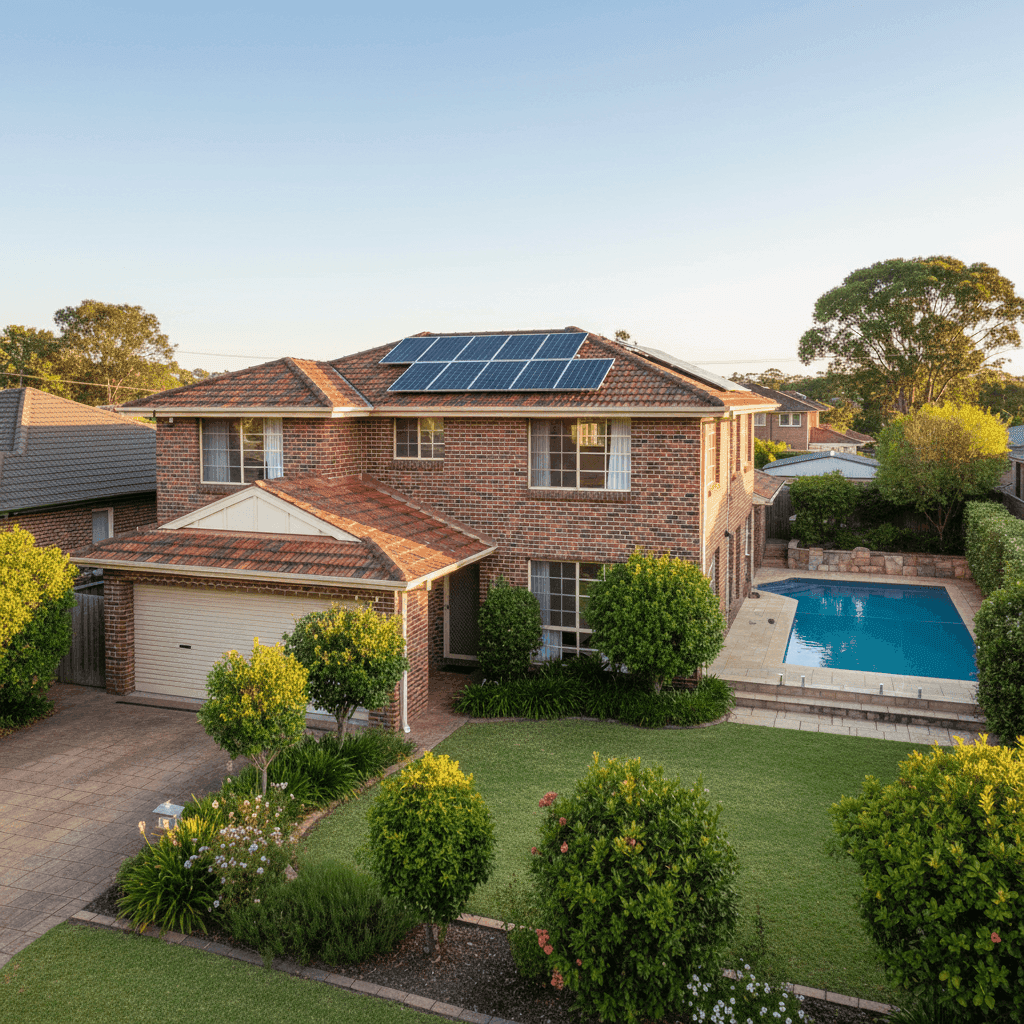

Panania is a well-established suburb in Sydney's south-west, sitting within the Canterbury-Bankstown local government area. It's a family-friendly pocket of the city known for its leafy streets and solid housing stock — and a four-bedroom, double brick free standing home here is a significant asset worth protecting. If you've recently received a home and contents insurance quote for a property like this, you might be wondering whether what you're paying is reasonable. Let's break it all down.

---

Is This Quote Fair?

The quote in question sits at $2,749 per year (or $276/month) for a combined home and contents policy, covering a building sum insured of $1,650,000 and contents valued at $216,000. The building excess is $3,000 and the contents excess is $1,000.

Our pricing analysis rates this quote as Fair — Around Average. That's a meaningful result. It means the premium isn't a bargain-basement outlier, but it's also not inflated. For a property of this size and specification — 268 sqm, above-average fittings, a pool, and solar panels — landing near the middle of the market is a solid outcome.

Compared to the suburb average of $3,259/year and the suburb median of $3,618/year, this quote comes in noticeably below both benchmarks. That's a saving of over $500 against the average and nearly $870 against the median. In practical terms, the homeowner is doing better than most of their neighbours with similar cover.

---

How Panania Compares

To put this quote in proper context, it helps to look at the broader picture. You can explore the full data on the Panania suburb insurance stats page, but here's a summary:

| Benchmark | Premium |

|---|---|

| This quote | $2,749/yr |

| Panania suburb average | $3,259/yr |

| Panania suburb median | $3,618/yr |

| Panania 25th percentile | $1,445/yr |

| Panania 75th percentile | $4,637/yr |

| NSW state average | $3,801/yr |

| NSW state median | $3,410/yr |

| National average | $2,965/yr |

| National median | $2,716/yr |

| Canterbury-Bankstown LGA average | $9,344/yr |

A few things stand out here. First, this quote sits below the NSW state average of $3,801/year by over $1,000 — a meaningful gap when you're talking about ongoing annual costs. Check out the NSW insurance stats for a deeper look at how premiums vary across the state.

Second, the Canterbury-Bankstown LGA average of $9,344/year looks startling at first glance. This figure is heavily influenced by high-risk properties across the broader LGA — particularly those in flood-prone areas — and shouldn't be taken as a typical expectation for Panania specifically. The suburb-level data tells a far more relevant story.

Third, when benchmarked against national averages, this quote is also competitive. The national average sits at $2,965/year and the national median at $2,716/year, placing this quote slightly below the national average — solid for a property of this calibre in metropolitan Sydney.

The spread within Panania itself is also worth noting. The 25th–75th percentile range runs from $1,445 to $4,637/year, which is a wide band. This reflects the diversity of properties and cover levels across the suburb, and underscores why comparing your own quote against multiple data points matters.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on how insurers price the risk:

Double brick construction is generally viewed favourably by insurers. It offers strong structural integrity, better fire resistance, and greater durability compared to timber or clad homes. This can contribute to more competitive premiums.

Tiled roof is another positive. Tiles are a durable, low-maintenance roofing material that holds up well in Sydney's climate, and insurers typically price tiled roofs more favourably than older materials like fibrous cement or corrugated iron.

Concrete slab foundation provides stability and reduces the risk of subsidence-related claims, which can be a factor in some parts of Sydney's south-west.

Swimming pool adds to the replacement cost of the property and introduces additional liability considerations. Pools are a factor in building sum insured calculations and can nudge premiums upward.

Solar panels are increasingly common on Australian homes, but they do add to the rebuild cost and require specific cover. Homeowners should confirm their policy explicitly covers solar panels — both the panels themselves and any damage they might cause to the roof during a storm event.

Above-average fittings mean that the cost to rebuild or repair the home to its existing standard is higher than a comparably sized home with standard finishes. This is reflected in the $1,650,000 building sum insured — a figure that should be reviewed regularly to ensure it keeps pace with construction cost inflation.

268 sqm floor area is a substantial home. At current construction rates in Sydney, rebuilding a home of this size and quality could easily exceed $1.5 million, so the sum insured appears well-calibrated.

---

Tips for Homeowners in Panania

1. Review your building sum insured annually Construction costs in Sydney have risen sharply in recent years. A sum insured that was adequate three years ago may no longer cover a full rebuild today. Use a building cost calculator or speak with a quantity surveyor to sense-check your figure each year.

2. Confirm your solar panels are explicitly covered Not all policies cover solar panels as a default inclusion. Check your Product Disclosure Statement (PDS) carefully to confirm your panels are covered for storm damage, fire, and accidental breakage — and that any damage they cause to the roof is also included.

3. Don't over-insure your contents, but don't under-insure either $216,000 in contents cover is a significant amount. It's worth doing a room-by-room inventory every couple of years to make sure this figure reflects what you actually own. Over-insuring wastes money; under-insuring leaves you exposed at claim time.

4. Compare quotes before renewal The wide premium range within Panania — from $1,445 to $4,637/year — shows that different insurers price the same risk very differently. Even if your current insurer has treated you well, it costs nothing to compare. A few minutes of research could save you hundreds.

---

Ready to Compare?

Whether you're reviewing an existing policy or shopping for the first time, comparing quotes is the smartest move you can make. Get a home insurance quote at CoverClub and see how your premium stacks up against the market — it only takes a few minutes and could save you significantly on your next renewal.