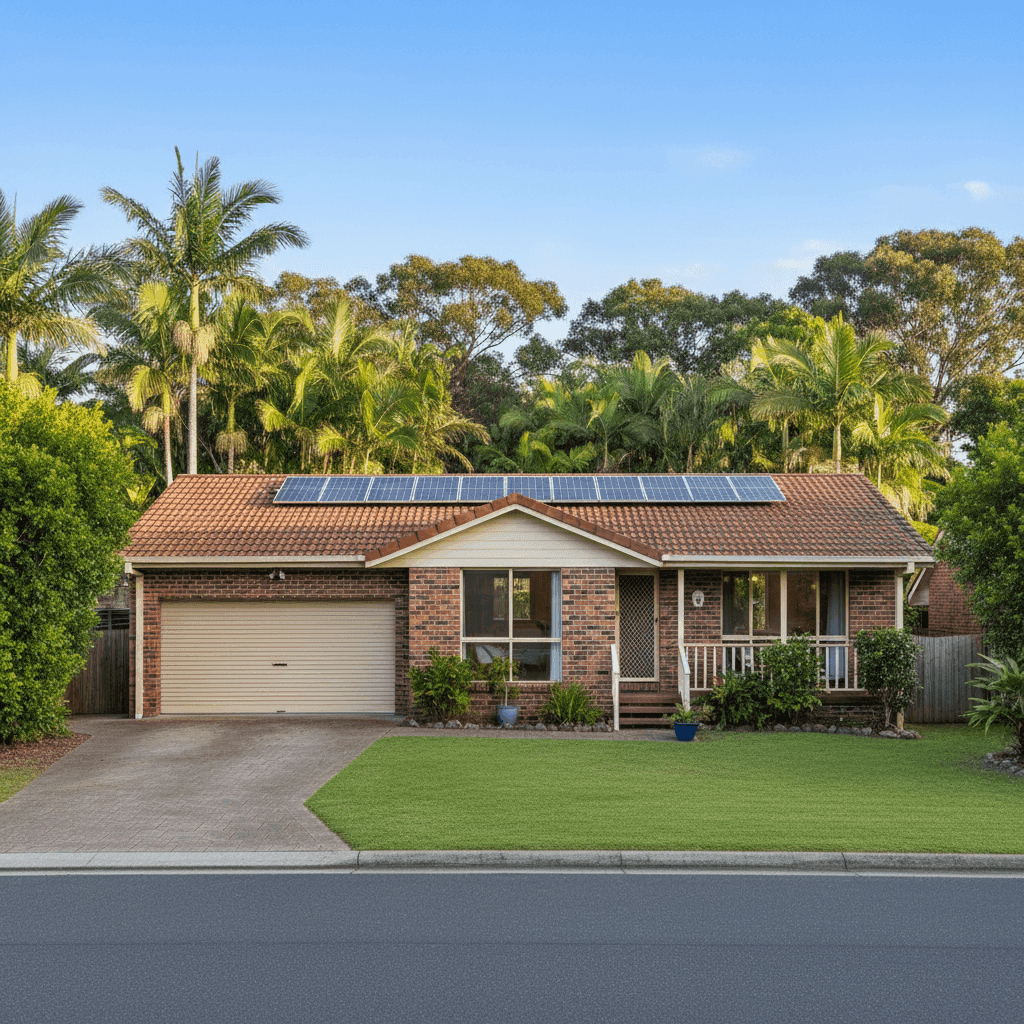

Ocean Shores is a laid-back coastal suburb tucked into the Northern Rivers region of New South Wales, just a short drive from Byron Bay. Known for its lush hinterland backdrop, surf beach access, and relaxed lifestyle, it's a sought-after location — but one that comes with its own set of insurance considerations. This article breaks down a recent building insurance quote for a four-bedroom, free-standing brick veneer home in the area, rated Expensive (Above Average), and helps you understand what's driving that price.

---

Is This Quote Fair?

The quoted annual premium of $8,477 (or $832/month) for building-only cover with a $3,000 excess sits well above what most Ocean Shores homeowners are paying. Based on 54 quotes collected for postcode 2483, the suburb average premium is $4,028 per year, and the median sits at $3,566. That means this quote is more than double the local median — a significant gap that warrants close attention.

Even at the upper end of the local market, the 75th percentile premium for Ocean Shores is $4,833 per year. This quote exceeds even that benchmark by a wide margin, placing it firmly in "expensive" territory by any reasonable measure.

It's worth noting that the sum insured of $750,000 for a 169 sqm home is on the higher side, and this will be one of the primary drivers of the elevated premium. Building sum insured is one of the most direct levers on your annual cost — the more it costs to rebuild your home, the more you'll pay to insure it. That said, even accounting for a generous rebuild estimate, the premium still appears steep compared to local benchmarks.

---

How Ocean Shores Compares

To put this quote in broader context, here's how Ocean Shores stacks up against NSW averages and national benchmarks:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Ocean Shores (2483) | $4,028/yr | $3,566/yr |

| Tweed LGA | $4,680/yr | — |

| NSW | $3,801/yr | $3,410/yr |

| National | $2,965/yr | $2,716/yr |

| This Quote | $8,477/yr | — |

A few things stand out here. Ocean Shores already sits above both the NSW state average and the national average — reflecting the elevated risk profile of coastal Northern Rivers properties. The Tweed LGA average of $4,680 is the highest benchmark in this comparison, which tells us that insurers are pricing Northern Rivers properties with a degree of caution, likely due to flood, storm, and rainfall risk in the region.

Still, even within this elevated local context, the $8,477 quote is a significant outlier. Homeowners in this area should absolutely shop around before accepting a premium at this level.

---

Property Features That Affect Your Premium

Several characteristics of this property are likely influencing the quote — some pushing the price up, others potentially working in the homeowner's favour.

Brick veneer construction is generally viewed favourably by insurers. It offers solid resistance to fire and wind compared to lightweight cladding materials, and most Australian insurers price it accordingly. This should, in theory, be a moderating factor on the premium.

Tiled roofing is similarly regarded as a lower-risk roofing material. Tiles are durable, fire-resistant, and less susceptible to storm damage than corrugated iron or Colorbond in many scenarios — though they can crack under hail. Overall, tiles tend to attract more competitive premiums than older or more vulnerable roofing types.

Slab foundation is standard for this era and region, and generally doesn't attract a premium loading on its own.

Timber and laminate flooring can be a factor in claims costs — these materials are more susceptible to water damage than tiles, which may subtly influence an insurer's risk assessment.

Solar panels are an increasingly common feature on Australian homes, but they do add to rebuild costs and can introduce additional risk factors (particularly around electrical faults and storm damage to panels). Many insurers factor solar installations into their building sum insured calculations, which can nudge premiums upward.

Ducted climate control is another above-average fitting that adds to the overall rebuild value of the home. Combined with the "above average" fittings quality noted for this property, it's reasonable to expect a higher-than-typical rebuild cost — and therefore a higher premium.

Construction year of 1988 places the home in a period where building standards were solid but not modern. Some insurers apply age-related loadings to homes of this vintage, particularly around plumbing, electrical, and roofing systems.

Finally, the Northern Rivers location itself is a major pricing factor. This region has experienced significant flood and storm events in recent years — most notably the catastrophic 2022 floods — and insurers have responded by repricing risk across much of the area. Even properties not directly in flood zones may see elevated premiums simply due to regional risk loading.

---

Tips for Homeowners in Ocean Shores

1. Review your sum insured carefully. A $750,000 building sum insured is substantial. Make sure it reflects a realistic rebuild cost — not the market value of your property. Tools like the Cordell Sum Sure Calculator can help you estimate an accurate figure. Over-insuring drives up your premium without adding meaningful protection.

2. Shop around — seriously. Given that this quote is more than double the local median, comparing multiple insurers is essential. Premiums for the same property can vary enormously between providers. Use CoverClub to compare quotes and see what other insurers are offering for your specific address and risk profile.

3. Ask about flood zone classification. If your property is not in a designated flood zone, confirm this with your insurer and ensure it's correctly reflected in your policy. Incorrect flood classifications can significantly inflate premiums. If you've been incorrectly categorised, you may have grounds to request a reassessment.

4. Consider your excess strategically. This policy carries a $3,000 building excess. Opting for a higher excess is one of the most straightforward ways to reduce your annual premium — but make sure you can comfortably cover that amount out of pocket if you need to make a claim. Find the balance that works for your financial situation.

---

Ready to Find a Better Deal?

If you're a homeowner in Ocean Shores or anywhere in the Northern Rivers, it pays to compare. CoverClub makes it easy to see how your current quote stacks up against the market — and to find a policy that gives you genuine value without overpaying. Get a home insurance quote today and see what's available for your property.