If you own a four-bedroom free standing home in Parkhurst, QLD 4702, you're likely paying close attention to the cost of home and contents insurance — especially as premiums across Queensland continue to climb. This article breaks down a real insurance quote for a property in this suburb, puts the price in context, and offers practical tips to help you get better value on your cover.

---

Is This Quote Fair?

The quote in question comes to $3,952 per year (or $364 per month) for combined home and contents insurance, covering a building sum insured of $600,000 and contents valued at $100,000. The building excess is set at $5,000 and the contents excess at $2,000.

Our pricing analysis rates this quote as FAIR — around average. That means you're not being overcharged, but there's also room to potentially find a more competitive deal depending on your insurer and policy features.

To put this in perspective: the quote sits just above the suburb average of $3,397/yr and comfortably below the suburb's 75th percentile of $3,971/yr. In other words, roughly three-quarters of comparable quotes in Parkhurst come in at a similar price or lower — but a quarter are actually more expensive. You're in the middle of the pack, which is a reasonable position to be in for a well-appointed, newly built home in this part of Queensland.

---

How Parkhurst Compares

Understanding how your premium stacks up across different benchmarks gives you real negotiating power. Here's how this quote measures up:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $3,952 |

| Parkhurst Suburb Average | $3,397 |

| Parkhurst Suburb Median | $3,162 |

| Parkhurst 25th Percentile | $2,776 |

| Parkhurst 75th Percentile | $3,971 |

| QLD State Average | $4,547 |

| QLD State Median | $3,931 |

| National Average | $2,965 |

| National Median | $2,716 |

A few things stand out here. First, this quote is significantly below the Queensland state average of $4,547/yr — a meaningful saving of nearly $600 per year. That's a positive sign, suggesting the property's characteristics and location aren't attracting the worst-case pricing that many Queensland homeowners face.

Second, compared to the national average of $2,965/yr, the quote is noticeably higher. This reflects the broader reality of insuring property in Queensland, where weather-related risk, building costs, and claims history push premiums above the national norm. This is a pattern you'll see consistently when you explore Queensland insurance data versus national benchmarks.

For more localised data specific to this postcode, you can explore Parkhurst suburb insurance statistics to see how premiums trend over time and how your property compares.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct influence on what insurers charge. Here's what's likely at play:

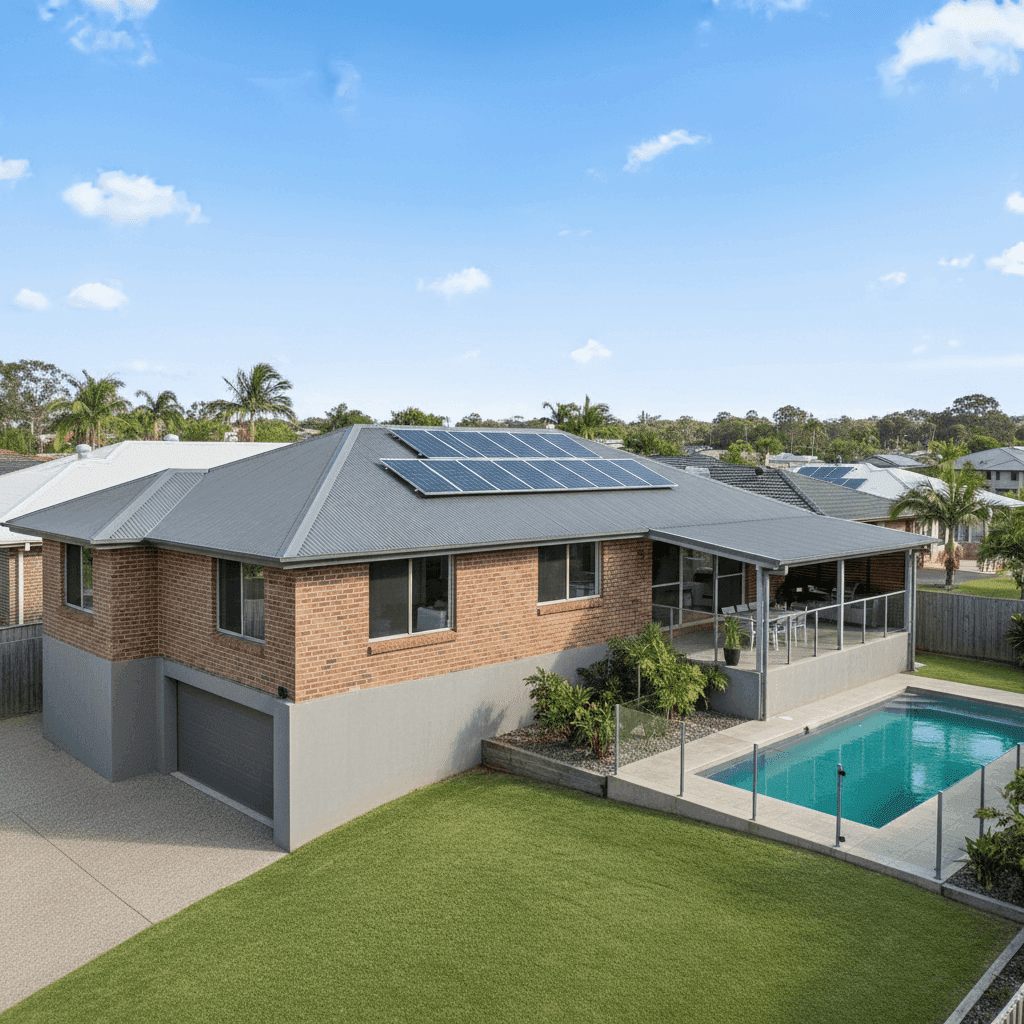

Newly Built (2025)

A brand-new home is generally viewed favourably by insurers. Modern construction meets current building codes, which typically means better structural integrity, improved fire resistance, and reduced likelihood of certain claims. This can work in your favour at renewal time.

Brick Veneer Walls & Colorbond Roof

Brick veneer is a widely accepted construction type in Australia and is generally considered low-to-moderate risk. Steel/Colorbond roofing is durable, fire-resistant, and well-suited to Queensland's climate — both features that tend to support competitive premiums compared to, say, timber or tile.

Slab Foundation

A concrete slab foundation is standard for modern Queensland builds and is generally considered stable and low-risk from an insurance perspective, particularly in non-flood-prone areas.

Pool, Solar Panels & Ducted Climate Control

These three features add value to the property — and to the sum insured. A swimming pool introduces liability considerations and can nudge premiums upward slightly. Solar panels are an increasingly common inclusion in Queensland homes, but they do represent a significant asset that needs to be covered under the building sum insured. Ducted climate control is similarly reflected in the above-average fittings quality rating, which influences the overall rebuild cost estimate.

Above-Average Fittings Quality

Higher-quality fittings mean a higher rebuild cost, which flows through to the $600,000 building sum insured. This is appropriate — underinsuring a well-appointed home is a common and costly mistake.

Slightly Elevated (Less Than 1m)

The property is noted as being elevated by less than one metre. While this is a modest elevation, it can still offer some benefit in terms of flood resilience, which may be factored into the risk assessment.

No Cyclone Risk

Parkhurst is not classified as a cyclone risk area, which is a meaningful advantage for Queensland homeowners. Cyclone-rated premiums in northern parts of the state can be dramatically higher, so this property avoids that loading entirely.

---

Tips for Homeowners in Parkhurst

Whether you're reviewing your current policy or shopping for the first time, here are some practical steps to make sure you're getting the best value:

- Review your sum insured annually. Building costs in Queensland have risen sharply in recent years. A home built in 2025 with above-average fittings needs a sum insured that reflects today's rebuild costs — not last year's. Make sure your $600,000 figure is reviewed at each renewal.

- Consider your excess carefully. This quote carries a $5,000 building excess and a $2,000 contents excess. Choosing a higher excess is one of the most effective ways to reduce your annual premium, but only if you're genuinely comfortable covering that amount out of pocket in the event of a claim. Run the numbers before locking in.

- Bundle home and contents — but compare separately too. Combined home and contents policies are convenient and often offer a discount, but it's worth getting separate quotes to make sure the bundled price is actually competitive for both components.

- Use comparison data to your advantage. With the suburb median sitting at $3,162/yr, there's a reasonable gap between this quote and what some homeowners in Parkhurst are paying. That doesn't mean a cheaper policy is better — but it does mean it's worth shopping around to see what else is available at a similar or higher level of cover.

---

Ready to Compare?

Whether you're happy with your current quote or keen to explore alternatives, comparing your options is always a smart move. At CoverClub, we make it easy to see how your premium stacks up and find cover that suits your property and budget. Get a home insurance quote today and see what's available for your Parkhurst home.