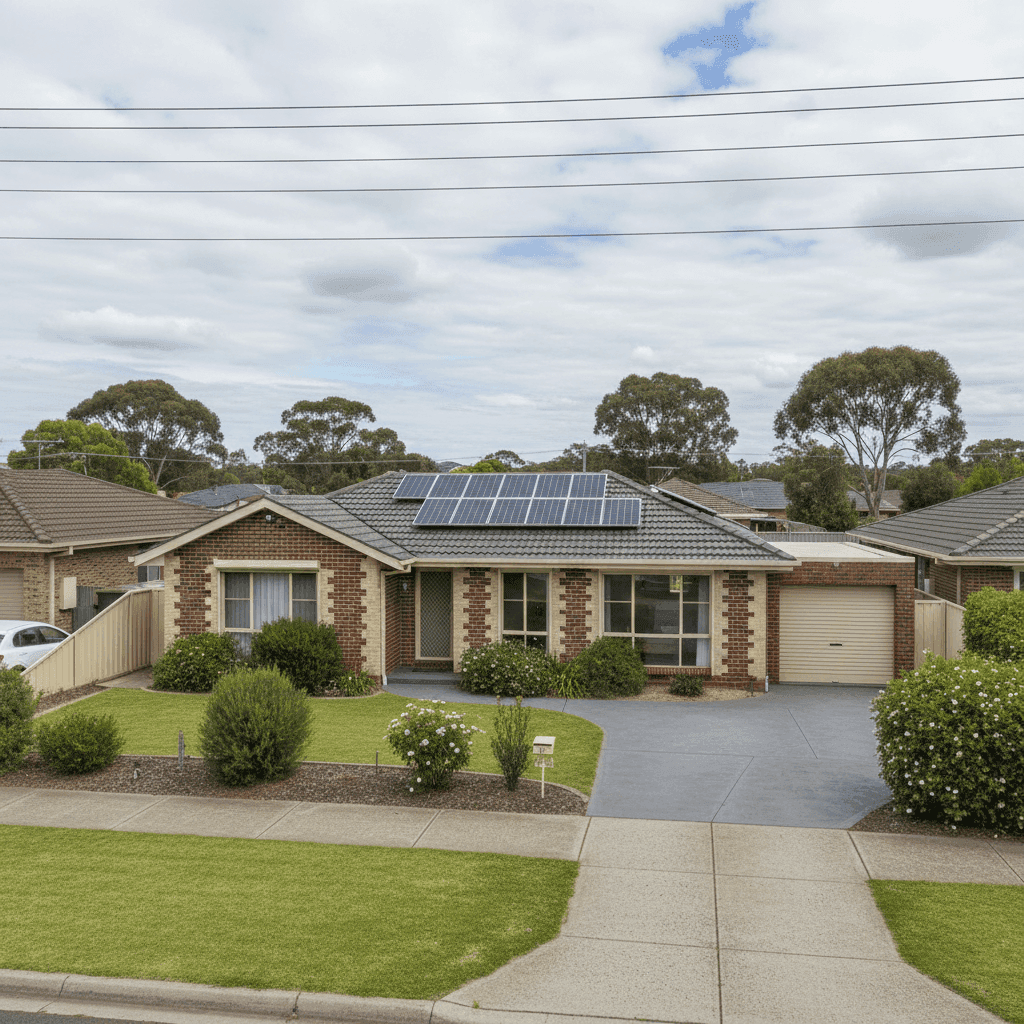

If you own a free standing home in Oakhurst, NSW 2761, you're likely paying close attention to the cost of home and contents insurance — especially as premiums across Australia continue to climb. This article breaks down a real insurance quote for a 3-bedroom, 1-bathroom brick veneer home in Oakhurst, compares it against local and national benchmarks, and offers practical tips to help you get better value on your cover.

---

Is This Quote Fair?

The quote in question comes in at $2,771 per year (or $266/month) for combined home and contents insurance, covering a building sum insured of $492,000 and contents valued at $250,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is Expensive — above average for the Oakhurst area.

To put that in perspective, the suburb average premium in Oakhurst sits at just $1,244 per year, with a median of $1,131. This quote is more than double the local median, which is a significant gap worth investigating before renewing or accepting any policy.

That said, context matters. The sum insured here is substantial — $492,000 for the building alone — and the contents cover of $250,000 is on the higher end for a standard 3-bedroom home. These figures will naturally push the premium upward compared to neighbours who may be insuring for less. Still, even accounting for coverage levels, there may be room to shop around.

---

How Oakhurst Compares

Understanding where Oakhurst sits in the broader insurance landscape helps you gauge whether a quote is reasonable or inflated.

| Benchmark | Premium |

|---|---|

| Oakhurst suburb average | $1,244/yr |

| Oakhurst suburb median | $1,131/yr |

| Oakhurst 25th percentile | $808/yr |

| Oakhurst 75th percentile | $1,636/yr |

| LGA (Blacktown) average | $2,242/yr |

| NSW state average | $9,528/yr |

| NSW state median | $3,770/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

Based on 22 quotes collected for the Oakhurst area.

A few things stand out here. First, Oakhurst is actually a relatively affordable suburb to insure compared to broader NSW benchmarks — the state median of $3,770 is more than three times the local suburb median. This suggests the area doesn't carry the same elevated risk profile as many other NSW postcodes, particularly those exposed to flooding, bushfire, or coastal hazards.

Second, the quote of $2,771 sits just above the national median of $2,764, meaning it's broadly in line with what Australians pay on average — but well above what most Oakhurst homeowners are actually paying.

For a deeper look at pricing trends in the area, visit our Oakhurst suburb stats page, or explore NSW-wide insurance data and national benchmarks for broader context.

---

Property Features That Affect Your Premium

Several characteristics of this property will influence how insurers calculate the premium. Here's how the key features come into play:

Brick Veneer Walls & Tiled Roof Brick veneer construction with a tiled roof is generally viewed favourably by insurers. It's a durable combination that offers solid fire resistance and structural integrity — common in Western Sydney homes built in the 1990s. This should, in theory, work in the homeowner's favour when it comes to pricing.

Built in 1995 A home approaching 30 years of age sits in a moderate risk bracket. It's old enough that some systems (electrical, plumbing, roofing) may be nearing the end of their serviceable life, but not so old as to attract the steep loadings often applied to pre-1970s homes. Insurers may factor in potential maintenance issues, particularly with the slab foundation and timber/laminate flooring.

Slab Foundation & Timber/Laminate Flooring Concrete slab foundations are standard for this era of construction and are generally considered low risk. However, timber and laminate flooring can be more susceptible to water damage than tiles, which some insurers may price into the contents or building premium — particularly if a burst pipe or internal flood event were to occur.

Solar Panels The presence of solar panels adds a layer of complexity to the building sum insured. Panels need to be covered for damage from storms, hail, and fire, and their replacement cost can be significant. Ensuring your building sum insured adequately accounts for solar panel replacement is important — and it's likely contributing to the higher-than-average premium here.

Ducted Climate Control Ducted air conditioning systems are a meaningful asset and, as a fixed building fixture, need to be included in the building sum insured. A full ducted system can cost $10,000–$20,000+ to replace, so it's right that it's factored into coverage — though it does add to the overall premium.

No Pool, No Cyclone Risk The absence of a pool removes a common liability loading, and Oakhurst falls outside designated cyclone risk zones — both factors that help keep the base premium more manageable.

---

Tips for Homeowners in Oakhurst

1. Review your sum insured carefully At $492,000, the building sum insured is on the higher end for a 130 sqm home in Western Sydney. Use a building cost calculator to verify this figure reflects actual rebuild costs — not market value. Overinsuring inflates your premium without adding real benefit.

2. Shop around with multiple insurers The gap between this quote ($2,771) and the suburb median ($1,131) is large enough to warrant getting at least two or three competing quotes. Insurers price risk differently, and the same property can attract very different premiums across providers. Compare quotes at CoverClub to see what else is available.

3. Consider your excess level Both the building and contents excess are set at $1,000. Opting for a higher excess — say $2,000 — can meaningfully reduce your annual premium. If you have an emergency fund in place and are unlikely to make small claims, this is often a smart trade-off.

4. Check your contents valuation $250,000 in contents cover is generous for a 3-bedroom home with standard fittings. Walk through each room and take stock of what you actually own. Many homeowners find they're overinsuring contents, which directly inflates the premium. An accurate valuation protects you without paying for cover you don't need.

---

Compare Your Options with CoverClub

Whether you're renewing your policy or shopping for the first time, it pays to compare. CoverClub makes it easy to see how your current quote stacks up against real data from your suburb and across Australia. Get a home insurance quote today and find out if you're paying more than you need to.