Parrearra is a sought-after coastal suburb on Queensland's Sunshine Coast, sitting within postcode 4575 and known for its waterway-facing streets, relaxed lifestyle, and strong property values. If you own a free standing home here, you'll know that protecting it with the right insurance is non-negotiable — but knowing whether you're paying a fair price is a different challenge entirely. This article breaks down a real home and contents insurance quote for a four-bedroom property in Parrearra, compares it against local, state, and national benchmarks, and offers practical advice for homeowners looking to get better value.

---

Is This Quote Fair?

The quote in question comes to $4,791 per year (or $468 per month) for a combined home and contents policy, covering a building sum insured of $700,000 and contents valued at $20,000. Both the building and contents excess are set at $1,000.

Our pricing analysis rates this quote as Expensive — Above Average.

To put that in context: the average home and contents premium for properties in the Parrearra suburb sits at $4,238 per year, with a median of $4,118. This quote lands above both figures, and also exceeds the 75th percentile for the suburb ($4,742), meaning it's priced higher than roughly three-quarters of comparable quotes in the area.

That said, "expensive" doesn't automatically mean "wrong." A $700,000 building sum insured is substantial, and a 315 sqm home with a pool and solar panels carries genuine complexity that insurers price accordingly. The question isn't just whether this premium is high — it's whether the coverage justifies the cost, and whether shopping around could deliver the same protection for less.

---

How Parrearra Compares

Understanding where Parrearra sits in the broader insurance landscape helps frame whether any local quote is reasonable. You can explore the full data on the Parrearra suburb stats page.

| Benchmark | Annual Premium |

|---|---|

| This quote | $4,791 |

| Parrearra suburb average | $4,238 |

| Parrearra suburb median | $4,118 |

| QLD state average | $4,547 |

| QLD state median | $3,931 |

| National average | $2,965 |

| National median | $2,716 |

| Sunshine Coast LGA average | $7,249 |

A few things stand out here. First, Queensland homeowners already pay significantly more than the national average — the QLD state average of $4,547 is more than 50% above the national average of $2,965. This reflects the elevated risk profile of Queensland properties generally, driven by factors like storm activity, flooding, and extreme weather events that are far less common in southern states.

Second — and perhaps surprisingly — this quote is actually well below the Sunshine Coast LGA average of $7,249. The LGA figure is pulled upward by higher-risk areas within the region, so Parrearra's suburb-level averages are a more meaningful comparison point. On that basis, this quote does sit on the expensive side, but it's not dramatically out of step with the local market.

---

Property Features That Affect Your Premium

Several characteristics of this property are likely influencing the premium, both positively and negatively.

Construction Materials

The home features Hardiplank/Hardiflex external walls and a steel Colorbond roof — both of which are generally viewed favourably by insurers. Colorbond roofing is durable, resistant to corrosion, and performs well in high-wind conditions. Hardiflex cladding is non-combustible and low-maintenance. Compared to weatherboard or older brick construction, these materials can help moderate premiums.

Slab Foundation

A concrete slab foundation is standard for Queensland homes built in the 2000s and is typically considered a neutral-to-positive factor. It reduces the risk of subsidence and pest-related structural damage compared to older suspended floor systems.

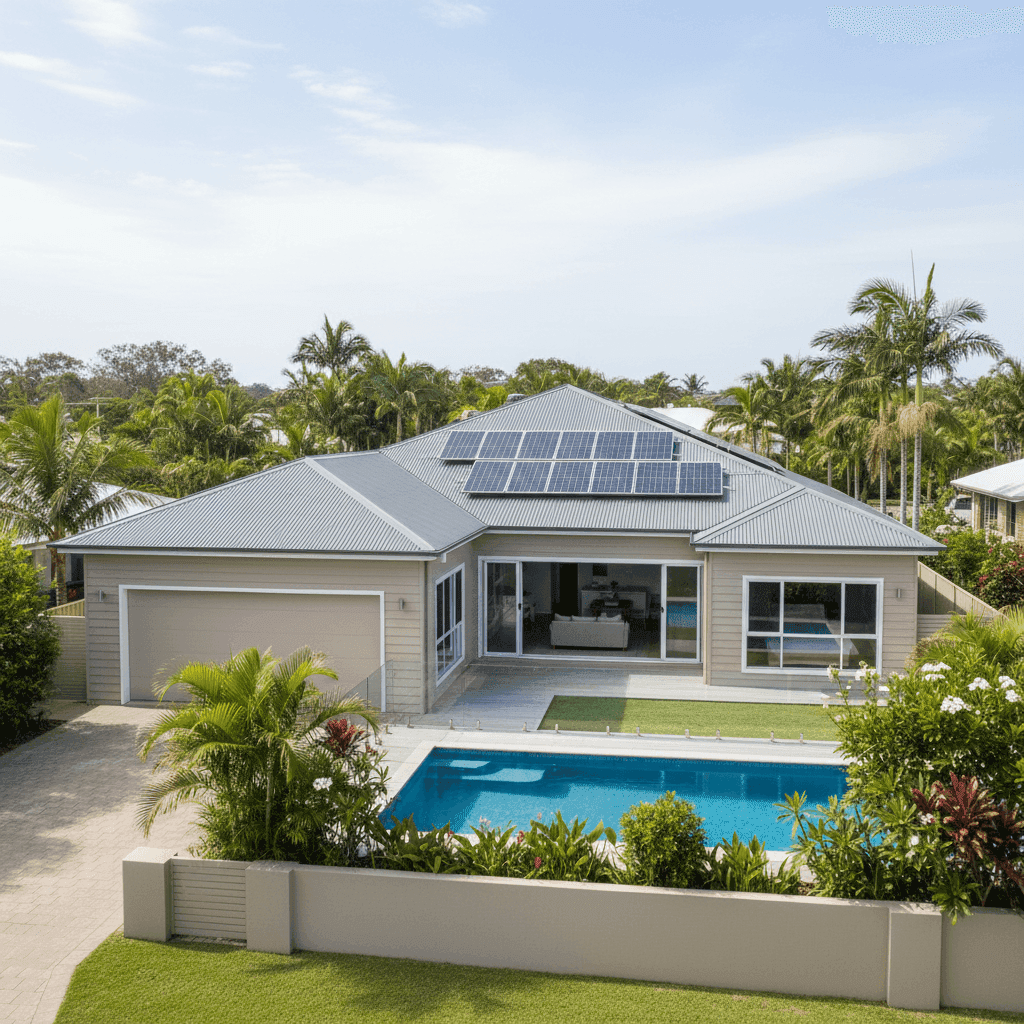

Swimming Pool

The presence of a pool adds to the replacement cost of the property and introduces additional liability considerations. Insurers factor in the cost of pool fencing compliance, equipment, and the pool structure itself when calculating building sums insured.

Solar Panels

Solar panels are increasingly common on Queensland homes, but they do add to the insured value of the building. A quality solar system can represent $10,000–$20,000 or more in replacement costs. It's worth confirming with your insurer that your panels are explicitly covered under your building policy, as some policies treat them as an optional extra.

Building Size and Age

At 315 sqm and built in 2005, this is a relatively modern, mid-to-large home. The $700,000 building sum insured translates to roughly $2,222 per sqm — broadly in line with current Queensland construction costs for a well-fitted home of this size, though it's worth periodically reviewing this figure to avoid being under- or over-insured.

---

Tips for Homeowners in Parrearra

1. Compare Multiple Quotes — Especially in QLD

Queensland's insurance market is competitive, and premiums for the same property can vary significantly between providers. Given this quote sits above the suburb average, it's worth getting at least two or three competing quotes before renewing. CoverClub makes it easy to compare without having to contact each insurer individually.

2. Review Your Building Sum Insured Annually

Construction costs have risen sharply in recent years. If your sum insured hasn't kept pace, you could be underinsured in the event of a total loss. Equally, if your sum insured is too high, you may be paying more premium than necessary. Use a building cost calculator or speak with a quantity surveyor to validate your figure.

3. Check That Your Pool and Solar Are Properly Covered

These are two features that homeowners sometimes assume are automatically included — but coverage can vary. Confirm with your insurer exactly what is and isn't covered for your pool equipment, fencing, and solar system. Some policies cap solar panel cover or exclude certain types of damage.

4. Ask About Excess Adjustments

Both the building and contents excess on this policy are set at $1,000. Increasing your excess — for example, to $2,500 — can meaningfully reduce your annual premium. If you have sufficient savings to cover a higher out-of-pocket amount in the event of a claim, this can be a cost-effective strategy.

---

Ready to See What You Could Pay?

Whether you're renewing an existing policy or insuring a new purchase, comparing quotes is the single most effective way to make sure you're not overpaying. CoverClub aggregates real premium data from across Australia so you can see exactly how your quote stacks up — and find better options if they exist.