If you own a four-bedroom free standing home in Orange, NSW 2800, you're probably wondering whether your home and contents insurance premium stacks up against what your neighbours are paying. Orange is a thriving regional city in the Central Tablelands, known for its cool climate, heritage streetscapes, and a growing property market. It's also a place where insurance costs can vary quite a bit depending on your property's characteristics and the insurer you choose.

This article breaks down a real home and contents insurance quote for a four-bedroom, three-bathroom brick veneer home in Orange — and puts the numbers in context so you can make a more informed decision.

---

Is This Quote Fair?

The quote in question comes in at $3,152 per year (or $302 per month), covering a building sum insured of $867,000 and contents valued at $50,000. Both the building and contents carry a $1,000 excess.

Our price rating for this quote is Expensive — above average for the Orange area.

To understand why, consider that the suburb average premium for Orange (NSW 2800) sits at just $1,462 per year, with a median of $1,135 per year. This quote is more than double the suburb average and nearly three times the median. Even at the 75th percentile — meaning 75% of Orange quotes are cheaper — the benchmark is only $1,858 per year, still well below this figure.

That said, it's important to note that the sum insured here is quite high at $867,000. Building replacement costs are a primary driver of premiums, and a higher insured value will naturally push the price up. If comparable quotes in the suburb are insuring smaller or lower-valued homes, a direct comparison isn't entirely apples-to-apples. Still, the gap is significant enough to warrant shopping around.

---

How Orange Compares to NSW and Australia

Zooming out to a broader view, Orange actually looks relatively affordable compared to the rest of New South Wales. According to NSW home insurance data, the state average premium is a staggering $9,528 per year, with a median of $3,770 per year. Much of this is driven by high-risk coastal and flood-prone areas, as well as the Sydney metro market where property values are significantly higher.

At the national level, the average premium across Australia is $5,347 per year, with a median of $2,764 per year.

Here's a quick snapshot of how this quote sits across different benchmarks:

| Benchmark | Premium |

|---|---|

| This Quote | $3,152/yr |

| Orange Suburb Average | $1,462/yr |

| Orange Suburb Median | $1,135/yr |

| Orange 75th Percentile | $1,858/yr |

| LGA (Dubbo Region) Average | $3,426/yr |

| NSW State Average | $9,528/yr |

| National Average | $5,347/yr |

Interestingly, the Dubbo LGA average of $3,426 per year is actually quite close to this quote, suggesting that at a regional level, the pricing isn't entirely out of line. The Orange suburb sample (37 quotes) may skew lower if many of those properties carry lower sums insured.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on the premium calculated. Here's what's likely at play:

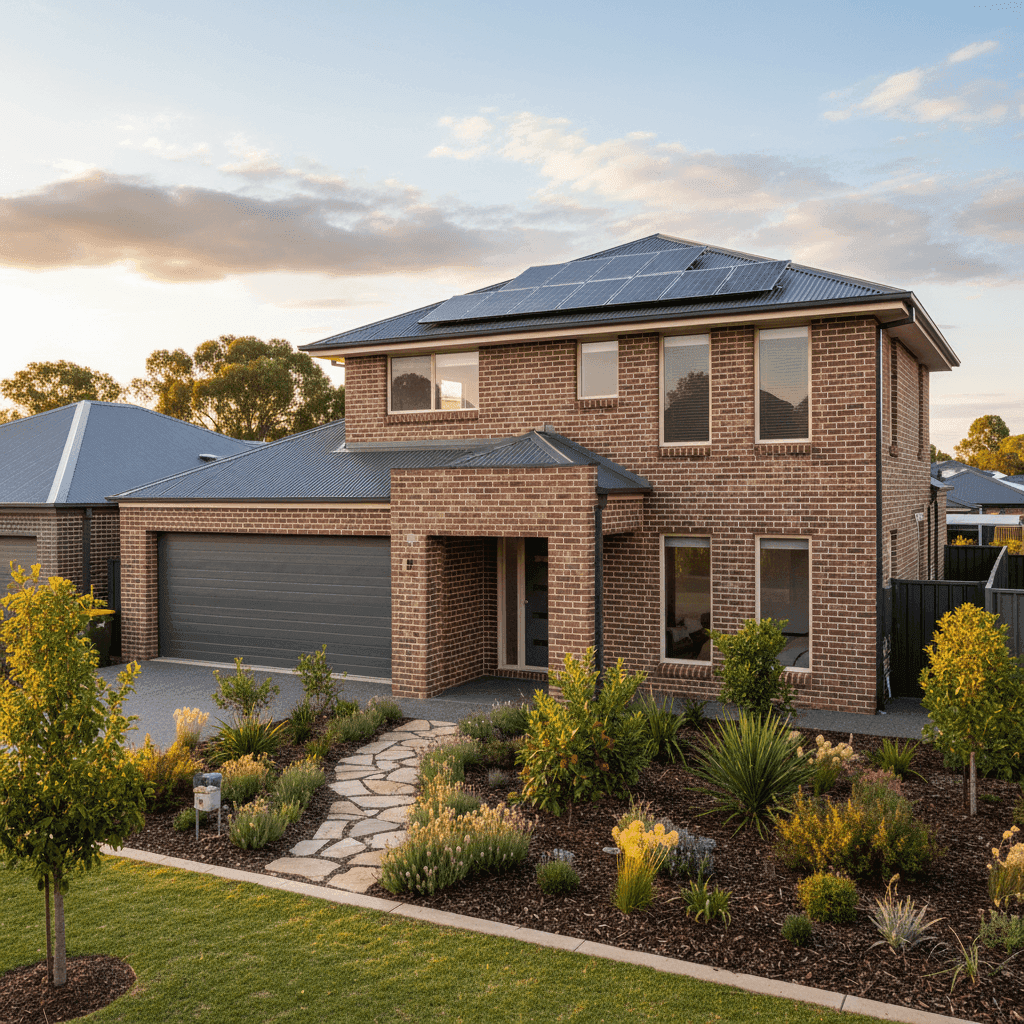

Brick Veneer Construction Brick veneer is one of the more common external wall materials in regional NSW and is generally viewed favourably by insurers. It offers solid fire resistance and structural durability, which can help moderate premiums compared to weatherboard or lightweight cladding.

Steel / Colorbond Roof A Colorbond steel roof is widely regarded as a premium roofing material in Australia. It's durable, low-maintenance, and performs well in both heat and cold — all factors that reduce the likelihood of weather-related claims. This is a positive for your premium.

Slab Foundation A concrete slab foundation is generally considered stable and low-risk from an insurer's perspective, particularly in non-reactive soil areas. It avoids the subsidence and pest-entry risks sometimes associated with older stumped or timber-framed subfloors.

Timber / Laminate Flooring Flooring type can influence contents and building claims, particularly for water damage events. Timber and laminate floors can be costly to repair or replace if damaged by water ingress, which may factor into the overall pricing.

Solar Panels This property has solar panels installed. While solar panels add value to a home, they also add to the replacement cost in the event of damage — whether from hail, storm, or fire. Insurers typically include solar panels in the building sum insured, so ensuring your coverage accurately reflects their value is important.

Ducted Climate Control Ducted systems are a significant fixture in terms of replacement value. A full ducted heating and cooling system can cost tens of thousands of dollars to replace, and this will be factored into the building sum insured.

Building Size: 214 sqm At 214 square metres, this is a comfortably sized family home. Rebuild costs in regional NSW typically range from $2,000 to $3,000+ per square metre depending on finishes, meaning a sum insured of $867,000 is broadly in line with realistic rebuild estimates for a home of this size and specification.

No Pool, No Cyclone Risk The absence of a pool removes a common liability and maintenance risk factor, and Orange's inland location means it falls outside cyclone risk zones — both of which help keep premiums lower than they might otherwise be.

---

Tips for Homeowners in Orange

1. Review your sum insured carefully The building sum insured of $867,000 is the biggest lever on your premium. Use a reputable building cost calculator (many insurers offer these for free) to verify whether your current sum insured is accurate. Over-insuring costs you money; under-insuring can leave you exposed at claim time.

2. Compare at least three quotes With 37 quotes in the Orange suburb sample showing an average of $1,462 per year, there's clearly a wide range of pricing in the market. Even accounting for the higher sum insured, comparing multiple insurers could reveal meaningful savings. Get a comparison quote at CoverClub to see what other insurers are offering for your property.

3. Ask about bundling discounts Some insurers offer discounts when you combine home and contents cover under a single policy. Since this quote already covers both, confirm that you're receiving any applicable multi-cover discount.

4. Consider your excess level Both excesses here are set at $1,000. Opting for a higher voluntary excess — say $2,000 — can reduce your annual premium noticeably. If you have a solid emergency fund and rarely make small claims, this trade-off can make financial sense over time.

---

Ready to Find a Better Deal?

Whether you're renewing your policy or shopping around for the first time, comparing quotes is one of the simplest ways to ensure you're not overpaying. CoverClub makes it easy to compare home and contents insurance options for properties across Orange and regional NSW — so you can find cover that fits both your home and your budget.

You can also explore detailed Orange suburb insurance statistics, NSW state-wide data, and national benchmarks to better understand where your premium sits in the broader market.