If you own a four-bedroom free standing home in Parkdale, VIC 3195, you're likely no stranger to the challenge of figuring out whether your home insurance premium is reasonable. Parkdale is a well-established bayside suburb in Melbourne's south-east, characterised by a mix of post-war homes, tree-lined streets, and a strong sense of community. Properties here tend to be solid, older-style dwellings — and that history has a real bearing on what insurers charge.

In this article, we break down a recent home and contents insurance quote for a four-bedroom, two-bathroom free standing home in Parkdale, comparing it against suburb, state, and national benchmarks to help you understand exactly where it sits.

---

Is This Quote Fair?

The quote in question comes in at $2,593 per year (or $249/month) for combined home and contents cover, with a building sum insured of $1,803,000 and contents valued at $248,000. Both the building and contents excess are set at $5,000.

Our independent price rating for this quote is FAIR — Around Average.

That assessment holds up when you look at the numbers. The Parkdale suburb average sits at $2,497/year, and the median is $2,431/year — meaning this quote is slightly above the midpoint but well within the normal range for the area. Specifically, it falls between the suburb's 25th percentile ($2,095/yr) and the 75th percentile ($2,819/yr), which is exactly where you'd expect a reasonably priced quote to land.

It's worth noting that a $5,000 excess on both building and contents is on the higher end of the spectrum. Choosing a higher excess is a common way to bring down your annual premium — so if this quote feels a touch steep, it may partly reflect that trade-off working in the policyholder's favour already.

---

How Parkdale Compares

One of the most useful ways to evaluate any insurance quote is to zoom out and look at the broader context. Here's how Parkdale stacks up:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Parkdale (3195) | $2,497/yr | $2,431/yr |

| Kingston LGA (Vic.) | $3,103/yr | — |

| Victoria | $3,000/yr | $2,718/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. First, Parkdale premiums are meaningfully below both the Victorian state average and the Kingston LGA average — suggesting the suburb is considered relatively lower risk by insurers compared to other parts of the region. Second, the national average of $5,347/year is dramatically higher than what Parkdale homeowners are paying, though this is largely skewed by high-risk areas in Queensland, Western Australia, and the Northern Territory where cyclone, flood, and bushfire exposure drives premiums up sharply.

For deeper suburb-level data, visit the Parkdale insurance stats page. You can also explore Victoria-wide home insurance trends or the national home insurance overview for a broader picture.

---

Property Features That Affect Your Premium

Every home is different, and insurers price policies based on a detailed assessment of a property's characteristics. Here's how the specific features of this Parkdale home are likely influencing the quote:

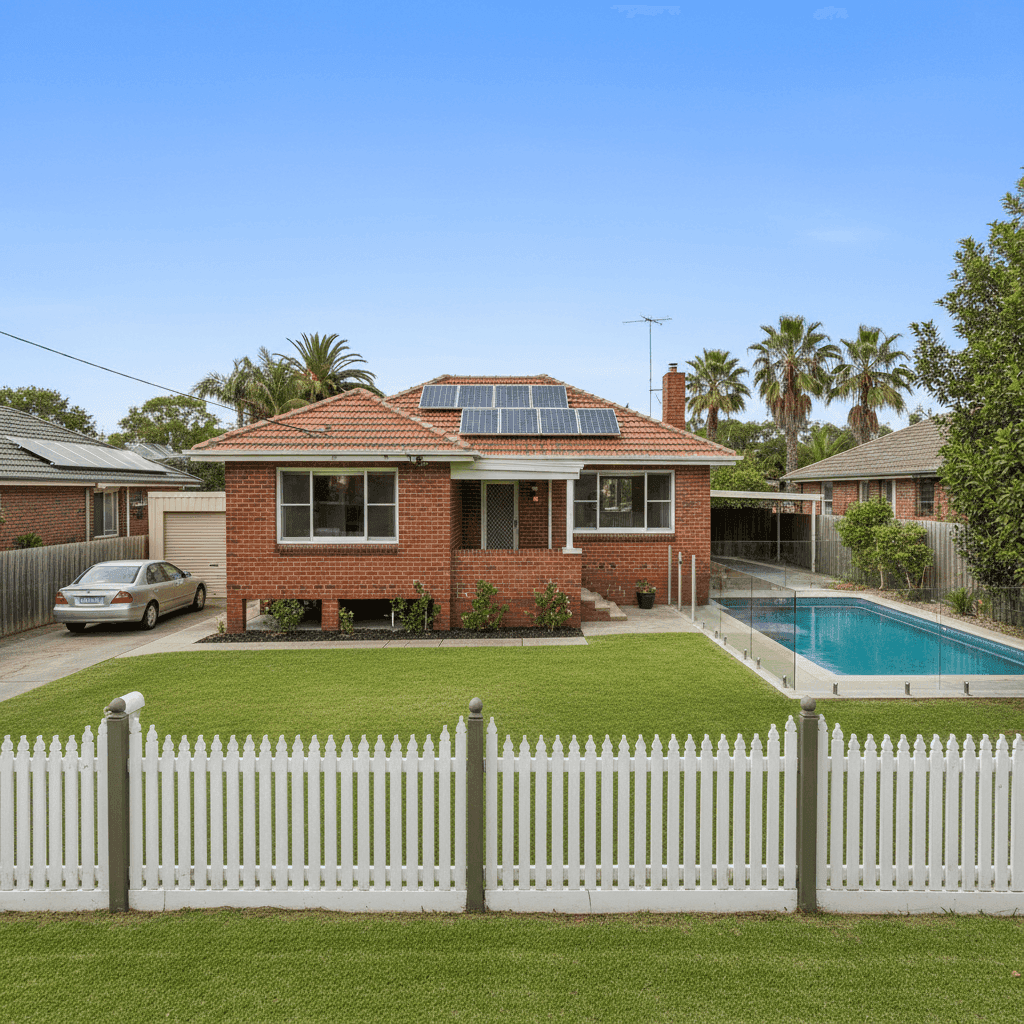

Age and Construction (1955 Build, Brick Veneer, Tiled Roof)

Built in 1955, this home falls squarely into the post-war era — a common vintage in Parkdale and the broader Bayside area. Brick veneer construction is generally viewed favourably by insurers; it's durable, fire-resistant, and widely understood. Tiled roofs similarly attract reasonable rates, as they're long-lasting and less prone to storm damage than some alternatives. That said, older homes can carry higher rebuild costs due to the complexity of matching period features and materials, which may partly explain the substantial building sum insured of $1,803,000.

Stump Foundation and Timber Flooring

The property sits on stumps and features timber or laminate flooring — both hallmarks of a classic Melbourne home of this era. Stump foundations can introduce some additional risk considerations, particularly around subsidence or moisture ingress, though in a well-maintained home these are manageable. Insurers may factor this into their assessment, particularly if the property is elevated by less than one metre.

Pool, Solar Panels, and Ducted Climate Control

The presence of a swimming pool adds to the insurable value of the property and can increase liability exposure — both factors that nudge premiums upward. Solar panels on the roof are increasingly common in Victoria and are generally covered under building insurance, though it's always worth confirming the extent of that cover with your insurer. Ducted climate control is another high-value fixture that contributes to the overall contents and building sum insured.

No Cyclone Risk

Parkdale is not in a cyclone risk zone, which is a meaningful advantage. Cyclone-prone areas in northern Australia can face premiums several times higher than those in Melbourne's south-east — so this is a genuine cost saving for Parkdale homeowners.

---

Tips for Homeowners in Parkdale

1. Review Your Sum Insured Regularly

A building sum insured of $1,803,000 is substantial, and it's important this figure reflects the actual cost to rebuild — not the market value of the property. With construction costs rising across Victoria, it's worth getting an independent building valuation every few years to ensure you're neither underinsured nor paying for more cover than you need.

2. Consider Whether Your Excess Suits Your Situation

A $5,000 excess on both building and contents is relatively high. While it reduces your annual premium, it also means you'd need to cover the first $5,000 of any claim out of pocket. If you'd struggle to absorb that cost in an emergency, it may be worth comparing quotes with a lower excess to find the right balance.

3. Don't Forget to Cover Your Pool and Solar

Make sure your policy explicitly covers your swimming pool (including the pump and filtration equipment) and solar panel system. These are significant assets that are sometimes underspecified in standard policies — leaving homeowners with unexpected gaps at claim time.

4. Compare Quotes Before Renewal

With 22 quotes sampled in the Parkdale suburb dataset, there's clear evidence that premiums vary considerably from insurer to insurer. The gap between the 25th and 75th percentile is over $700/year — meaning the difference between a good deal and a poor one can be substantial. Don't let your policy auto-renew without shopping around first.

---

Ready to Compare?

Whether you're reviewing an existing policy or shopping for cover on a new property, comparing multiple quotes is the single most effective way to make sure you're getting fair value. Get a home insurance quote through CoverClub and see how your premium stacks up against real data from your suburb and beyond.