Ocean Grove is one of the Surf Coast's most sought-after residential addresses — a relaxed beachside town on Victoria's Bellarine Peninsula that draws families, retirees, and sea-changers alike. With that lifestyle appeal comes the practical reality of protecting your home, and for owners of a free-standing property in the area, understanding what you should be paying for home and contents insurance is an important part of managing household finances.

This article breaks down a recent insurance quote for a four-bedroom, one-bathroom free-standing home in Ocean Grove (VIC 3226), weighing it against local, state, and national benchmarks so you can make a more informed decision about your own cover.

---

Is This Quote Fair?

The quote in question sits at $2,539 per year (or $243 per month) for combined home and contents cover, with a building sum insured of $809,000 and contents valued at $90,000. Both the building and contents excess are set at $1,000.

Our pricing engine rates this quote as Fair — Around Average, and the data backs that up. The suburb average for Ocean Grove sits at $2,294 per year, meaning this quote is roughly $245 above the local average — a modest premium that likely reflects the specific characteristics of this property rather than any red flags with the insurer's pricing.

It's worth noting the difference between the suburb average and median. The median premium in Ocean Grove is $2,048 per year, which is noticeably lower than the average, suggesting a handful of higher-priced quotes are pulling the average upward. This quote falls between the 75th percentile ($2,822/yr) and the suburb average, placing it in the upper-middle range of what Ocean Grove homeowners are paying — not cheap, but certainly not an outlier.

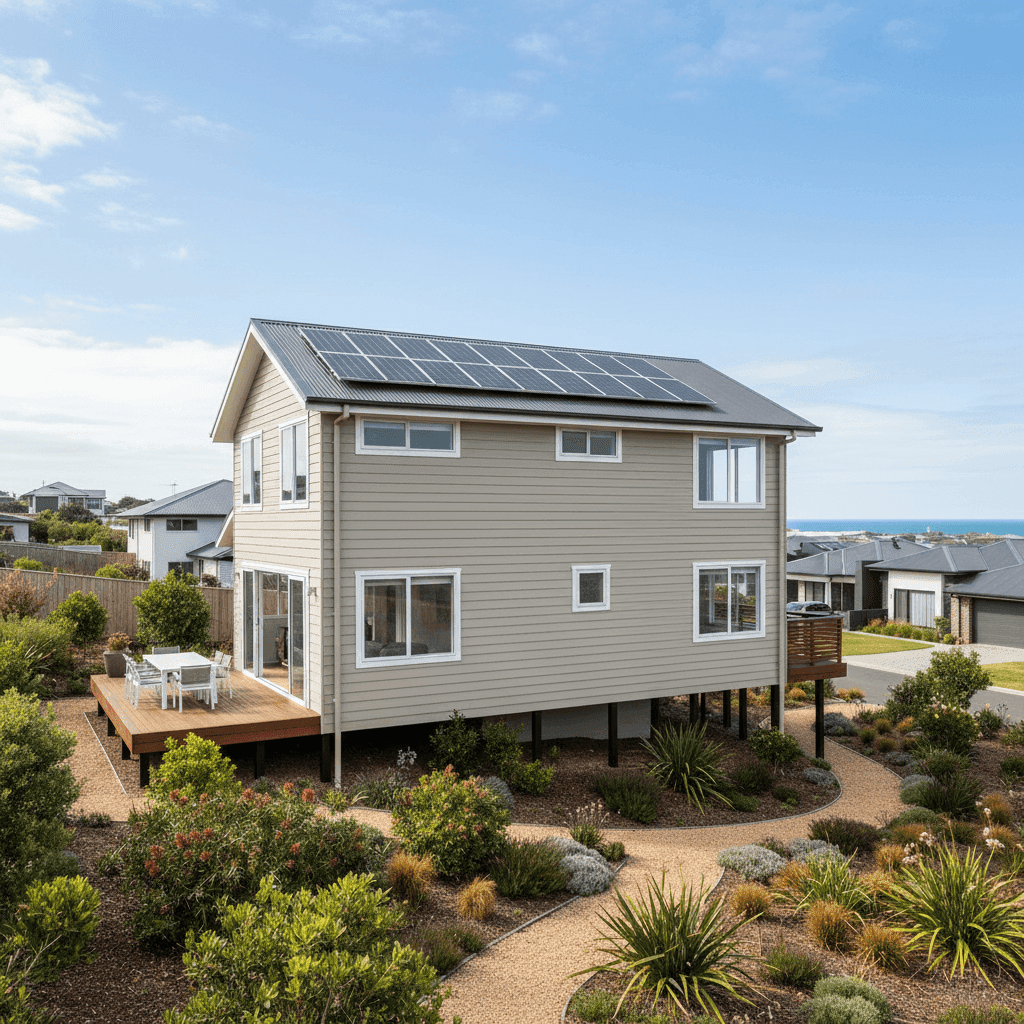

For a property of this size (205 sqm), age (built 1983), and with features like solar panels and ducted climate control, a premium in this range is reasonable. You can explore the full pricing landscape for this postcode at CoverClub's Ocean Grove suburb stats page.

---

How Ocean Grove Compares

Putting this quote in a broader context reveals just how well-priced Victorian coastal properties can be relative to the rest of the country.

| Benchmark | Annual Premium |

|---|---|

| This quote | $2,539 |

| Ocean Grove suburb average | $2,294 |

| Ocean Grove suburb median | $2,048 |

| Greater Geelong LGA average | $1,754 |

| VIC state average | $3,000 |

| VIC state median | $2,718 |

| National average | $5,347 |

| National median | $2,764 |

A few things stand out here. First, this quote is below the Victorian state average of $3,000 per year — good news for the homeowner. Second, the Greater Geelong LGA average of $1,754 is considerably lower, which likely reflects the mix of property types, sizes, and risk profiles across the broader LGA. Ocean Grove, as a coastal suburb, typically attracts slightly higher premiums than inland Geelong areas due to wind and weather exposure.

Perhaps most striking is the national average of $5,347 per year. This figure is heavily influenced by high-risk areas in Queensland, Western Australia, and the Northern Territory — regions prone to cyclones, flooding, and extreme weather events. By comparison, Ocean Grove homeowners are paying a fraction of what some Australians face. Explore Victoria's statewide insurance data or national home insurance statistics for more context.

---

Property Features That Affect Your Premium

Several characteristics of this property will have influenced how insurers priced the risk:

Hardiplank/Hardiflex external walls are a fibre cement cladding product widely used in Australian residential construction. Insurers generally view this material favourably — it's non-combustible, resistant to rot and termites, and holds up well in coastal environments where salt air can degrade timber and metal cladding over time. This is a positive factor for premium pricing.

Steel/Colorbond roofing is another tick in the box. Colorbond is durable, fire-resistant, and performs well in high-wind conditions. It's one of the most common roofing materials in coastal Victoria, and insurers are well-acquainted with its risk profile.

Stump foundations (also known as stumped or pier foundations) are common in older Victorian homes, particularly those built before the 1990s. While they allow for good airflow and are practical in certain soil conditions, they can introduce some vulnerability to underfloor damage and may warrant attention in terms of maintenance. Insurers typically price these similarly to slab foundations, though the age of the stumps and condition of the subfloor can be a factor.

Solar panels add replacement value to the property and are increasingly factored into building sum insured calculations. At $809,000, the building sum insured for this property appears to account for a 205 sqm home with quality fixtures — solar panels included.

Ducted climate control is another contents and building consideration. Ducted systems are expensive to repair or replace, and their presence is consistent with the $90,000 contents valuation and the standard fittings quality noted for this property.

The property is not in a cyclone risk area, which is a meaningful cost saving compared to properties in northern Australia. It is also pool-free, removing another layer of liability and replacement cost from the equation.

---

Tips for Homeowners in Ocean Grove

1. Review your building sum insured annually Construction costs have risen sharply in recent years. A 205 sqm home built in 1983 may have a replacement cost that differs significantly from its market value — and it's the replacement cost that matters for insurance. Make sure your $809,000 sum insured reflects current building rates in the Bellarine Peninsula area, including demolition and debris removal.

2. Check that your solar panels are properly covered Solar panel systems can be covered under either the building or contents section of your policy, depending on the insurer. Confirm with your provider exactly how your system is covered, what events are included (e.g., storm damage, accidental breakage), and whether the inverter is separately listed.

3. Consider your excess strategically Both the building and contents excess on this policy are set at $1,000. A higher excess typically reduces your annual premium. If you have a healthy emergency fund and are unlikely to make small claims, increasing your excess to $2,000 or more could lower your premium meaningfully — worth modelling before renewal.

4. Shop around at renewal time The 25th percentile for Ocean Grove premiums is $1,419 per year — nearly $1,100 less than this quote. While direct comparisons are difficult without identical cover details, it's a strong signal that competitive pricing exists in this market. Loyalty doesn't always pay in insurance; comparing quotes annually is one of the simplest ways to manage costs.

---

Compare Your Own Quote

Whether you're a long-time Ocean Grove local or new to the Bellarine Peninsula, it pays to know where your premium stands. CoverClub aggregates real quote data from Australian homeowners to give you transparent, suburb-level benchmarks — no sign-up required.

Get a home insurance quote and see how it compares in seconds. You might be paying more than you need to.