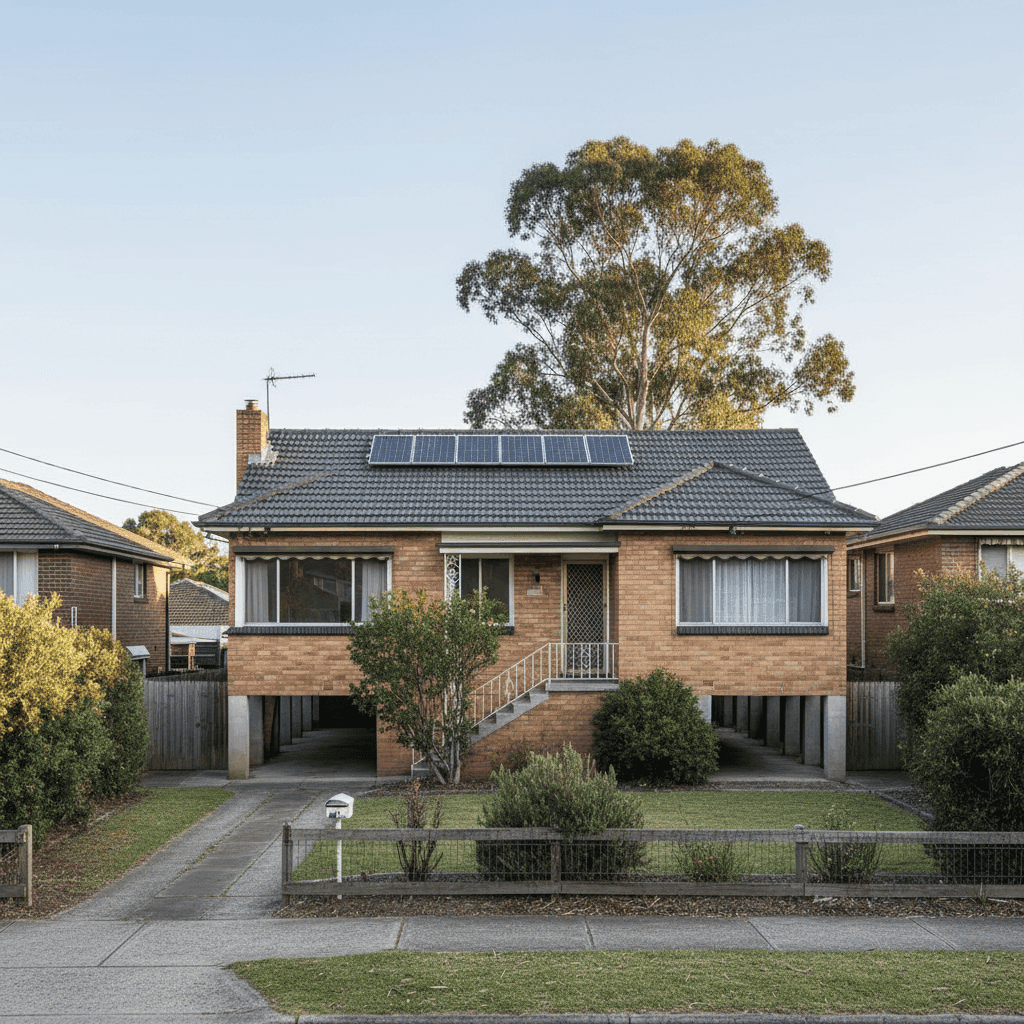

If you own a free standing home in Pascoe Vale, VIC 3044, you've probably wondered whether you're paying a fair price for home insurance — or whether there's a better deal out there. This article breaks down a real home and contents insurance quote for a 3-bedroom, brick veneer property in the suburb, and puts the numbers in context against local, state, and national benchmarks.

---

Is This Quote Fair?

The quoted annual premium for this property is $1,595 per year (or $153/month), covering both building (sum insured: $708,000) and contents ($50,000), each with a $1,000 excess.

Our price rating for this quote is FAIR — around average. That assessment is backed by data. Based on 37 quotes collected for Pascoe Vale, the suburb average sits at $1,487/year, with a median of $1,379/year. This quote comes in about $108 above the suburb average and $216 above the median — placing it comfortably within the middle of the market, just above the 50th percentile but well below the 75th percentile of $1,782/year.

In other words, you're not getting the cheapest deal available in the area, but you're also far from overpaying. For a property of this size (214 sqm) and age (built 1983), with features like solar panels and ducted climate control, landing in the mid-range is a reasonable outcome.

---

How Pascoe Vale Compares

One of the most telling aspects of this quote is just how favourably Pascoe Vale sits relative to broader benchmarks.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Pascoe Vale (suburb) | $1,487/yr | $1,379/yr |

| LGA (Moreland) | $1,551/yr | — |

| Victoria (state) | $3,000/yr | $2,718/yr |

| National | $5,347/yr | $2,764/yr |

Compared to the Victorian state average of $3,000/year, homeowners in Pascoe Vale are paying roughly half what the typical Victorian pays. And against the national average of $5,347/year — heavily influenced by high-risk regions like northern Queensland and coastal areas — Pascoe Vale looks exceptionally affordable.

Even within the Moreland LGA, Pascoe Vale tracks slightly below the local government area average of $1,551/year, suggesting it's one of the more competitively priced pockets in the region.

The key takeaway: Pascoe Vale is a relatively low-risk suburb from an insurer's perspective, and that's reflected in the premiums on offer.

---

Property Features That Affect Your Premium

Several characteristics of this particular property influence where the premium lands — both positively and negatively.

🧱 Brick Veneer Walls & Tiled Roof

Brick veneer construction is one of the most common wall types in Melbourne's inner-north, and insurers generally view it favourably. It offers solid fire resistance and durability. Combined with a tiled roof — another low-maintenance, fire-resistant material — this property presents a relatively low structural risk profile.

🏠 Elevated on Stumps

The property sits elevated by at least one metre on stumps, which is a notable feature. On the positive side, elevation can reduce flood and moisture damage risk to the main living areas. However, stump foundations do introduce some additional considerations — they can be more susceptible to subsidence, pest damage, and movement over time, which some insurers may price in. The timber and laminate flooring throughout is also consistent with this style of construction.

☀️ Solar Panels

Solar panels are increasingly common on Australian homes, and most home insurance policies cover them as part of the building sum insured. It's worth confirming with your insurer that the panels are explicitly included in your $708,000 building cover, as some policies treat them as optional extras.

❄️ Ducted Climate Control

Ducted heating and cooling systems add meaningful value to a home and can increase the cost to rebuild or repair — both of which feed into the building sum insured calculation. Having this system properly accounted for in your $708,000 sum insured is important to avoid being underinsured.

📅 1983 Construction

Homes built in the early 1980s are well past the stage where construction defects are a concern, but they may have older electrical wiring, plumbing, or roofing materials that could require attention. Insurers sometimes factor in the age of a property when assessing risk, particularly for internal systems.

---

Tips for Homeowners in Pascoe Vale

1. Check Your Sum Insured Annually

With building costs continuing to rise across Victoria, the $708,000 sum insured on this property should be reviewed each year at renewal. Underinsurance is one of the most common — and costly — mistakes homeowners make. Use a building calculator or speak with a quantity surveyor if you're unsure.

2. Confirm Solar Panel Coverage

Before renewing, ask your insurer explicitly whether your solar panels are covered under the building policy and up to what value. Some policies have sub-limits or exclusions for solar systems, particularly for damage caused by electrical faults.

3. Consider Raising Your Excess to Lower Your Premium

This quote carries a $1,000 excess on both building and contents. If you have the financial buffer to absorb a higher out-of-pocket cost in the event of a claim, increasing your excess to $2,000 or more can meaningfully reduce your annual premium.

4. Shop Around at Renewal

Even with a "Fair" rating, there's a spread of $607/year between the 25th percentile ($1,175/yr) and 75th percentile ($1,782/yr) in Pascoe Vale alone. That's a significant range, and it means comparison shopping at renewal could put real money back in your pocket. Don't assume your current insurer's renewal quote is competitive.

---

Ready to Compare?

Whether you're reviewing your current policy or shopping for the first time, CoverClub makes it easy to see how your quote stacks up. Get a home insurance quote today and compare options tailored to your Pascoe Vale property — so you can make a confident, informed decision at renewal time.