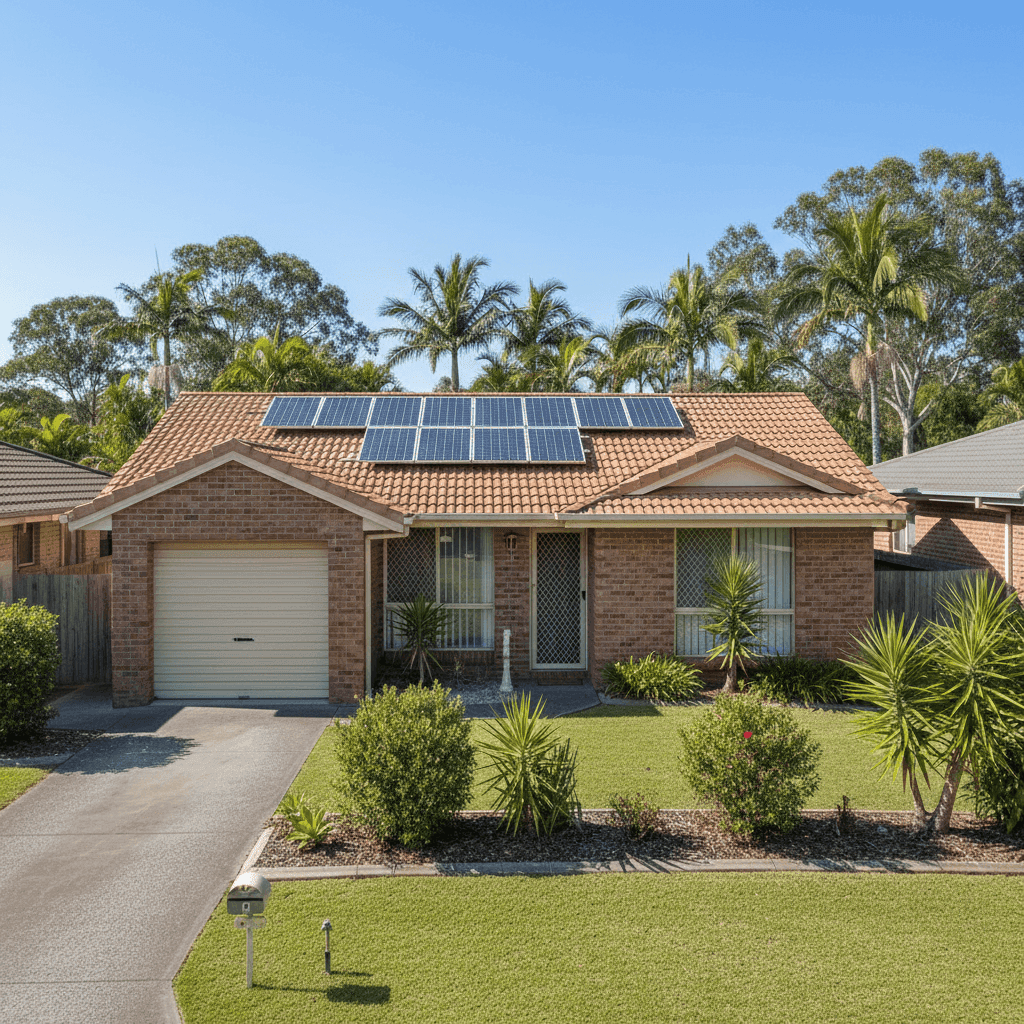

Oxenford, nestled in the northern Gold Coast corridor of Queensland, is a well-established suburb popular with families and downsizers alike. If you own a semi detached home here, understanding what you should be paying for building insurance — and why — can make a real difference to your hip pocket. This article breaks down a recent building-only insurance quote for a 2-bedroom, 1-bathroom semi detached property in Oxenford (postcode 4210), and puts the numbers into context against local, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question comes in at $2,583 per year (or around $248 per month) for building-only cover, with a $1,000 building excess and a sum insured of $850,000.

Our price rating for this quote is FAIR — Around Average.

That rating reflects a genuinely competitive position. Based on data from 121 quotes collected for Oxenford, the suburb's 25th percentile sits at $2,357/yr — meaning roughly three-quarters of comparable quotes in the area cost more than this one. At $2,583/yr, this quote is sitting just above the cheapest quarter of the market, which is a solid result for a property of this profile.

To put it plainly: you're not getting a rock-bottom bargain, but you're also not being overcharged. For a brick veneer semi detached with solar panels and above-average fittings on the Gold Coast, landing near the lower end of the pricing range is a reasonable outcome.

---

How Oxenford Compares

The numbers tell an interesting story when you zoom out:

| Benchmark | Premium |

|---|---|

| This quote | $2,583/yr |

| Oxenford suburb average | $4,299/yr |

| Oxenford suburb median | $3,274/yr |

| Gold Coast LGA average | $8,161/yr |

| QLD state average | $9,129/yr |

| QLD state median | $3,903/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

A few things stand out here. The Queensland state average of $9,129/yr is dramatically higher than what most Oxenford homeowners are actually paying — that figure is heavily skewed by high-risk coastal and cyclone-prone areas further north in the state. The QLD median of $3,903/yr is a more meaningful yardstick, and this quote sits comfortably below it.

Compared to the national picture, the quote also fares well — it's below both the national average ($5,347/yr) and the national median ($2,764/yr) is close, but this quote edges just below it too, which is encouraging.

The Gold Coast LGA average of $8,161/yr might raise eyebrows, but this is again influenced by higher-value properties and more exposed coastal locations within the broader Gold Coast region. Oxenford itself, being further inland and outside designated cyclone risk zones, benefits from a more moderate risk profile.

---

Property Features That Affect Your Premium

Several characteristics of this property work in the homeowner's favour when it comes to pricing:

Brick Veneer Walls & Tiled Roof Brick veneer construction is generally well-regarded by insurers for its durability and fire resistance. Combined with a tiled roof, this property presents a lower risk profile than, say, a weatherboard home with a metal sheet roof. These materials tend to attract more competitive premiums.

Slab Foundation A concrete slab foundation is considered stable and low-maintenance by underwriters, particularly in Queensland's subtropical climate. It reduces the risk of subsidence-related claims compared to older stumped or pier foundations.

Solar Panels The property has solar panels installed, which adds a modest layer of complexity to a building insurance policy. Solar systems are typically covered under building insurance as a fixed fixture, but it's worth confirming with your insurer that the panels and inverter are explicitly included — and that the sum insured accounts for their replacement cost.

Above-Average Fittings With above-average fittings quality, the $850,000 sum insured reflects the cost of rebuilding to a higher standard. This is appropriate — underinsurance is one of the most common and costly mistakes homeowners make. Fittings such as stone benchtops, quality cabinetry, and premium flooring (timber/laminate in this case) all add to the rebuild cost.

Construction Year: 1991 At over 30 years old, the property is past its first major maintenance cycle. Insurers may factor in the age of plumbing, electrical systems, and roofing when pricing risk. Keeping up with maintenance and being able to demonstrate this can support favourable renewal terms.

No Pool, No Cyclone Risk Zone The absence of a pool removes a liability risk that can nudge premiums upward. Being outside a designated cyclone risk area is a meaningful advantage for Queensland homeowners — cyclone cover is a significant cost driver in northern parts of the state.

---

Tips for Homeowners in Oxenford

1. Review Your Sum Insured Annually Construction costs in South East Queensland have risen considerably in recent years. A sum insured set even two or three years ago may no longer reflect the true cost of rebuilding your home. Use a building cost calculator or speak with a quantity surveyor to make sure your $850,000 coverage is still adequate — especially with above-average fittings in the mix.

2. Confirm Solar Panel Coverage Not all building policies automatically cover solar panel systems to their full replacement value. Check your Product Disclosure Statement (PDS) to confirm your panels and inverter are listed as insured items, and that the sum insured is sufficient to replace them at current market rates.

3. Compare at Renewal, Not Just at Inception Insurance loyalty rarely pays off in Australia. Premiums can shift significantly between insurers year to year. Given that the suburb average is $4,299/yr and this quote came in at $2,583/yr, there's clearly wide variation in the market — which means shopping around at renewal time is genuinely worthwhile.

4. Consider a Higher Excess to Reduce Premiums The current excess is set at $1,000. If you have a financial buffer and rarely make small claims, increasing your excess to $2,000 or more can reduce your annual premium. Just make sure the saving justifies the additional out-of-pocket cost in the event of a claim.

---

Compare Your Own Quote

Curious how your home insurance stacks up? CoverClub makes it easy to benchmark your current premium against real quotes from across your suburb, the Gold Coast, and beyond. Whether you're coming up for renewal or just bought a property in Oxenford, it pays to know where you stand. Get a quote and compare today — it only takes a few minutes and could save you hundreds.