like CoverClub to find policies that reward bundling.

3. Consider a higher excess to reduce your premium The current excess is set at $2,000 for both building and contents. If you have the financial buffer to absorb a higher out-of-pocket cost in a claim, increasing the excess to $3,000 or $5,000 can noticeably reduce your annual premium. Just make sure the savings justify the added risk exposure.

4. Document your contents thoroughly With $100,000 in contents cover, it's essential to have an up-to-date home inventory. Photograph valuables, keep receipts where possible, and store a copy of your inventory off-site or in the cloud. This makes claims faster and reduces the risk of disputes over item values.

---

Compare Quotes and Find a Better Deal

Whether you're renewing your policy or shopping for the first time, comparing multiple quotes is the single most effective way to ensure you're not overpaying. Premiums for the same property can vary by thousands of dollars between insurers — and the cheapest isn't always the best value once you factor in coverage limits, exclusions, and claim service.

Get a home insurance quote at CoverClub and see how your premium compares against real data from your suburb, your state, and across Australia. It takes minutes and could save you significantly.