Paradise Point is one of the Gold Coast's most sought-after waterside suburbs — a quiet peninsula community in postcode 4216 where well-established homes sit close to canals, parks, and Moreton Bay. Insuring a free standing home here comes with its own set of considerations, from the area's coastal proximity to the age and construction of the property itself. This article breaks down a real home and contents insurance quote for a four-bedroom, three-bathroom free standing home in Paradise Point, compares it against local and national benchmarks, and offers practical guidance for homeowners looking to get the best value on their cover.

---

Is This Quote Fair?

The annual premium for this property came in at $4,313 per year (or around $406 per month), covering both building (sum insured: $886,000) and contents ($112,000), each with a $1,000 excess.

CoverClub's pricing engine has rated this quote as Fair — Around Average, and the data backs that up. When you look at the suburb-level statistics for Paradise Point (4216), the average premium across 126 quotes sits at $6,876 per year, with a median of $6,394. That means this quote is sitting noticeably below both the average and median for the area — a positive sign for the homeowner.

To be precise, this quote falls just above the 25th percentile for the suburb ($4,010/yr), meaning roughly three-quarters of comparable properties in Paradise Point are paying more. That's a reasonably strong position, though there is still room to explore whether a lower premium is achievable without sacrificing meaningful cover.

The "Fair" rating reflects the fact that while this quote beats the local average comfortably, it sits somewhat above state and national benchmarks — which is expected given Paradise Point's coastal location and the elevated rebuild costs associated with larger, older homes in the area.

---

How Paradise Point Compares

To put this quote in proper context, it helps to look at the numbers across three geographic levels:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Paradise Point (4216) | $6,876/yr | $6,394/yr |

| Gold Coast LGA | $5,494/yr | — |

| Queensland | $4,547/yr | $3,931/yr |

| National | $2,965/yr | $2,716/yr |

A few things stand out here. First, Paradise Point premiums are substantially higher than the Queensland average — roughly 51% above the state mean. This is consistent with what you'd expect from a coastal Gold Coast suburb, where flood risk, storm surge exposure, and high property values all push premiums upward.

Second, Queensland itself sits well above the national average of $2,965/yr — a reflection of the state's exposure to severe weather events including tropical storms, heavy rainfall, and hail. Homeowners moving to Queensland from southern states are often surprised by the jump in insurance costs.

You can explore how Queensland premiums compare more broadly across the state, or drill into the Paradise Point suburb data to see the full distribution of quotes in your area.

---

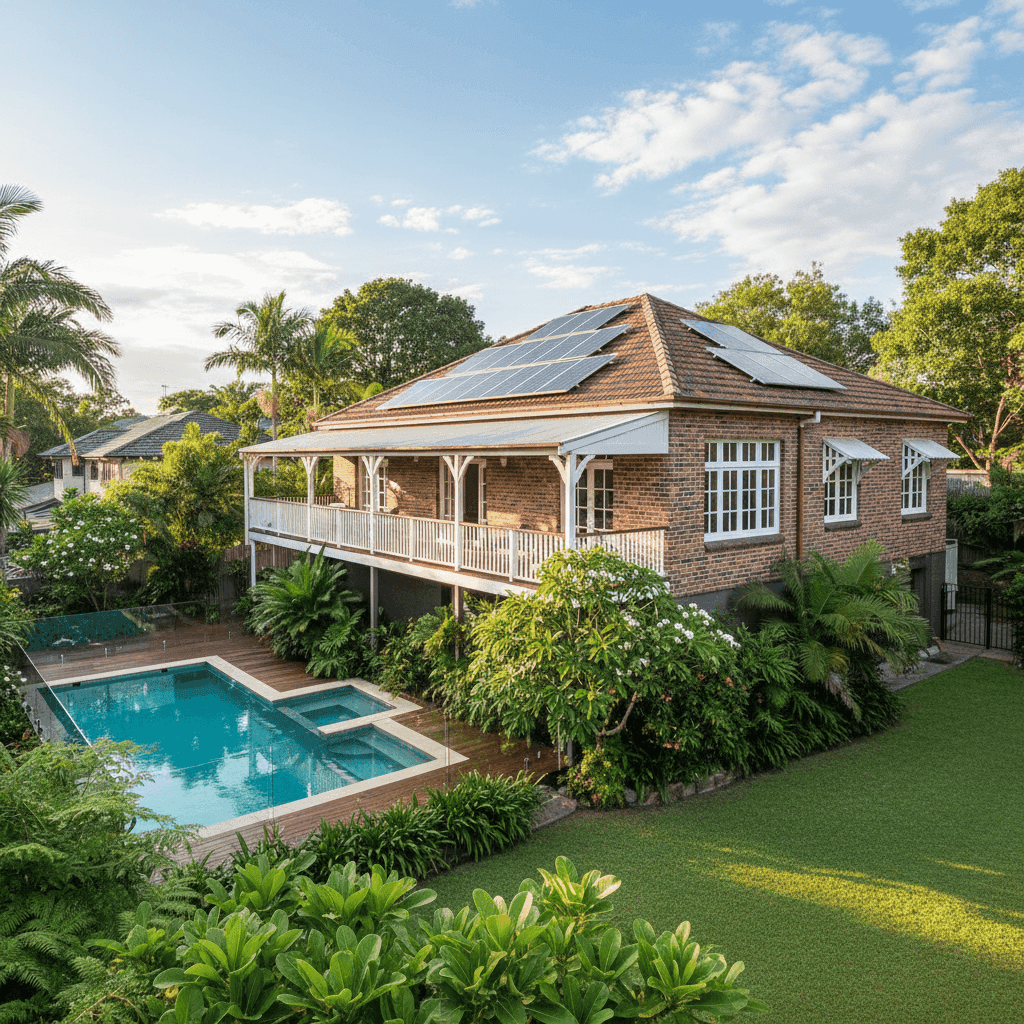

Property Features That Affect Your Premium

Every home is different, and insurers assess a range of property characteristics when calculating your premium. Here's how the key features of this particular property are likely influencing the quote:

Double Brick Construction Double brick walls are generally viewed favourably by insurers. They offer strong resistance to wind, fire, and impact damage compared to timber or clad construction. This is a meaningful advantage in a coastal suburb like Paradise Point where storm events are a real consideration.

Tiled Roof A terracotta or concrete tile roof is considered a moderate-to-good risk profile. Tiles are durable and fire-resistant, though they can crack under hail impact or significant storm debris. Compared to Colorbond or metal roofing, tiles sit in the mid-range for insurability.

Slab Foundation, Slightly Elevated This home sits on a concrete slab and is elevated by less than one metre. The slight elevation can offer a marginal benefit in terms of flood resilience, though properties in low-lying coastal areas like Paradise Point should always be assessed carefully against local flood mapping data.

Construction Year: 1981 Homes built in the early 1980s are well past the 40-year mark. While double brick construction ages well, older homes may have outdated plumbing, electrical systems, or roofing materials that can attract higher premiums or specific exclusions. It's worth ensuring your sum insured reflects current rebuild costs, including any upgrades made over the decades.

Swimming Pool A pool adds liability considerations to your policy. Most home and contents policies include some level of public liability cover, but it's worth confirming your policy explicitly covers pool-related incidents, particularly given Queensland's strict pool fencing laws.

Solar Panels Solar panels are an increasingly common feature and most insurers now include them under building cover — but it's worth double-checking. Panels can be damaged by hail or storm events, and their replacement cost should ideally be factored into your sum insured.

---

Tips for Homeowners in Paradise Point

1. Review Your Sum Insured Annually With a building sum insured of $886,000, it's critical to ensure this figure reflects the true cost of rebuilding your home from scratch — not its market value. Construction costs on the Gold Coast have risen significantly in recent years. Underinsurance is one of the most common and costly mistakes homeowners make.

2. Check Your Flood and Storm Surge Cover Paradise Point's canal-side and coastal geography means flood and storm surge risk is a genuine concern. Not all policies treat these the same way — some exclude storm surge entirely or apply separate flood sub-limits. Read the Product Disclosure Statement (PDS) carefully and ask your insurer directly.

3. Compare at Renewal, Not Just Once Insurance premiums can shift significantly year to year. The fact that this quote is below the suburb average today doesn't mean it will remain competitive at renewal. Set a reminder to compare quotes at CoverClub before your policy renews each year.

4. Consider Your Excess Strategy Both the building and contents excess on this policy are set at $1,000. Opting for a higher voluntary excess can reduce your annual premium, which may make sense if you have sufficient savings to cover a larger out-of-pocket cost in the event of a claim. Conversely, a lower excess provides more financial protection when you need to claim.

---

Ready to Compare?

Whether you're a long-term Paradise Point local or new to the area, it pays to know where your premium sits relative to the market. CoverClub makes it easy to compare home and contents insurance quotes from multiple insurers in minutes. Get a quote today and see how much you could save — or simply confirm that your current cover is giving you the value you deserve.