Old Toongabbie is a well-established suburb in Western Sydney's Cumberland local government area, known for its mix of family homes, leafy streets, and convenient access to Parramatta and the broader Sydney metro. If you own a free standing home here, understanding what you should expect to pay for home and contents insurance — and why — can make a significant difference to your household budget. This article breaks down a real quote for a six-bedroom property in the area, compares it against local, state, and national benchmarks, and offers practical advice for homeowners looking to get better value from their cover.

---

Is This Quote Fair?

The quote in question comes in at $5,088 per year (or $470 per month) for combined home and contents insurance, covering a building sum insured of $2,034,000 and contents valued at $301,000, with a $1,000 excess on both building and contents claims.

Our pricing analysis rates this quote as Expensive — above average for the area. That's a meaningful finding worth unpacking.

To put it in context: the suburb average for Old Toongabbie sits at around $2,122 per year, with a median of just $1,090. This quote is more than double the local average and nearly five times the suburb median. Even at the 75th percentile — meaning three-quarters of quotes in the area are cheaper — the benchmark is $3,148 per year, still well below this figure.

That said, context matters enormously here. This is a large, six-bedroom home with a high building sum insured of over $2 million. The contents cover alone adds $301,000 to the risk profile. When you factor in additional features like a swimming pool, solar panels, and ducted climate control, the insurer is covering considerably more than a typical three-bedroom suburban home. So while the price tag looks steep at first glance, it's partly a reflection of the scale and value of what's being insured.

---

How Old Toongabbie Compares

Zooming out to a broader view helps calibrate whether this premium is genuinely high or simply the cost of insuring a larger-than-average home.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Old Toongabbie (2146) | $2,122/yr | $1,090/yr |

| Cumberland LGA | $2,285/yr | — |

| New South Wales | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

Compared to the NSW state average of $9,528 per year, this quote is actually below par — a reassuring sign. And against the national average of $5,347, it comes in slightly cheaper as well. The national median of $2,764 per year is lower, but again, that reflects a much broader pool of properties of varying sizes and values.

The Cumberland LGA average of $2,285 per year is more directly comparable geographically, though it still covers a wide range of property types. The key takeaway: for a home of this size and insured value, the quote is broadly in line with — or even below — state and national averages, even if it sits above what most Old Toongabbie homeowners pay.

It's worth noting that the suburb sample size is relatively small (7 quotes), so the local benchmarks should be treated as indicative rather than definitive.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on what insurers charge. Understanding them helps you see where the premium comes from — and where there might be room to move.

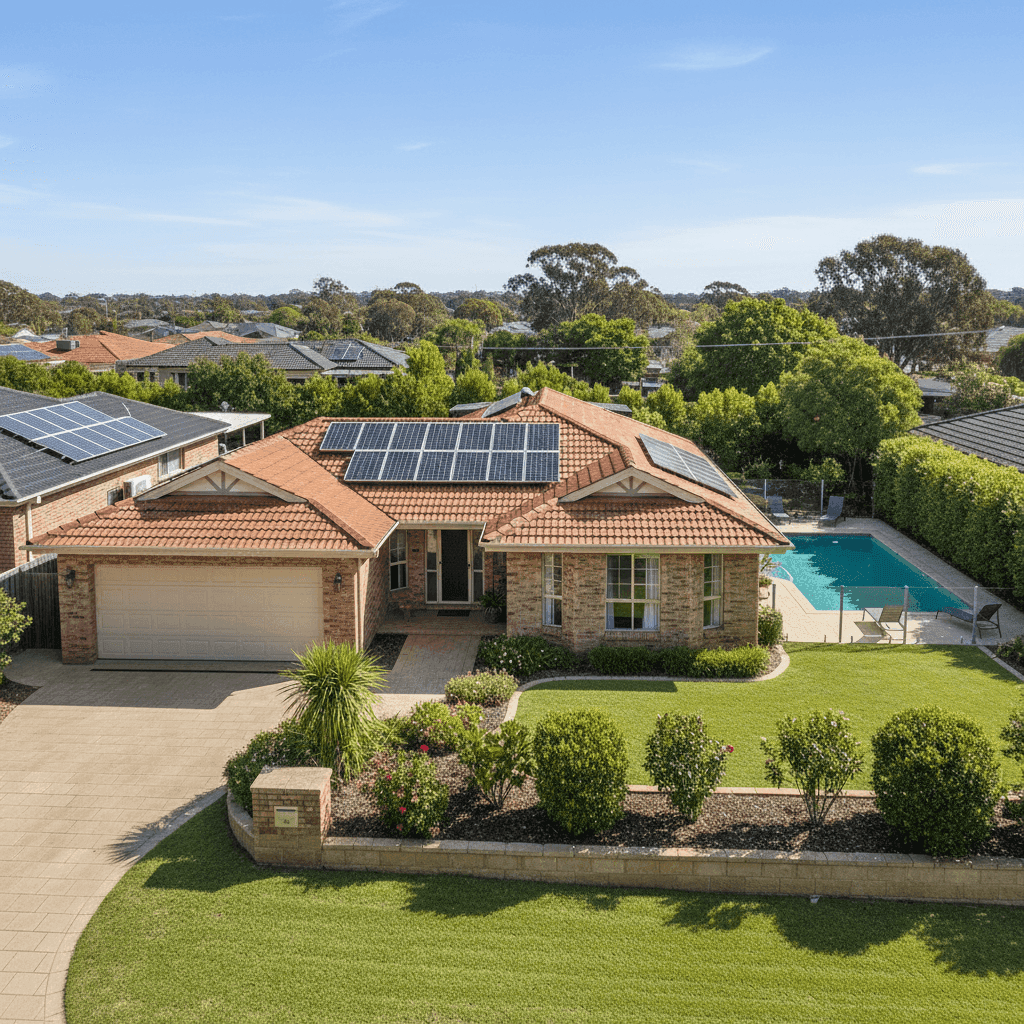

Size and sum insured: At 452 sqm with six bedrooms and two bathrooms, this is a large home by any measure. A building sum insured of $2,034,000 reflects the cost to fully rebuild a property of this scale, and insurers price accordingly. Larger sums insured mean larger potential payouts, which directly lifts the base premium.

Construction type: Brick veneer walls and a tiled roof are generally viewed favourably by insurers. Both materials offer solid fire resistance and durability compared to alternatives like timber weatherboard or Colorbond steel. The slab foundation is similarly low-risk. These construction features likely help keep the premium from climbing even higher.

Swimming pool: A pool adds both value and liability to a property. Insurers factor in the cost of pool-related damage (e.g., from storms or structural issues) as well as the public liability exposure that comes with having a pool on the premises. Expect this to contribute a noticeable loading to your premium.

Solar panels: Solar systems are now a standard feature on many Australian homes, but they do add to the replacement cost of the property. A quality solar installation can cost $10,000–$20,000 or more to replace, and this is factored into the building sum insured and the insurer's risk calculations.

Ducted climate control: Ducted air conditioning systems are expensive to repair or replace — often $15,000–$30,000 for a full system. Their inclusion in the building sum insured adds to the overall replacement cost and, by extension, the premium.

Year of construction: Built in 1993, the home is over 30 years old. Properties of this vintage may carry a slightly higher risk profile than newer builds due to ageing infrastructure (plumbing, electrical systems, roofing materials), though this is often offset by solid construction practices common in that era.

---

Tips for Homeowners in Old Toongabbie

1. Review your sum insured carefully With a building sum insured of over $2 million, it's essential this figure accurately reflects the cost to rebuild — not the market value of the property. Overinsuring inflates your premium unnecessarily, while underinsuring leaves you exposed at claim time. Use a reputable building cost calculator or speak with a quantity surveyor to validate your figure annually.

2. Compare quotes from multiple insurers The insurance market is competitive, and premiums for the same property can vary by hundreds — sometimes thousands — of dollars between providers. Get a comparison quote at CoverClub to see how your current premium stacks up against the broader market.

3. Consider your excess settings Both the building and contents excess on this policy sit at $1,000. Opting for a higher voluntary excess (say, $2,500 or $5,000) can reduce your annual premium meaningfully. If you have the financial buffer to cover a larger out-of-pocket cost in the event of a claim, this can be a smart way to lower ongoing costs.

4. Bundle and ask about discounts Many insurers offer discounts for bundling home and contents cover (as this policy does), maintaining a claims-free history, or installing security systems. It's worth contacting your insurer directly to ask what discounts you may be eligible for — they're not always applied automatically.

---

Find a Better Deal with CoverClub

Whether you're renewing your current policy or shopping around for the first time, comparing quotes is the single most effective way to ensure you're not overpaying. CoverClub makes it easy to see how your premium compares to others in Old Toongabbie and across New South Wales. Start a free quote today and find out if you could be paying less for the same level of cover.