If you own a four-bedroom free standing home in Pacific Pines, QLD 4211, you're likely paying close attention to rising insurance costs. This leafy Gold Coast hinterland suburb sits in a region where premiums can vary enormously depending on your property's construction, elevation, and proximity to flood-prone land. In this article, we break down a real home and contents insurance quote for a weatherboard home in Pacific Pines — and help you decide whether it represents fair value.

---

Is This Quote Fair?

The quote in question comes in at $3,904 per year (or $374/month) for a combined home and contents policy, covering a building sum insured of $987,000 and contents valued at $50,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is Expensive (Above Average).

To understand why, it helps to look at the local context. Across 57 quotes collected for Pacific Pines (postcode 4211), the suburb average sits at $3,347/yr and the median is $2,880/yr. This quote lands above the 75th percentile threshold of $3,620/yr — meaning it's pricier than at least three-quarters of comparable quotes in the area.

That said, "expensive" doesn't automatically mean "wrong." A high sum insured of nearly $1 million for the building, combined with above-average fittings quality, will naturally push a premium upward. The question worth asking is whether you can achieve similar coverage at a lower price point with a different insurer.

---

How Pacific Pines Compares

Understanding where Pacific Pines sits relative to broader benchmarks puts this quote in sharper perspective.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Pacific Pines (4211) | $3,347/yr | $2,880/yr |

| Queensland (State) | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

| Scenic Rim LGA | $8,744/yr | — |

A few things stand out here. Queensland's state average of $9,129/yr is dramatically higher than the national average of $5,347/yr — a reflection of the outsized impact that cyclone, flood, and storm risk has on premiums across regional and coastal QLD. However, the state median of $3,903/yr tells a more nuanced story: most Queensland homeowners are actually paying closer to $3,900/yr, with a smaller number of very high-risk properties pulling the average up significantly.

Interestingly, the quote being analysed ($3,904/yr) is almost exactly in line with the Queensland state median — which means it's not out of step with what most Queenslanders pay, even if it's above the local Pacific Pines average.

The Scenic Rim LGA average of $8,744/yr is also worth noting. This figure captures a much broader area that includes rural and flood-exposed properties, so it's not a direct comparison — but it does illustrate that Pacific Pines homeowners are generally getting a better deal than many of their LGA neighbours.

Explore more data at our Pacific Pines suburb stats page, the Queensland state overview, or the national home insurance stats.

---

Property Features That Affect Your Premium

This particular property has a number of characteristics that insurers weigh carefully when calculating risk. Here's how each one is likely influencing the premium:

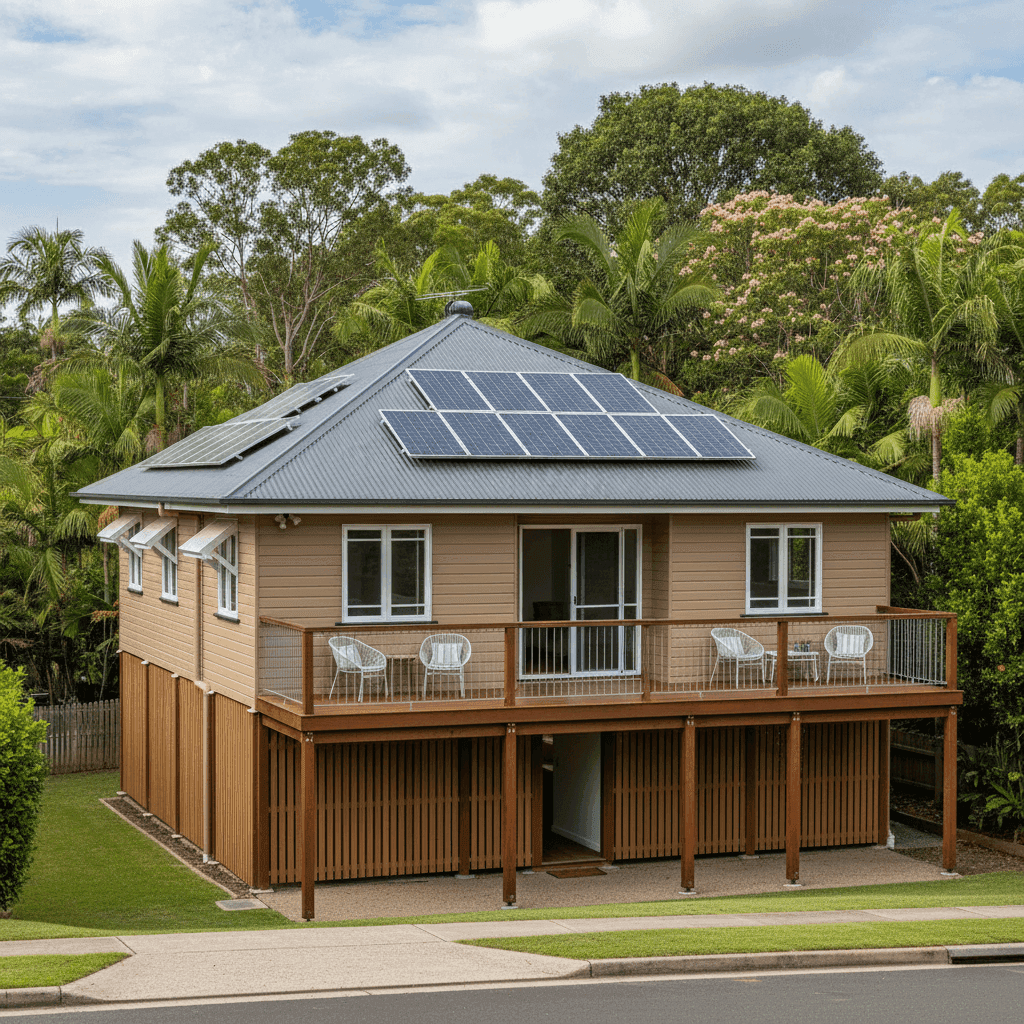

Weatherboard Timber Walls

Weatherboard construction is common in older Queensland homes and is generally considered a higher-risk material than brick veneer or full brick. Timber is more susceptible to fire, termite damage, and general deterioration, which typically results in a moderately higher premium compared to masonry construction.

Steel/Colorbond Roof

Colorbond roofing is viewed favourably by most insurers. It's durable, resistant to corrosion, and performs well in high-wind events — all of which can help keep premiums in check relative to older tile or fibrous cement roofing.

Elevated on Poles

The home is elevated by at least one metre on poles — a classic Queensland architectural feature. Elevation provides meaningful flood protection by keeping the living areas above ground-level water ingress. Insurers generally recognise this as a risk-reducing feature, particularly in areas with any history of localised flooding.

Timber/Laminate Flooring

Flooring type matters when assessing reinstatement costs. Timber and laminate floors are mid-range in terms of replacement cost, though they can be more susceptible to water damage than tiles — a consideration in storm-prone regions.

Above-Average Fittings Quality

Above-average fittings — think stone benchtops, quality appliances, and premium fixtures — increase the cost to rebuild or repair, which directly lifts the building sum insured and, in turn, the premium. This is a legitimate driver of cost and reflects the real value of the home.

Solar Panels

Solar panels add replacement value to the building and introduce a small amount of additional risk (electrical faults, storm damage to panels). Most insurers include them under building cover, but their presence can nudge the premium slightly higher.

Construction Year: 1994

At 30 years old, this home sits in a middle ground — past the point where new-build defects are a concern, but old enough that some components (wiring, plumbing, roofing) may be approaching the end of their serviceable life. Insurers may factor this into their risk assessment.

---

Tips for Homeowners in Pacific Pines

If you're looking to get better value on your home and contents insurance in Pacific Pines, here are four practical steps worth taking:

- Review your sum insured regularly. A building sum insured of $987,000 is substantial. Make sure it reflects the actual cost to rebuild — not the market value of the land. Overinsuring can mean you're paying unnecessarily high premiums, while underinsuring leaves you exposed. Tools like a quantity surveyor report or an online rebuild calculator can help you calibrate this figure accurately.

- Shop around at renewal time. Loyalty rarely pays in the insurance market. Insurers routinely offer better rates to new customers, so comparing quotes before your policy renews is one of the most effective ways to reduce your annual cost. Even a modest saving of $300–$500/yr compounds significantly over time.

- Consider a higher excess. If you have the financial buffer to absorb a larger out-of-pocket cost in the event of a claim, opting for a higher excess (say, $2,000 instead of $1,000) can meaningfully reduce your annual premium. Just make sure the saving justifies the increased risk you're taking on.

- Ask about discounts for security and safety features. Some insurers offer premium reductions for homes with monitored alarm systems, deadbolts, or smoke detectors. Given the above-average fittings in this property, it's worth confirming with your insurer whether any applicable discounts have been applied.

---

Find a Better Deal with CoverClub

Whether you're renewing soon or simply curious about what else is on the market, CoverClub makes it easy to compare home and contents insurance quotes tailored to your property. Our platform analyses real quote data from across Australia so you can make an informed decision — not just accept the first number that lands in your inbox.

Get a home insurance quote for your Pacific Pines property →