Orange, NSW is one of Central West's most sought-after regional cities — known for its cool climate, thriving food scene, and a strong property market that continues to attract families and tree-changers alike. If you own a free standing home in the 2800 postcode and you're trying to make sense of your home and contents insurance premium, you're in the right place. This article breaks down a real quote for a five-bedroom property in Orange, benchmarks it against local, state, and national data, and offers practical advice for getting better value on your cover.

---

Is This Quote Fair?

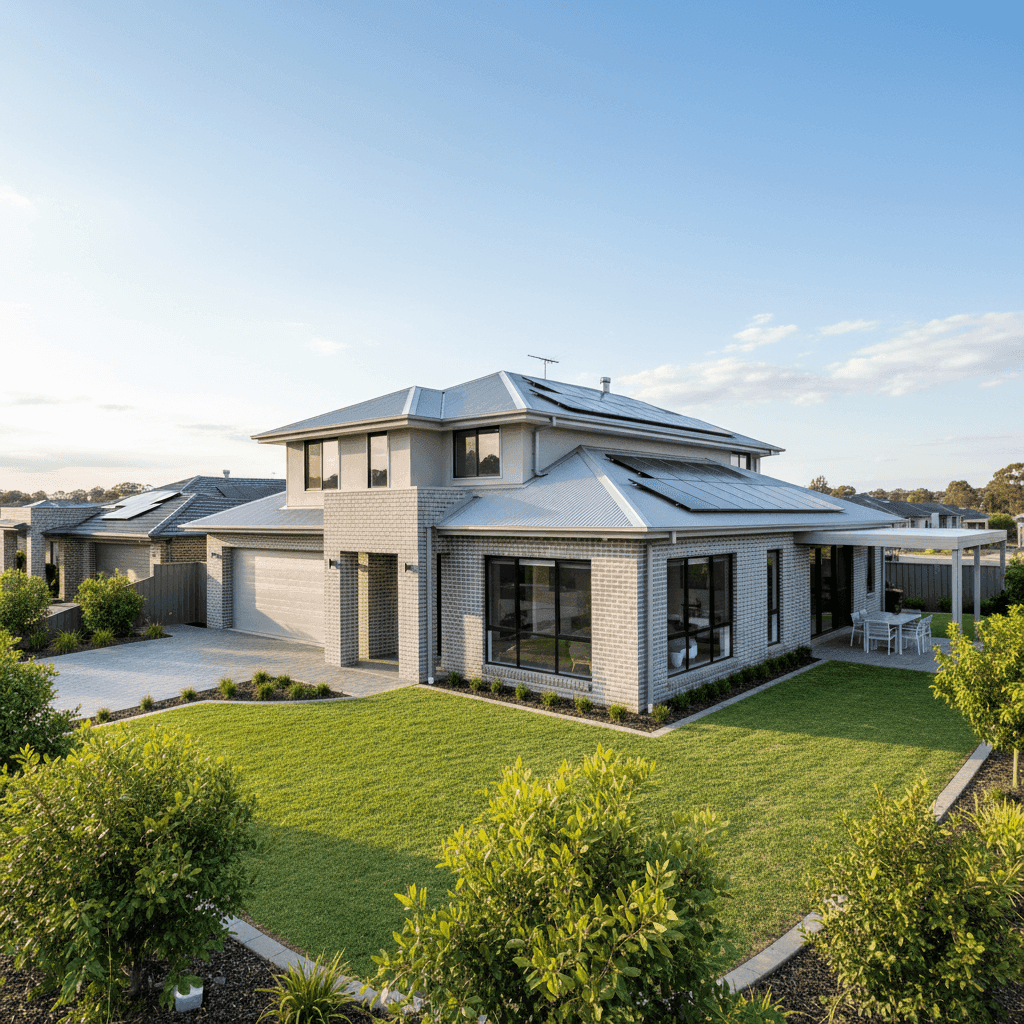

The quote in question comes in at $4,665 per year (or $453/month) for combined home and contents insurance, covering a building sum insured of $1,157,000 and contents valued at $200,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is Expensive — above average for the area.

To put that in context: the average home insurance premium in Orange (2800) sits at just $1,462 per year, with a median of $1,135. This quote is more than three times the suburb average — a significant gap that warrants a closer look.

That said, it's important to remember that averages can be misleading. The suburb sample includes properties of all sizes and cover levels. A five-bedroom home with top-of-the-range fittings, a 277 sqm footprint, and a $1.157 million building sum insured is going to attract a substantially higher premium than a modest three-bedroom home insured for $500,000. When you factor in the high replacement value and premium contents cover, the figure becomes more understandable — though it still sits on the higher end of what comparable properties should be paying.

---

How Orange Compares to NSW and National Benchmarks

One of the more striking findings from our data is just how affordable Orange is relative to the broader NSW insurance market.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Orange (2800) | $1,462/yr | $1,135/yr |

| LGA (Dubbo region) | $3,426/yr | — |

| NSW State | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

Orange homeowners are, on the whole, paying significantly less than the NSW state average — which is heavily skewed by high-risk coastal and flood-prone areas. Even compared to the national average of $5,347, Orange comes out well ahead in terms of affordability for most homeowners.

The quote analysed here, at $4,665, actually sits below the national average — which is a useful anchor point when you're insuring a large, high-value property. For a home of this size and specification, paying less than the national average is arguably reasonable, even if it appears steep compared to the typical Orange property.

The 75th percentile for Orange premiums is $1,858 per year — meaning 75% of quotes in the suburb come in below that figure. This quote exceeds even that upper band, reflecting the outsized nature of the property and its insured values.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on the premium calculated:

Size and Sum Insured At 277 sqm with five bedrooms and three bathrooms, this is a large home by any measure. The building sum insured of $1,157,000 reflects the genuine cost to rebuild — and that figure drives the base premium more than almost any other factor. Underinsuring might lower your premium, but it's a risk that can leave you seriously out of pocket after a total loss.

Top-of-the-Range Fittings High-end fittings — think stone benchtops, premium cabinetry, quality fixtures throughout — are more expensive to repair or replace, and insurers price accordingly. This property's "top of the range" fittings classification is a meaningful contributor to the elevated premium.

Brick Veneer Walls and Colorbond Roof Brick veneer construction is generally viewed favourably by insurers — it's durable, fire-resistant, and widely used across Australian suburbs. A steel Colorbond roof is similarly regarded as a solid, low-maintenance choice. These construction types typically attract standard or slightly reduced rates compared to timber-framed or tiled alternatives.

Slab Foundation A concrete slab foundation offers good structural stability and is common in homes built from the 1990s onwards. It's generally considered a neutral-to-positive factor from an insurance risk perspective.

Solar Panels This property has solar panels installed, which are typically covered under building insurance but can add a small amount to the premium due to their replacement cost. It's worth confirming with your insurer exactly what's covered — some policies include solar systems automatically, while others require a specific endorsement.

Ducted Climate Control Ducted air conditioning systems are a significant fixed asset and are generally included in building cover. Their presence adds to the overall replacement cost of the home, contributing modestly to the insured value and premium.

No Pool, No Cyclone Risk The absence of a swimming pool removes a common liability and maintenance risk factor. Orange is also outside any designated cyclone risk zone, which keeps premiums lower than they'd be in northern Queensland or parts of WA.

---

Tips for Homeowners in Orange

1. Review Your Sum Insured Annually Building costs have risen sharply over recent years. Make sure your sum insured reflects current rebuild costs — not what you paid for the property or what it was worth a few years ago. Many insurers offer a calculator, or you can use an independent quantity surveyor for a precise figure.

2. Compare Quotes Before Renewing Loyalty doesn't always pay in insurance. Insurers frequently offer better rates to new customers than to existing ones. Before your renewal date, use a comparison platform like CoverClub to see what other providers are offering for the same level of cover.

3. Consider Bundling Building and Contents Purchasing building and contents cover together — as in this quote — often attracts a discount compared to buying them separately. If you currently have them with different insurers, it may be worth consolidating.

4. Check Your Excess Settings A $1,000 excess on both building and contents is fairly standard. If you're financially comfortable absorbing a higher out-of-pocket cost in the event of a claim, increasing your excess to $2,000 or more can meaningfully reduce your annual premium. Just make sure the saving is worth the additional risk exposure.

---

Ready to Compare?

Whether your premium feels too high or you simply want peace of mind that you're on the right deal, comparing quotes is always a smart move. At CoverClub, you can benchmark your home insurance against real market data for Orange and beyond — in minutes, with no obligation. Don't let inertia cost you hundreds of dollars a year.