If you own a free standing home in One Tree Hill, SA 5114, you've probably wondered whether your home insurance premium is competitive — or whether you're paying more than you should be. This article breaks down a recent home and contents insurance quote for a four-bedroom, double brick home in the suburb, compares it against local and national benchmarks, and offers practical tips to help you get better value on your cover.

---

Is This Quote Fair?

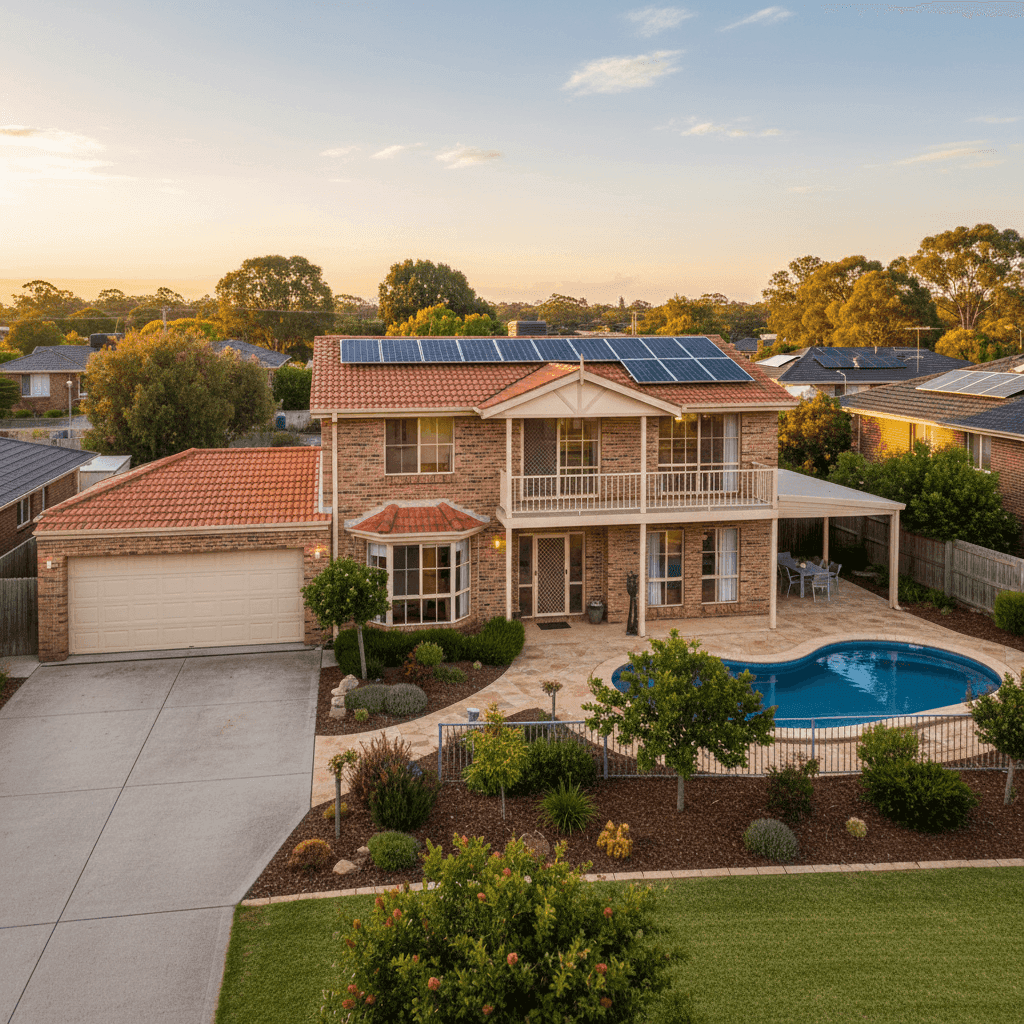

The quote in question comes in at $2,886 per year (or $277 per month) for combined home and contents cover, with a building sum insured of $763,000 and contents valued at $66,000. Both the building and contents excess are set at $1,000.

Based on available pricing data, this quote is rated Expensive — above average for the area. It sits above the suburb average of $2,487/yr and just above the suburb's 75th percentile of $2,834/yr, meaning it's pricier than roughly three-quarters of comparable quotes in One Tree Hill.

That said, context matters. The higher building sum insured ($763,000) is a significant driver here — a larger insured value naturally attracts a higher premium. The property also features a swimming pool, solar panels, and ducted climate control, all of which add to the replacement cost and risk profile of the home. So while the quote is above average, it's not necessarily unreasonable given what's being covered.

---

How One Tree Hill Compares

Understanding where your suburb sits in the broader pricing landscape is key to evaluating any quote. Here's how One Tree Hill stacks up:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $2,886 |

| Suburb Average (5114) | $2,487 |

| Suburb Median (5114) | $2,429 |

| Suburb 25th Percentile | $2,015 |

| Suburb 75th Percentile | $2,834 |

| SA State Average | $2,433 |

| SA State Median | $1,679 |

| LGA Average (Gawler) | $1,429 |

| National Average | $5,347 |

| National Median | $2,764 |

A few things stand out from this comparison. First, One Tree Hill premiums are broadly in line with the South Australian state average of $2,433/yr, suggesting the suburb doesn't carry any extraordinary local risk loading. Second, the national average of $5,347/yr is dramatically higher — largely driven by high-risk regions in Queensland and Western Australia where cyclone and flood exposure push premiums up significantly. By that measure, One Tree Hill homeowners are in a relatively affordable part of the country.

Interestingly, the LGA average for Gawler sits notably lower at $1,429/yr. This likely reflects a mix of lower-value properties and simpler risk profiles across the broader Gawler council area, rather than a direct like-for-like comparison with this particular property.

You can explore more localised pricing data on the One Tree Hill suburb stats page.

> Note: The suburb sample size for this comparison is 8 quotes, so these averages should be treated as indicative rather than definitive. A larger dataset would provide a more robust benchmark.

---

Property Features That Affect Your Premium

Several characteristics of this property have a meaningful influence on the insurance premium. Here's what's at play:

Double Brick Construction

Double brick is generally viewed favourably by insurers. It's durable, fire-resistant, and less susceptible to storm damage than timber or clad construction. This can work in the homeowner's favour when it comes to pricing.

Tiled Roof

Terracotta or concrete tile roofs are a standard and well-regarded roofing material in South Australia. They tend to be more resilient than Colorbond in hail events but can be more expensive to repair if individual tiles crack or shift. Insurers generally price tiled roofs at a moderate risk level.

Slab Foundation & Tiled Flooring

A concrete slab foundation is common for homes built in the early 1990s and is considered structurally sound. Combined with tiled flooring throughout, this reduces the risk of water damage claims compared to properties with timber subfloors or carpet.

Swimming Pool

A pool adds both value and risk to a property. It increases the replacement cost of the home and introduces liability considerations. Homeowners should ensure their policy explicitly covers pool infrastructure, including pumps, filtration systems, and surrounding paving.

Solar Panels

Solar panels are increasingly common across South Australia, but they're not always automatically covered under standard building policies. It's worth confirming with your insurer that your panels — including inverters and mounting hardware — are included in your building sum insured.

Ducted Climate Control

A ducted heating and cooling system is a significant fixed asset that forms part of the building. At standard fittings quality, it contributes meaningfully to the overall replacement cost, which is reflected in the $763,000 building sum insured.

No Cyclone Risk

One Tree Hill is not located in a cyclone risk zone, which is a genuine premium advantage. Properties in northern Australia can pay substantially more due to cyclone loading, so this is a meaningful cost saving for SA homeowners.

---

Tips for Homeowners in One Tree Hill

1. Review Your Building Sum Insured Carefully

At $763,000, the building sum insured is the single biggest driver of this premium. Make sure this figure reflects the actual cost to rebuild your home from scratch — not its market value. Overcovering can be just as costly as undercovering. Consider getting a building replacement cost estimate from a quantity surveyor every few years.

2. Confirm Solar Panels Are Covered

South Australia has one of the highest rates of solar adoption in the country, but coverage isn't always automatic. Ask your insurer directly whether your solar system is included in the building sum insured, and whether accidental damage to panels is covered.

3. Bundle and Compare

Home and contents insurance is often cheaper when bundled with the same insurer. However, bundling doesn't always guarantee the best deal — it's worth comparing combined quotes against separate policies to see which offers better value. Platforms like CoverClub make this comparison straightforward.

4. Revisit Your Excess

This policy carries a $1,000 excess on both building and contents. Opting for a higher excess (say, $2,000) can meaningfully reduce your annual premium. If you have sufficient savings to cover a larger out-of-pocket expense in the event of a claim, this can be a smart way to lower your ongoing costs.

---

Compare Your Quote Today

Whether you're renewing your existing policy or shopping for cover for the first time, it pays to compare. Premiums for the same property can vary significantly between insurers — sometimes by hundreds of dollars a year. Get a home insurance quote through CoverClub to see how your current premium stacks up and whether there's a better deal available for your One Tree Hill home.