If you own or are considering insuring a semi detached home in Oxenford, QLD 4210, understanding what a fair premium looks like can save you hundreds of dollars a year. This analysis breaks down a real home and contents insurance quote for a five-bedroom, two-bathroom semi detached property in Oxenford — and puts the numbers into context against suburb, state, and national benchmarks.

---

Is This Quote Fair?

The annual premium on this quote comes in at $2,765 per year (or $265/month), covering a building sum insured of $653,000 and contents valued at $50,000, each with a $1,000 excess. Our price rating for this quote is FAIR — Around Average.

That rating reflects a nuanced position in the market. The premium sits comfortably below the suburb average of $4,299/yr and also below the suburb median of $3,274/yr. In fact, at $2,765/yr, it's sitting right at the 25th–50th percentile range for Oxenford — meaning roughly half of comparable properties in the area are paying more, and about a quarter are paying less (the suburb's 25th percentile sits at $2,357/yr).

So while it's not the cheapest quote available in the suburb, it's well below the top end of the market (the 75th percentile hits $4,722/yr), and the homeowner is getting solid coverage for a price that's genuinely competitive. The "Fair" rating is a reasonable reflection of where this quote lands.

---

How Oxenford Compares

To really appreciate this quote, it helps to zoom out and look at the broader picture. Here's how Oxenford stacks up against Queensland and the national market:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Oxenford (suburb) | $4,299/yr | $3,274/yr |

| Gold Coast LGA | $8,161/yr | — |

| Queensland (state) | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. The Queensland state average of $9,129/yr is dramatically higher than both the suburb and national figures — this is largely driven by high-risk coastal and cyclone-prone areas in Far North Queensland pushing the average up significantly. The Gold Coast LGA average of $8,161/yr similarly reflects the broader region's exposure to weather events, even though Oxenford itself is not classified as a cyclone risk area.

Compared to the national average of $5,347/yr, this quote at $2,765/yr is nearly half the price — a meaningful saving. And against the national median of $2,764/yr, this quote is virtually identical, suggesting it's right in line with what typical Australian homeowners are paying.

For a detailed breakdown of what homeowners in the 4210 postcode are paying, visit the Oxenford suburb stats page, which draws on data from 121 quotes in this area.

---

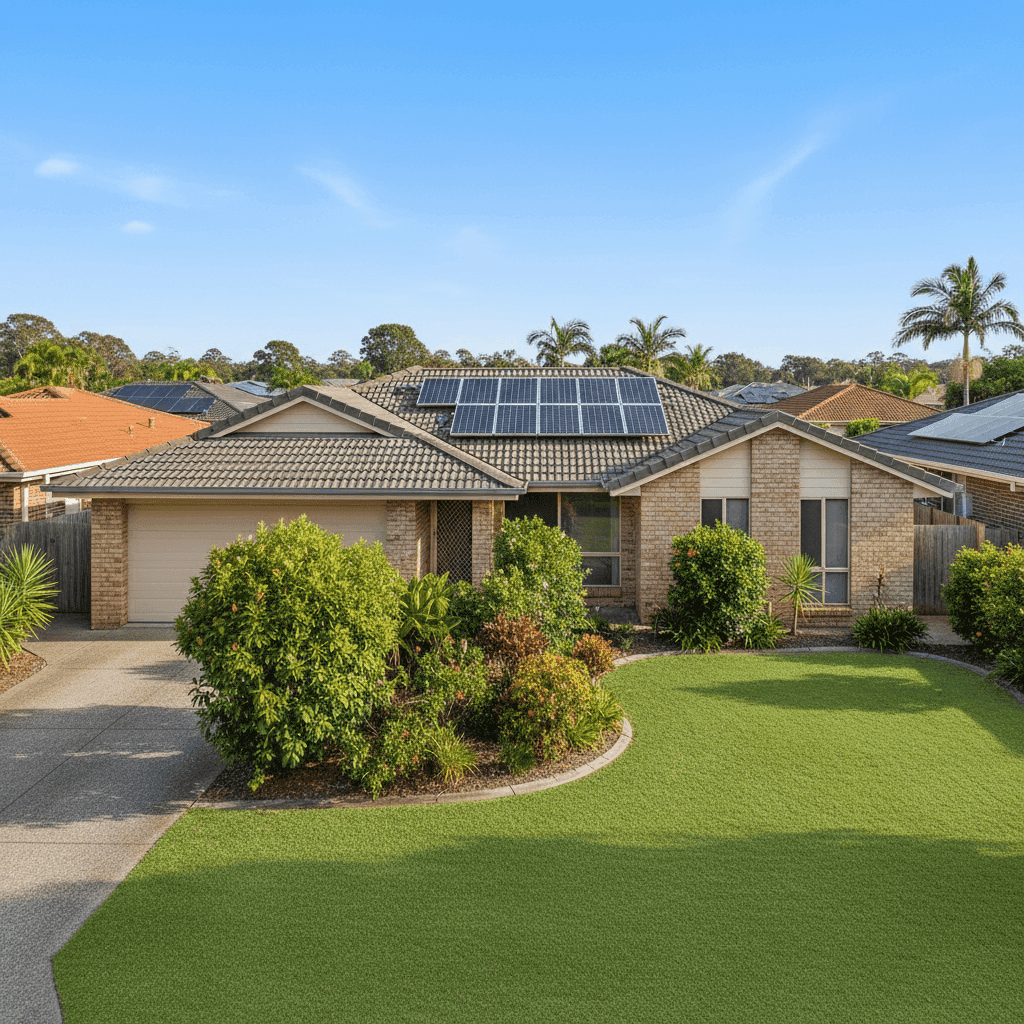

Property Features That Affect Your Premium

Several characteristics of this property influence how insurers price the risk — some favourably, some less so.

Double Brick Walls & Tiled Roof

This property's double brick external walls are generally viewed positively by insurers. Double brick construction is robust, fire-resistant, and holds up well in storms compared to lightweight cladding or weatherboard. Combined with a tiled roof, the building has a solid, durable profile that can attract more competitive premiums.

Slab Foundation

A concrete slab foundation is a common and generally low-risk foundation type in Queensland. It avoids some of the moisture and pest-related issues associated with raised timber stumps, which is a mild positive from an underwriting perspective.

Solar Panels

This property has solar panels, which are worth noting. While they add value to the home, solar panels need to be accounted for in your building sum insured — they're typically considered part of the building and should be included in that figure. Damage from storms or hail is a real risk in South East Queensland, so confirming your insurer covers solar panels under the building policy is essential.

Ducted Climate Control

Ducted air conditioning is a significant fixed installation. Like solar panels, it forms part of the building and contributes to the overall replacement cost. At 325 sqm, this is a sizeable home, and the ducted system adds meaningful value that should be reflected in the building sum insured.

Timber & Laminate Flooring

Timber and laminate flooring can be more susceptible to water damage than tiles, which is a minor risk factor — particularly relevant in Queensland's wet season. Ensuring your policy has adequate water damage cover (including escape of liquid) is worth checking.

No Pool

The absence of a pool removes a common liability risk and associated premium loading, which is a small but positive factor.

---

Tips for Homeowners in Oxenford

1. Review your building sum insured regularly At $653,000, the building sum insured needs to reflect the true cost of rebuilding — not the market value of the property. With a 325 sqm home featuring double brick construction, ducted air conditioning, and solar panels, rebuilding costs can escalate quickly. Use a building calculator or speak with a quantity surveyor to make sure you're not underinsured.

2. Confirm solar panel and ducted system coverage Ask your insurer explicitly whether solar panels and ducted climate control are covered under the building policy, and whether there are any sub-limits. Some policies cap coverage for these items or exclude storm damage to solar systems under certain conditions.

3. Consider a higher excess to reduce your premium The current excess is set at $1,000 for both building and contents. If you're in a strong financial position to absorb a larger out-of-pocket cost in a claim, increasing your excess to $2,000 or more can meaningfully reduce your annual premium.

4. Shop around — even a "fair" quote can be beaten A "Fair" rating means you're not overpaying significantly, but it also means there's room to do better. With the suburb's 25th percentile sitting at $2,357/yr, there are cheaper options available for comparable cover. Running a comparison takes minutes and could save you $400+ annually.

---

Compare Your Options at CoverClub

Whether you're renewing your existing policy or insuring a new home, it pays to compare. CoverClub makes it easy to see how your quote stacks up against real data from your suburb, your state, and across Australia. Get a home insurance quote today and find out if you're getting the best deal available for your Oxenford property.