Orange is one of New South Wales' most charming regional cities — known for its cool-climate produce, vibrant food scene, and a strong sense of community. It's also a place where homeowners are increasingly asking whether they're getting a fair deal on their home insurance. This article takes a close look at a real building-only insurance quote for a five-bedroom, free-standing home in Orange, NSW 2800, breaking down what's driving the premium and how it stacks up against local, state, and national benchmarks.

---

Is This Quote Fair?

The annual premium for this property came in at $2,459 per year (or $236/month), with a $1,000 building excess and a sum insured of $685,000. CoverClub's pricing engine rates this quote as EXPENSIVE — above average for the area.

To put that in perspective:

- The suburb average for Orange (2800) is $1,462/yr

- The suburb median sits at just $1,135/yr

- Even the 75th percentile — meaning 75% of quotes are cheaper — comes in at $1,858/yr

This quote sits well above the 75th percentile, meaning it's more expensive than roughly three-quarters of comparable quotes in the suburb. That's a meaningful gap, and one worth investigating before renewing or accepting a policy at this price.

That said, it's important to recognise that premiums aren't one-size-fits-all. A larger, older home with specific construction characteristics will naturally attract higher premiums than a compact modern townhouse. The key question is whether the price reflects the actual risk profile of the property — or whether there's a better deal out there.

---

How Orange Compares

Understanding where Orange sits in the broader insurance landscape helps contextualise any individual quote. Here's a snapshot based on NSW state data and national figures:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Orange (suburb) | $1,462/yr | $1,135/yr |

| LGA (Dubbo region) | $3,426/yr | — |

| NSW (state) | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. First, Orange is actually quite affordable compared to the broader NSW average — the state average of $9,528 is heavily skewed by high-risk coastal and flood-prone areas. Second, the LGA average of $3,426 (which covers the broader Dubbo regional area) is notably higher than Orange's suburb average, suggesting Orange itself is a relatively lower-risk pocket within the region.

Against the national median of $2,764, this particular quote of $2,459 is actually slightly below — which is a useful reminder that "expensive for Orange" doesn't necessarily mean expensive in absolute terms. Orange homeowners generally enjoy more competitive premiums than many parts of Australia.

Still, with a suburb median of just $1,135, there's clearly room to shop around.

---

Property Features That Affect Your Premium

Several characteristics of this property are likely influencing the premium, both upward and downward.

Size and Age

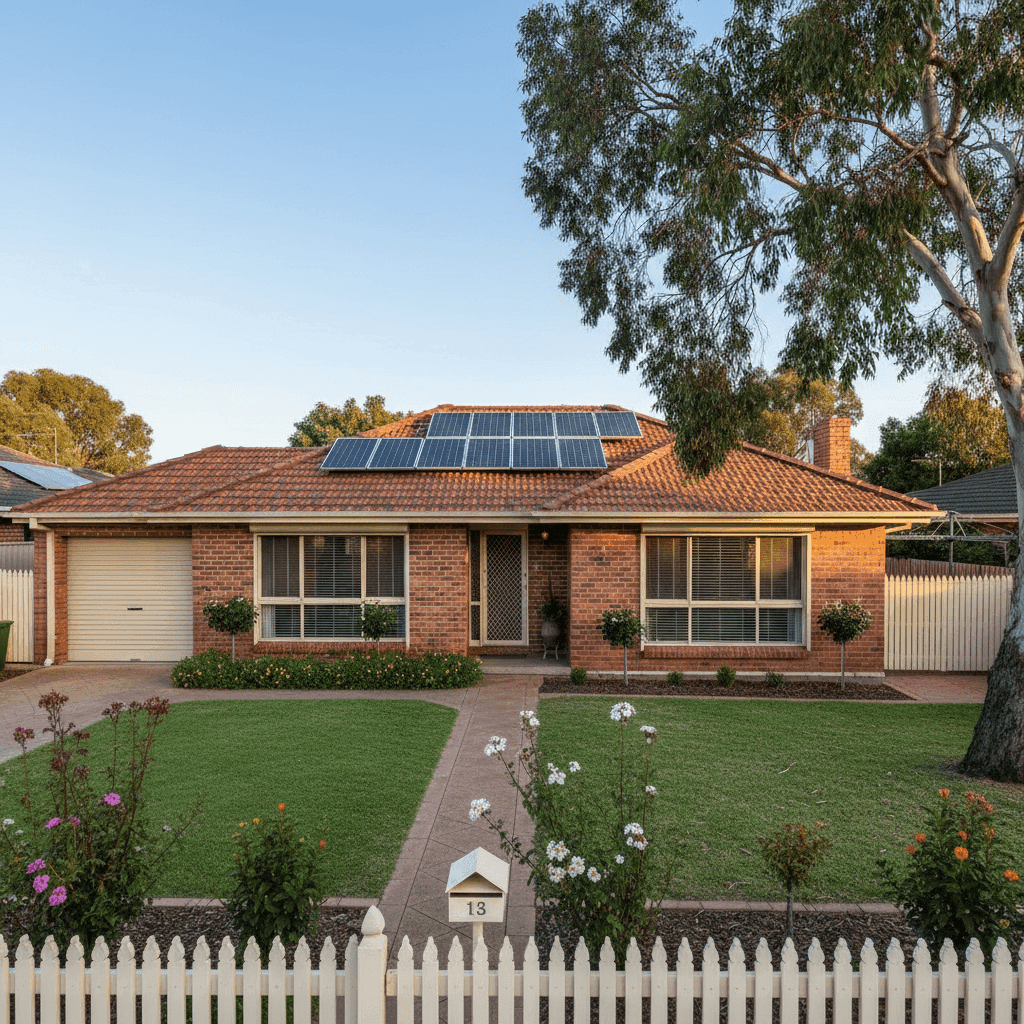

At 286 sqm, this is a sizeable home — well above the average Australian dwelling. Larger homes cost more to rebuild, which directly increases the sum insured and, in turn, the premium. The $685,000 sum insured reflects the rebuild cost for a property of this scale, and insurers price accordingly.

The home was built in 1976, making it nearly 50 years old. Older properties can carry higher risk in the eyes of insurers due to ageing electrical wiring, plumbing, and structural components that may not meet current building codes.

Construction: Brick Veneer on Stumps

Brick veneer walls are generally viewed favourably by insurers — they offer solid fire resistance and durability. However, this home sits on stump foundations, which is common in older NSW homes but can introduce concerns around subsidence, pest ingress, and structural movement over time. Combined with timber and laminate flooring, which is more vulnerable to moisture and pest damage than concrete slab alternatives, this foundation type may be nudging the premium higher.

Roof

A tiled roof is a neutral-to-positive factor for insurers — tiles are durable and widely used across regional NSW. They do carry some risk of cracking or displacement in severe weather, but are generally well-regarded.

Solar Panels and Ducted Climate Control

The presence of solar panels adds replacement value to the building and can slightly increase premiums, as they represent an additional insurable asset. Ducted climate control similarly adds to the overall value of the home's fixtures and fittings, contributing to the rebuild cost estimate.

No Pool, No Cyclone Risk

The absence of a swimming pool removes one common liability and maintenance risk from the equation. And being located in Orange — well inland and at elevation — means this property sits outside cyclone risk zones, which is a meaningful premium-saving factor compared to properties in northern Queensland or coastal NT.

---

Tips for Homeowners in Orange

If you're a homeowner in Orange looking to get better value from your building insurance, here are four practical steps worth considering:

- Shop around — seriously. With a suburb median of $1,135 and this quote sitting at $2,459, the gap is substantial. Use a comparison platform like CoverClub to benchmark your current policy against live market rates. Even switching to a comparable policy from a different insurer could save hundreds annually.

- Review your sum insured carefully. Over-insuring is a common and costly mistake. Make sure your $685,000 (or whatever figure your policy uses) reflects a genuine rebuild cost estimate — not the market value of the property. Tools like the Cordell Sum Sure calculator can help you arrive at a more accurate figure.

- Ask about bundling discounts. If you have contents, car, or landlord insurance, many providers offer multi-policy discounts. Even if this is a building-only policy, it's worth asking whether bundling could reduce your overall insurance spend.

- Consider your excess strategically. A $1,000 excess is fairly standard, but increasing it to $2,500 or even $5,000 can meaningfully reduce your annual premium if you have the financial buffer to cover a larger out-of-pocket cost in the event of a claim. This trade-off is worth modelling with your insurer.

---

Find a Better Deal with CoverClub

Whether you're renewing your current policy or shopping for the first time, CoverClub makes it easy to see how your quote stacks up. Our platform aggregates real pricing data from across Australia so you can make an informed decision — not just accept the first number that lands in your inbox. Get a quote today and see what homeowners in Orange are actually paying.