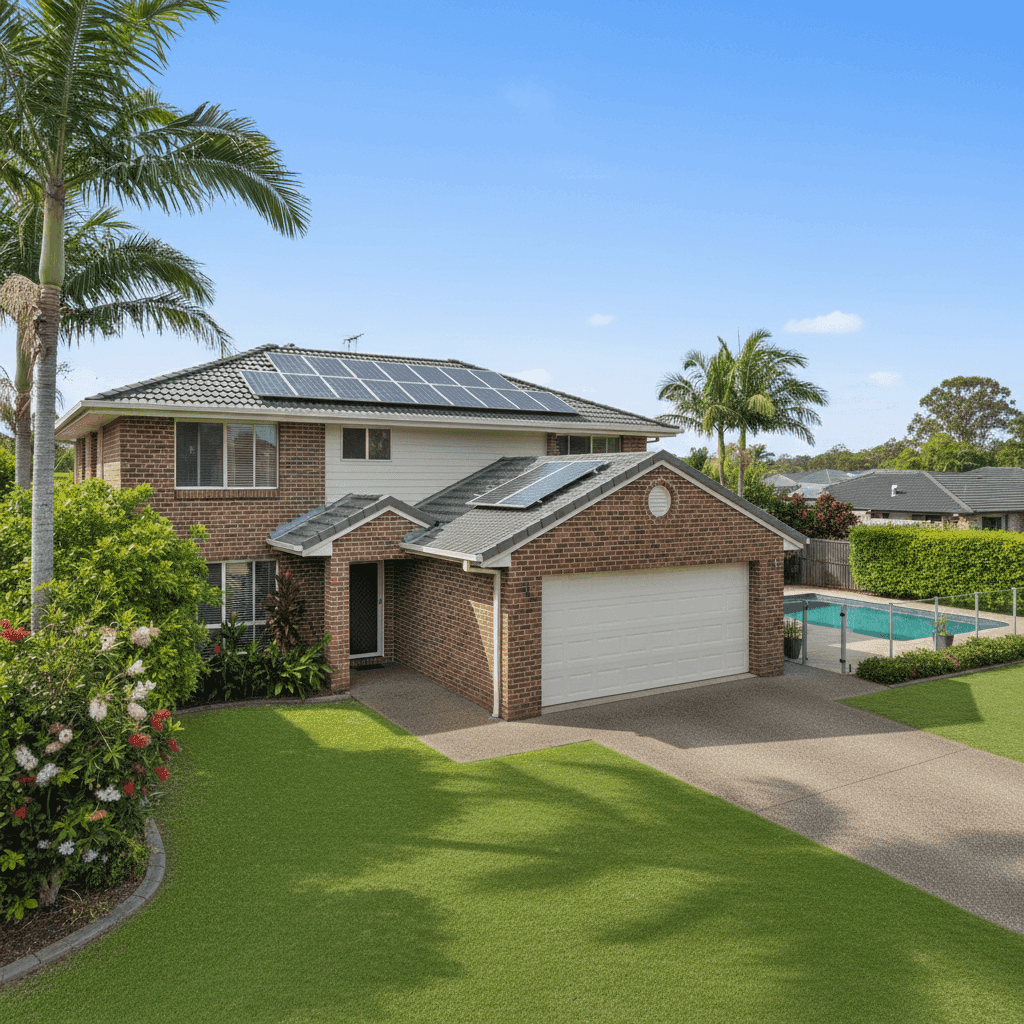

If you own a four-bedroom free standing home in Oxenford, QLD 4210, you're likely curious about whether your home insurance premium stacks up against what your neighbours are paying — and what the broader market looks like. Oxenford sits in the heart of the Gold Coast, a region known for its lifestyle appeal, strong property values, and a home insurance market that can vary significantly from street to street. This article breaks down a real quote of $3,233 per year (or $303/month) for a home and contents policy on a brick veneer property in the suburb, and puts it into context using data from CoverClub's Oxenford insurance statistics.

---

Is This Quote Fair?

The short answer: yes, broadly speaking. CoverClub rates this quote as Fair (Around Average), and the numbers back that up.

At $3,233 annually, this premium sits just below the suburb median of $3,274/yr — meaning roughly half of comparable quotes in Oxenford come in higher than this figure, and half come in lower. It's not a bargain-basement price, but it's also well clear of the suburb's 75th percentile at $4,722/yr, which is where premiums start to look genuinely expensive.

For a property insured at $677,000 for the building and $50,000 for contents, with a $1,000 excess on each, this is a reasonable position to be in. The coverage is substantial — particularly the building sum insured, which reflects current rebuild costs rather than market value — and the premium reflects that scope of cover without veering into overpriced territory.

That said, "fair" doesn't mean you can't do better. The suburb's 25th percentile sits at $2,357/yr, which tells us that a meaningful portion of Oxenford homeowners are securing comparable cover for noticeably less. It's worth understanding what drives the difference.

---

How Oxenford Compares

Context is everything when assessing an insurance premium. Here's how this quote measures up across different geographic levels:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Oxenford (suburb) | $4,299/yr | $3,274/yr |

| Queensland (state) | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

| Gold Coast LGA | $8,161/yr | — |

A few things stand out here. First, Queensland's average premium of $9,129/yr is dramatically higher than the median of $3,903/yr — a sign that the state's average is being pulled upward by high-risk properties, particularly those in cyclone-prone or flood-affected areas. Oxenford, by comparison, is not classified as a cyclone risk area, which is a meaningful factor keeping premiums more moderate.

Second, the Gold Coast LGA average of $8,161/yr might seem alarming at first glance, but again, this average is skewed by coastal and waterfront properties that carry substantially higher risk profiles. Oxenford is an inland suburb, and that geography works in its favour.

For a deeper look at how Queensland premiums are distributed, visit CoverClub's QLD insurance stats, or explore national home insurance benchmarks to see how your state compares to the rest of Australia.

---

Property Features That Affect Your Premium

Every home is different, and insurers price risk based on a range of property characteristics. Here's how the features of this particular Oxenford home influence its premium:

Brick Veneer Walls & Tiled Roof Brick veneer is generally well-regarded by insurers. It's more fire-resistant than timber weatherboard and holds up well in storms. Combined with a tiled roof — another durable, low-maintenance material — this property presents a relatively low structural risk profile. These features typically attract more competitive premiums compared to homes with lightweight cladding or metal roofing.

Slab Foundation A concrete slab foundation is standard for Queensland homes built in the 2000s and is considered a stable, low-risk foundation type. It eliminates the risk of subfloor issues that can affect older homes on stumps or piers.

Swimming Pool Pools are a beloved Gold Coast staple, but they do add a layer of liability risk that insurers account for. If someone is injured in or around your pool, your home insurance (specifically the liability component) may be called upon. Ensuring your policy includes adequate liability cover is important for pool owners.

Solar Panels Solar panels are increasingly common on Queensland rooftops, but they're not always automatically covered under a standard building policy. It's worth confirming with your insurer that your panels — and any associated inverter equipment — are included in your sum insured. If they were added after the original policy was written, they may need to be explicitly listed.

Ducted Climate Control Ducted air conditioning is a fixed installation and is typically covered under the building component of your policy. However, like solar panels, it's worth confirming the system is reflected in your building sum insured, as it can represent a significant replacement cost.

Construction Year: 2003 At just over two decades old, this home is relatively modern by insurance standards. Newer homes tend to benefit from more consistent construction quality, compliant electrical systems, and updated plumbing — all of which reduce the likelihood of claims related to building defects or ageing infrastructure.

---

Tips for Homeowners in Oxenford

1. Review your building sum insured regularly Construction costs have risen sharply in recent years. A sum insured of $677,000 may have been appropriate when the policy was first taken out, but it's worth checking against current rebuild cost estimators to ensure you're not underinsured. Many insurers offer tools to help with this.

2. Confirm solar panels and fixed systems are covered As mentioned above, solar panels and ducted systems can sometimes fall through the cracks in a policy. Ask your insurer directly whether these are included in your building cover, and for what value.

3. Shop around — even if your current premium seems reasonable A "fair" rating means you're not being gouged, but it doesn't mean you're getting the best deal available. With the suburb's 25th percentile at $2,357/yr, there's potential to save several hundred dollars annually by comparing quotes from multiple insurers. Use CoverClub to compare home insurance quotes in minutes.

4. Consider your excess strategically Both the building and contents excess on this policy sit at $1,000. Opting for a higher excess (say, $1,500 or $2,000) can meaningfully reduce your annual premium — provided you're comfortable covering that amount out of pocket in the event of a claim. For homeowners with solid emergency savings, this trade-off often makes financial sense.

---

Compare Your Home Insurance Today

Whether you're reviewing an existing policy or shopping for cover on a new property, CoverClub makes it easy to see what the market has to offer. Our platform aggregates real quote data so you can benchmark your premium against what others in Oxenford — and across Queensland — are actually paying. Get a home insurance quote today and find out if you could be paying less for the same level of protection.