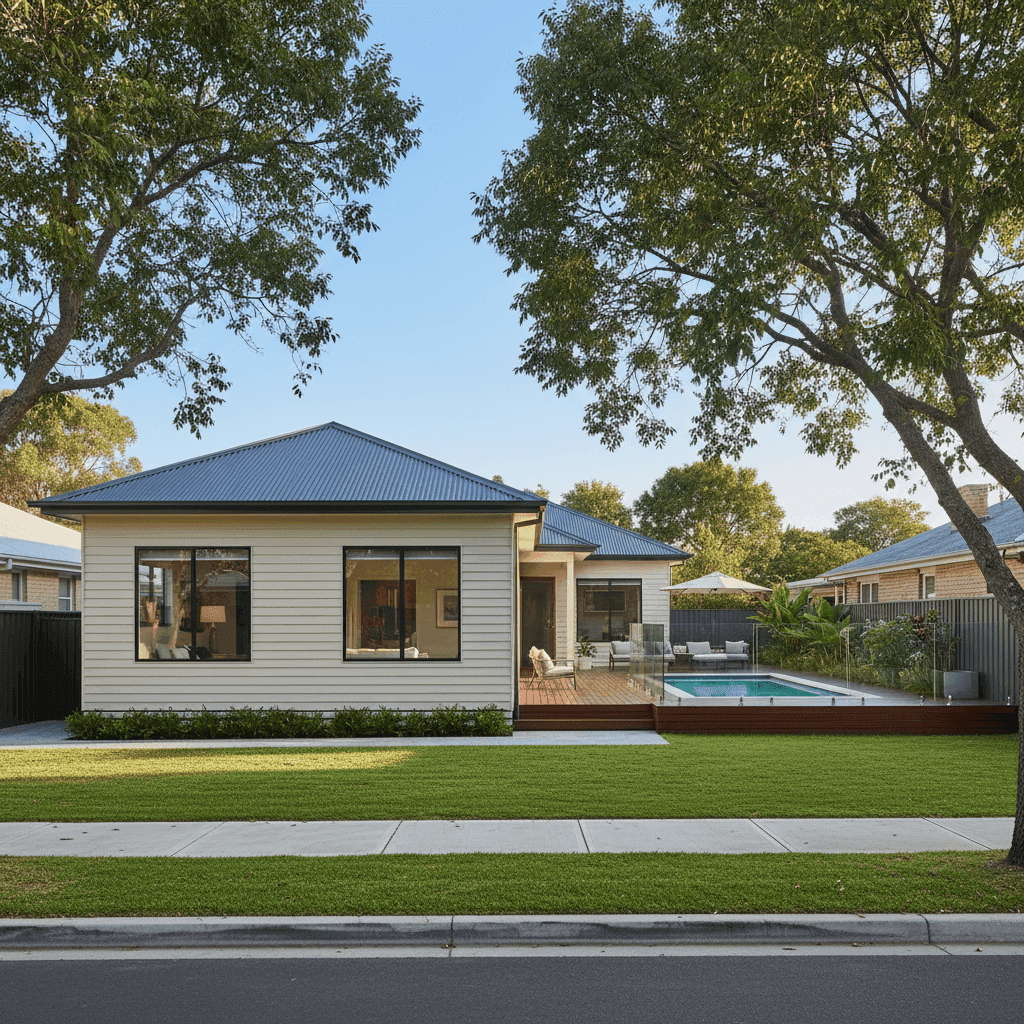

Padstow Heights is a quiet, leafy suburb in Sydney's south-west, known for its elevated streets, established homes, and family-friendly feel. But when it comes to insuring a four-bedroom free standing home here, homeowners can face some surprisingly varied premiums. This article breaks down a real home and contents insurance quote for a property in the area — examining whether it represents fair value, how it stacks up against local and national benchmarks, and what property-specific factors are likely driving the cost.

---

Is This Quote Fair?

The quote in question sits at $3,809 per year (or $365 per month) for combined home and contents cover, with a building sum insured of $847,000 and contents valued at $71,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is Expensive — Above Average.

To put that in context: the suburb average premium for Padstow Heights sits at just $2,016 per year, with a median of $1,962. This quote comes in at nearly double the local median, which is a significant gap worth understanding.

That said, it's important not to read too much into a single comparison point. The suburb sample size here is 14 quotes — a reasonable snapshot, but not enormous. Premiums vary considerably depending on the specific property, the insurer, the level of cover, and the sum insured. A $847,000 building sum insured is on the higher end for the area, and that alone will push the premium upward compared to properties insured for less.

---

How Padstow Heights Compares

Here's how this quote sits across different geographic benchmarks:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Padstow Heights (suburb) | $2,016/yr | $1,962/yr |

| NSW (state) | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

| Canterbury-Bankstown LGA | $9,344/yr | — |

At first glance, Padstow Heights looks like a relatively affordable suburb to insure in — and compared to the broader NSW state average of $9,528, it genuinely is. The LGA average for Canterbury-Bankstown is similarly elevated at $9,344, which suggests that some postcodes within the council area carry significantly higher risk profiles than Padstow Heights itself.

Compared to the national average of $5,347, this quote is below average — which is a more reassuring comparison. And against the national median of $2,764, it's roughly 38% higher, which aligns with the "expensive" rating relative to the suburb but looks more reasonable in a broader context.

The takeaway: this quote is expensive for Padstow Heights, but not outlandish when viewed against NSW and national figures — particularly given the property's characteristics.

---

Property Features That Affect Your Premium

Several features of this property are likely contributing to a higher-than-average premium. Understanding these can help you make sense of the cost — and potentially address some of them.

Weatherboard Timber Walls

Weatherboard construction is common in older Sydney suburbs, and this home — built in 1975 — is a classic example. Timber-clad homes are generally considered higher risk by insurers due to their susceptibility to fire and rot compared to brick veneer or full brick construction. This is one of the more significant factors pushing the premium upward.

Stump Foundation

Homes built on stumps (also called pier or post foundations) can be more vulnerable to movement, subsidence, and pest damage over time. Insurers factor this into their risk assessment, particularly for older homes where the stumps may be original timber rather than concrete or steel.

Swimming Pool

A pool adds both value and liability to a property. From an insurance perspective, pools increase the risk of accidental damage claims and can also affect public liability considerations. It's a relatively modest premium driver, but it's a factor nonetheless.

Age of Construction (1975)

A home approaching its 50th year carries inherent risks around ageing infrastructure — plumbing, wiring, roofing materials, and structural components. Insurers price older homes accordingly, especially when the sum insured is high enough to cover full replacement in today's market.

Ducted Climate Control

Ducted air conditioning systems are a premium item that increases the contents and building replacement cost. If the system is integrated into the building (as most ducted systems are), it contributes to the overall building sum insured — which at $847,000 is already substantial.

Colorbond Roof

On the positive side, a steel Colorbond roof is generally viewed favourably by insurers. It's durable, fire-resistant, and low-maintenance compared to terracotta tiles or older corrugated iron. This likely provides a modest offset against some of the other risk factors.

---

Tips for Homeowners in Padstow Heights

If you're looking to manage your home insurance costs without compromising on cover, here are some practical steps worth considering:

- Review your sum insured carefully. A building sum insured of $847,000 is significant. Make sure this reflects the actual cost to rebuild the home (not its market value), including demolition and debris removal. Overinsuring inflates your premium unnecessarily, while underinsuring leaves you exposed. Use a building cost calculator or get a professional assessment.

- Ask about discounts for security upgrades. Installing an alarm system, deadbolts, or a monitored security system can attract discounts with many insurers. Given the age of the home, it's worth checking whether your current security measures meet modern standards.

- Consider your excess strategically. Both excesses on this policy are set at $1,000. Opting for a higher excess (say, $2,000 or $2,500) can meaningfully reduce your annual premium. If you're unlikely to make small claims, this trade-off often makes financial sense.

- Compare quotes annually. Insurance loyalty rarely pays off. Premiums can shift significantly from year to year, and different insurers assess risk differently — especially for older, character-style homes like weatherboard properties. Use a comparison platform like CoverClub to benchmark your renewal quote before you accept it.

---

Compare Your Options with CoverClub

Whether you're renewing an existing policy or shopping for cover on a new purchase, it pays to see what's available across the market. CoverClub makes it easy to compare home and contents insurance quotes for properties across Padstow Heights and beyond — so you can make a confident, informed decision rather than simply rolling over your existing policy.

Get a quote today at CoverClub and see how your premium stacks up.