Pallarenda is a quiet coastal suburb sitting on the northern edge of Townsville, known for its relaxed beachside lifestyle and proximity to the Great Barrier Reef Marine Park. It's a sought-after pocket of North Queensland — but like much of the region, it comes with some unique insurance considerations. This article breaks down a real home and contents insurance quote for a four-bedroom free standing home in Pallarenda (QLD 4810), examines how it stacks up against local, state, and national benchmarks, and offers practical tips for homeowners looking to get the best value cover.

---

Is This Quote Fair?

The annual premium for this property came in at $5,911 per year (or $519/month), covering a building sum insured of $816,000 and contents valued at $210,000. Our pricing engine rates this quote as CHEAP — below average for the area.

That's genuinely good news for the homeowner. North Queensland is notoriously one of the most expensive regions in Australia for home insurance, largely due to cyclone exposure and the associated reinsurance costs that insurers pass on to policyholders. To land a below-average premium in this environment is a meaningful result.

The building excess sits at $5,000, which is on the higher side and worth factoring into your thinking. A higher excess is one of the levers insurers use to bring premiums down — so while the annual cost looks attractive, you'd be carrying more out-of-pocket risk in the event of a claim. The contents excess of $1,000 is more standard.

Overall, this quote represents solid value given the property's location, size, and the breadth of cover provided.

---

How Pallarenda Compares

There's no suburb-level pricing data available for Pallarenda specifically, but we can draw meaningful comparisons using state-wide QLD data and national benchmarks.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| This Quote | $5,911/yr | — |

| LGA (Townsville) Average | $7,340/yr | — |

| QLD State Average | $9,129/yr | $3,903/yr |

| National Average | $5,347/yr | $2,764/yr |

A few things stand out here:

- This quote is 19% below the Townsville LGA average of $7,340/yr — a significant saving for a property of this size and specification.

- It's 35% below the QLD state average of $9,129/yr, which reflects just how elevated premiums can get across the broader state (particularly in higher-risk coastal and cyclone-prone areas).

- It sits just 11% above the national average of $5,347/yr — remarkably competitive for a North Queensland property in a declared cyclone risk zone.

It's worth noting that the QLD state median of $3,903/yr is well below this quote, but medians are heavily influenced by lower-risk metropolitan areas like Brisbane and the Gold Coast. For a coastal Townsville suburb with cyclone exposure, a premium in the $5,000–$7,000 range is generally considered the norm. Coming in under $6,000 for this level of cover is a strong outcome.

You can explore more localised pricing data on the Pallarenda suburb stats page as our data set grows.

---

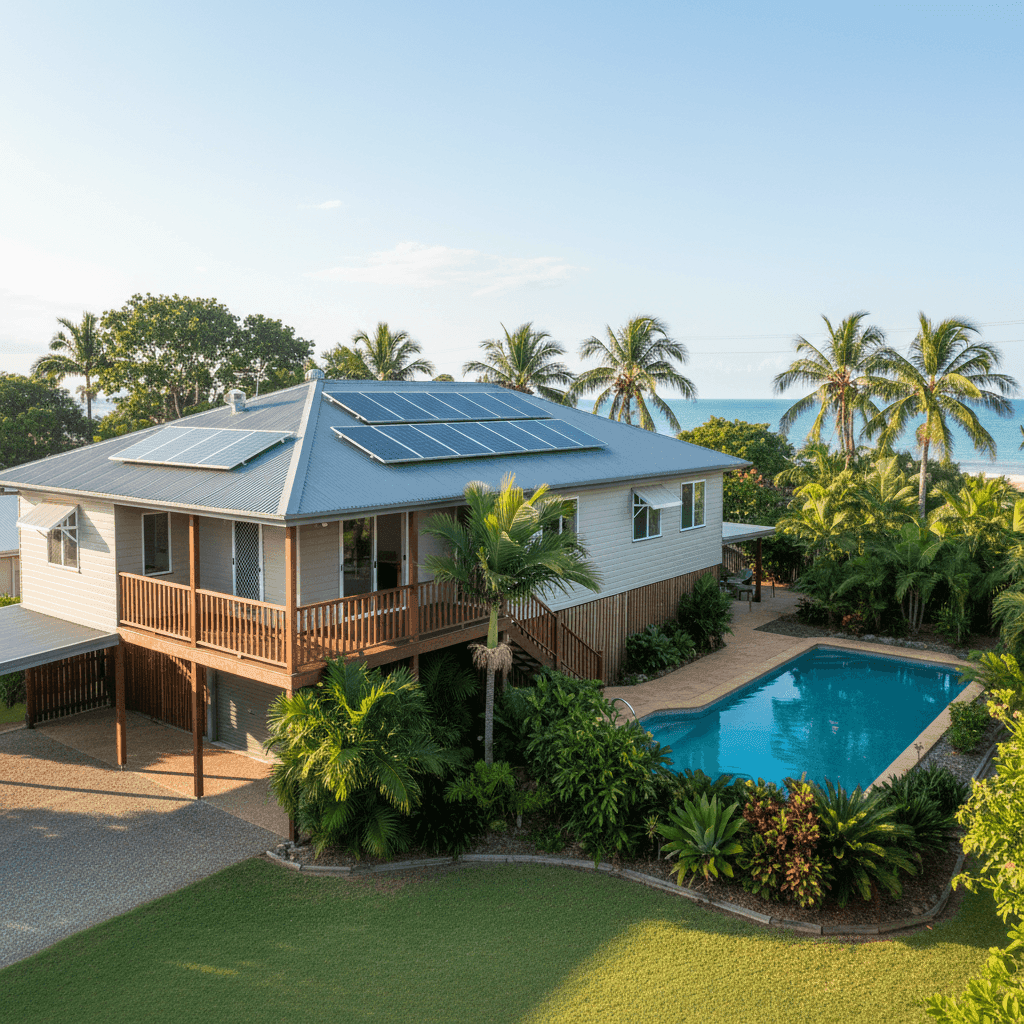

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on what insurers charge. Understanding them helps you make sense of your quote — and potentially negotiate a better one.

Cyclone Risk Zone

Pallarenda sits within a designated cyclone risk area, which is the single biggest driver of elevated premiums in North Queensland. Insurers price in the likelihood of wind, storm surge, and water damage events, as well as the cost of reinsurance in catastrophe-prone regions. This alone can add thousands to an annual premium compared with properties in southern states.

Construction: Hardiplank/Hardiflex Walls & Colorbond Roof

Fibre cement cladding (Hardiplank/Hardiflex) is generally viewed favourably by insurers — it's non-combustible, resistant to rot, and holds up well in tropical conditions. Combined with a steel Colorbond roof, this construction profile is considered durable and relatively low-risk, which likely contributes to the below-average premium.

Stumped Foundation & Elevated Design

The home is built on stumps and elevated by less than one metre — a classic Queensland construction style. Elevation can assist with flood resilience (water flows beneath rather than through the home), though insurers will assess the specific flood risk of the land itself. Stumped homes can also be more vulnerable to wind uplift during cyclone events, which may be factored into the rating.

Age of Construction (1960)

A home built in 1960 is over 60 years old. While older homes can have character and solid bones, insurers pay close attention to the age of key systems — roofing, plumbing, and electrical. Older wiring or plumbing can increase the risk of damage or failure. Ensuring these systems are well-maintained and up to current standards is important both for safety and for your insurance terms.

Pool, Solar Panels & Ducted Climate Control

These features increase the overall replacement value of the property, which is reflected in the $816,000 building sum insured. Solar panels, in particular, are an increasingly common consideration — they need to be covered for storm, hail, and cyclone damage. Ducted air conditioning systems are expensive to replace and are rightly included in the building sum insured calculation.

---

Tips for Homeowners in Pallarenda

1. Review Your Sum Insured Annually

Building costs in North Queensland have risen sharply in recent years, driven by labour shortages and supply chain pressures. Make sure your $816,000 sum insured reflects current rebuild costs — not just the market value of your home. Underinsurance is one of the most common and costly mistakes homeowners make.

2. Understand Your Cyclone Excess

Many policies in cyclone-declared areas apply a separate cyclone excess on top of the standard building excess. Check your Product Disclosure Statement (PDS) carefully — your effective out-of-pocket cost after a cyclone event could be significantly higher than the $5,000 standard excess shown in this quote.

3. Maintain Your Home Proactively

Insurers can reduce or deny claims where damage is attributed to lack of maintenance. In a tropical climate, this means regularly inspecting your roof fixings and flashings, clearing gutters, checking stump condition, and ensuring your solar panel mounting is secure. A well-maintained home is also a safer home.

4. Compare Quotes Before Renewal

Even if you're happy with your current premium, the home insurance market in Queensland is competitive — and pricing can shift significantly between insurers. Use a comparison platform like CoverClub to benchmark your renewal quote before automatically rolling over. A few minutes could save you hundreds of dollars.

---

Find the Right Cover for Your Home

Whether you're a long-term Pallarenda local or new to the area, making sure your home and contents are properly protected — at a fair price — is one of the most important financial decisions you'll make. CoverClub makes it easy to compare home insurance quotes from multiple insurers, so you can see exactly where your premium sits relative to the market.

Get a home insurance quote at CoverClub and find out if you're paying a fair price for your cover.