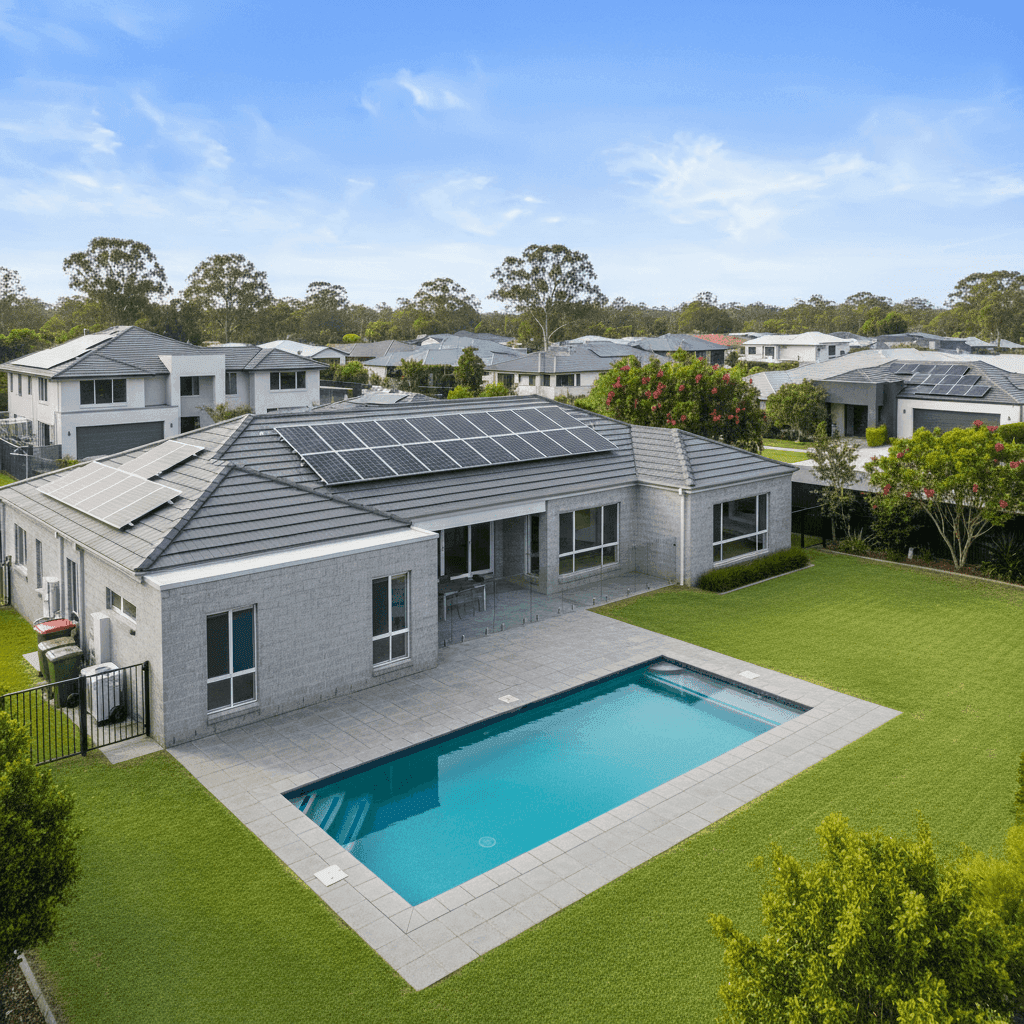

If you own a free standing home in Parkwood, QLD 4214, you've probably noticed that home insurance premiums can vary enormously — even between similar properties on the same street. This article breaks down a real home and contents insurance quote for a five-bedroom, three-bathroom home in Parkwood, examining whether the price stacks up against local, state, and national benchmarks, and what factors are likely driving the cost.

---

Is This Quote Fair?

The quote in question comes in at $4,760 per year (or $456/month) for combined home and contents cover, with a $2,000 excess on both building and contents. Our price rating for this quote is Expensive — above average for the Parkwood area.

To put that in context: the suburb average premium for Parkwood sits at $3,649/year, and the median is even lower at $3,408/year. That means this quote is roughly $1,111 above the suburb average — a meaningful gap that's worth interrogating before simply accepting the price.

That said, "expensive" doesn't automatically mean "wrong." A few factors specific to this property — including its size, the high building sum insured, and the presence of a pool and solar panels — can legitimately push premiums above the local norm. We'll unpack those shortly.

One important consideration: the building sum insured is set at $2,000,000, which is exceptionally high for a 286 sqm home in Parkwood. If this figure has been over-estimated, it could be a significant driver of the elevated premium. Reviewing your sum insured with a licensed adviser or quantity surveyor is always worthwhile.

---

How Parkwood Compares

Understanding where Parkwood sits within the broader insurance landscape helps you gauge whether a quote is reasonable. Here's a snapshot based on data from 87 quotes collected for the Parkwood area:

| Benchmark | Premium |

|---|---|

| Parkwood 25th percentile | $2,434/yr |

| Parkwood median | $3,408/yr |

| Parkwood average | $3,649/yr |

| This quote | $4,760/yr |

| Parkwood 75th percentile | $4,360/yr |

| Gold Coast LGA average | $8,161/yr |

| QLD state average | $9,129/yr |

| National average | $5,347/yr |

There are a few interesting takeaways here. First, this quote — while above the Parkwood average — is actually below both the QLD state average and the national average. Queensland as a whole carries some of the highest home insurance premiums in the country, largely due to the prevalence of flood, storm, and cyclone risk across the state. Parkwood, located in the Gold Coast hinterland, benefits from a non-cyclone risk classification, which keeps premiums notably lower than many other QLD postcodes.

The Gold Coast LGA average of $8,161/year also underscores just how varied premiums can be within a single council area — coastal and low-lying suburbs tend to attract significantly higher premiums than inland areas like Parkwood.

---

Property Features That Affect Your Premium

Several characteristics of this property will be influencing the quoted premium, both positively and negatively.

Building Construction

The home features concrete external walls and a tiled roof, both of which are generally viewed favourably by insurers. Concrete construction is highly resistant to fire and impact damage, while tiles are considered a durable, lower-risk roofing material compared to metal or timber alternatives. The slab foundation is similarly standard and well-regarded in Queensland's climate.

Size and Age

At 286 sqm, this is a substantial home. Larger homes cost more to rebuild, which directly influences the premium. Built in 1995, the property is around 30 years old — old enough that some systems (plumbing, electrical) may be approaching the end of their service life, which insurers factor into their risk assessments.

Swimming Pool

A pool adds both value and liability to a property. Insurers typically account for the cost of pool repairs or replacement in the event of structural damage, and in some cases, liability cover for accidents involving the pool may also influence pricing.

Solar Panels

Solar panels are an increasingly common feature on Queensland homes, but they do add complexity to a claim. Panels can be damaged by hail, storms, or falling debris, and their replacement cost needs to be factored into the building sum insured. Ensuring your solar system is adequately covered — and not overlooked in your policy — is essential.

Ducted Climate Control

A ducted air conditioning system is a high-value fixed installation that forms part of the building sum insured. These systems can cost tens of thousands of dollars to replace, and their inclusion is another legitimate reason for a premium to sit above the suburb median.

---

Tips for Homeowners in Parkwood

1. Review your building sum insured carefully A $2,000,000 building sum insured for a 286 sqm home is worth scrutinising. The sum insured should reflect the cost to rebuild your home from scratch — not its market value. Over-insuring inflates your premium without providing additional benefit. Consider getting a professional rebuild cost estimate.

2. Shop around — especially at renewal Insurers rarely reward loyalty with lower premiums. At renewal time, it pays to compare quotes from multiple providers. Even a modest saving of $300–$500 per year compounds significantly over time.

3. Consider your excess strategy This policy carries a $2,000 excess on both building and contents. Opting for a higher excess is one of the most straightforward ways to reduce your annual premium — just make sure the excess is an amount you could genuinely afford to pay in the event of a claim.

4. Check that your pool and solar panels are correctly listed Both your pool and solar panel system should be explicitly covered under your policy. Review the product disclosure statement (PDS) to confirm what's included and whether any sub-limits apply to these items. If your solar system has been upgraded since you took out the policy, notify your insurer to avoid being underinsured.

---

Compare Your Options with CoverClub

Whether this quote is the right fit depends on your individual circumstances — but you shouldn't have to accept the first number you're given. CoverClub makes it easy to compare home and contents insurance quotes for your Parkwood property, so you can see what the market is actually offering. You can also explore local premium data for Parkwood and broader QLD insurance trends to make a more informed decision. A few minutes of comparison could save you hundreds of dollars a year.