Paterson is a quiet residential locality in Queensland's Fraser Coast region, and like much of regional QLD, home insurance costs here can vary enormously depending on your property's characteristics and the insurer you choose. This article breaks down a real home and contents insurance quote for a 2-bedroom, free-standing home in Paterson (postcode 4570), comparing it against local, state, and national benchmarks — and offering practical tips to help you get the best deal on your cover.

---

Is This Quote Fair?

The annual premium for this property came in at $2,153 per year (or roughly $206 per month), covering both building and contents. CoverClub's pricing engine rates this as CHEAP — below average for the area, and it's easy to see why.

The building is insured for $300,000 with a $2,000 excess, while contents are covered for $31,000 with a $500 excess. For a 2-bedroom home with these coverage levels, that's a genuinely competitive outcome. The higher building excess of $2,000 plays a role in keeping the premium down — accepting a larger out-of-pocket cost in the event of a claim is one of the most effective levers for reducing what you pay annually.

So yes, by almost every measure, this quote represents strong value. But let's put the numbers in proper context.

---

How Paterson Compares

Understanding where a quote sits relative to the broader market is essential for judging whether you're getting a fair deal. Here's how this premium stacks up:

| Benchmark | Premium |

|---|---|

| This quote | $2,153/yr |

| Paterson suburb average | $6,022/yr |

| Paterson suburb median | $6,404/yr |

| Paterson 25th percentile | $4,667/yr |

| Fraser Coast LGA average | $4,810/yr |

| QLD state average | $9,129/yr |

| QLD state median | $3,903/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

The quote sits below the national median of $2,764, which is already a low bar to clear — and it clears it comfortably. It's also dramatically cheaper than the Paterson suburb average of $6,022, coming in at roughly 64% less than what the typical homeowner in the area is paying.

It's worth noting that the Queensland state average of $9,129 is exceptionally high — a reflection of the significant natural hazard exposure across much of the state, including cyclone, flood, and storm risk zones. The fact that this property sits well below even the national average of $5,347 suggests the insurer has assessed this particular property as relatively low risk.

One caveat: the suburb sample size is just 7 quotes, so the local averages should be interpreted with some caution. A larger dataset would give a more reliable picture of the Paterson market.

---

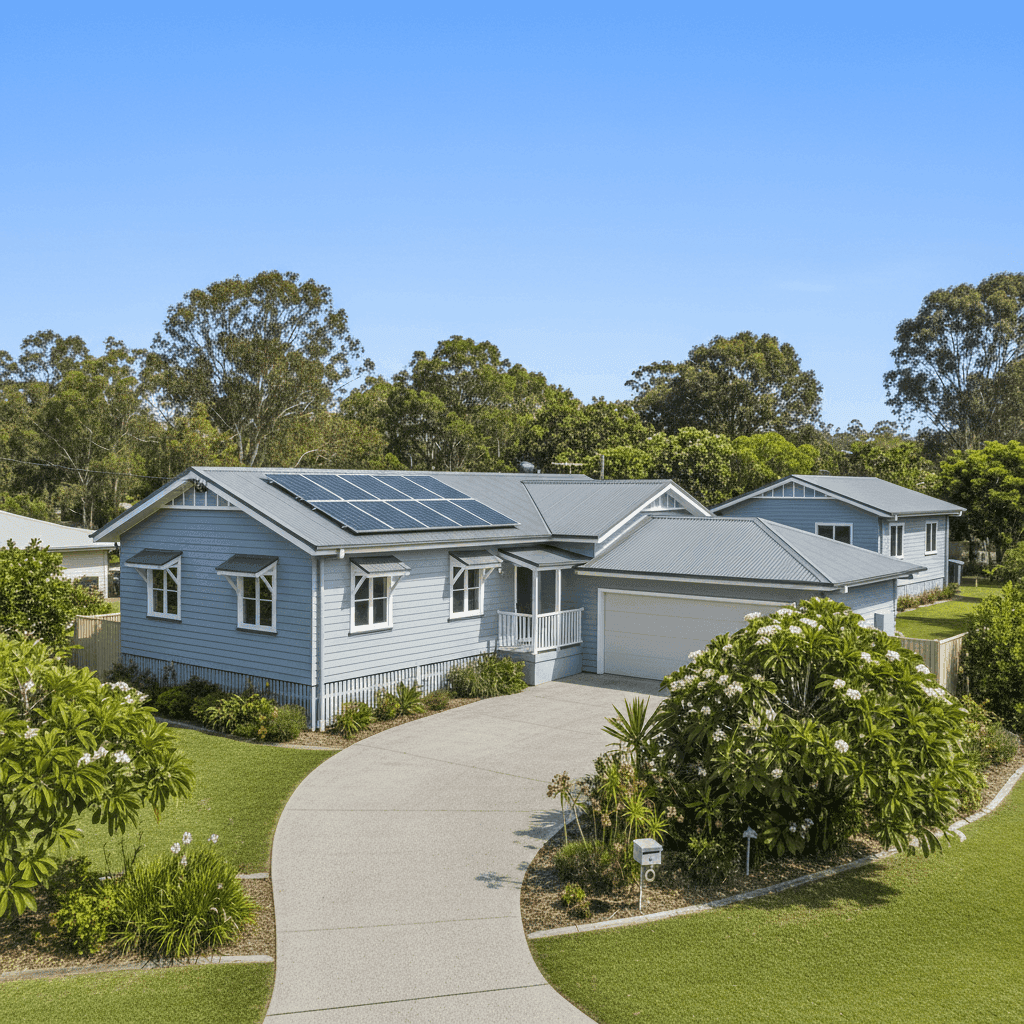

Property Features That Affect Your Premium

Several characteristics of this property are likely contributing to its favourable premium. Here's a breakdown of the key factors at play:

Weatherboard Timber Walls

Weatherboard wood is one of the more common external wall types in older Queensland homes, and it's generally viewed as a moderate-risk construction material. Timber can be more susceptible to fire and pest damage than brick or rendered masonry, which can push premiums up — but it's also widely understood by insurers and priced accordingly.

Steel / Colorbond Roof

Colorbond roofing is considered a strong, durable option by most insurers. It handles Queensland's harsh UV exposure, heavy rain, and hail better than terracotta or older iron sheeting, and it's a factor that can work in your favour at quoting time.

1980 Construction

Homes built in 1980 sit in a middle ground for insurers — old enough that some wear and tear is expected, but not so old that major structural concerns are presumed. Wiring, plumbing, and roofing from this era may warrant scrutiny, but the property's Colorbond roof (likely a later upgrade) mitigates some of that concern.

Slab Foundation

A concrete slab foundation is generally well-regarded by insurers. It's resistant to subsidence and termite ingress compared to raised stumped foundations, which is a plus — particularly in regional Queensland where soil movement and pests can be an issue.

Solar Panels

Solar panels add value to a property and also add a degree of complexity to an insurance policy. It's important to confirm with your insurer that the panels are explicitly included in your building sum insured, as some policies treat them as an optional extra. At $300,000 building cover, there should be sufficient headroom here, but it's worth verifying.

Granny Flat

The presence of a granny flat on the property is a meaningful factor. Whether it's used for family, rented out, or sits vacant, insurers will want to know — and some may require it to be separately declared or even separately insured. Make sure your policy wording covers the granny flat's structure and any contents within it.

Ducted Climate Control

Ducted air conditioning is a high-value fixture that contributes to the overall rebuild cost of the home. It's a positive sign that the building sum insured of $300,000 has been set to account for this — underinsurance on properties with significant fixed fittings is a common and costly mistake.

No Cyclone Risk

Paterson QLD 4570 falls outside designated cyclone risk zones, which is a significant premium driver in many parts of Queensland. The absence of cyclone loading is almost certainly one of the biggest reasons this quote is so competitive relative to the state average.

---

Tips for Homeowners in Paterson

Whether you're renewing your existing policy or shopping around for the first time, here are some practical steps to make sure you're getting the right cover at the right price.

1. Don't underinsure your building The $300,000 sum insured needs to reflect the full cost of rebuilding your home from scratch — not its market value. With a granny flat, ducted air conditioning, and solar panels on site, make sure your rebuild estimate accounts for all of these. Use a quantity surveyor or an online rebuild calculator if you're unsure.

2. Confirm the granny flat is covered Ask your insurer directly: does the policy cover the granny flat structure and any contents inside? If you're renting it out, you may also need landlord liability cover. Don't assume it's automatically included.

3. Review your excess settings This policy carries a $2,000 building excess — a smart way to reduce premiums, but only if you're comfortable funding that gap in the event of a claim. If $2,000 would be a financial stretch, consider whether a lower excess (and slightly higher premium) makes more sense for your situation.

4. Compare quotes at renewal Even a great quote today can become an average one at renewal. Insurers regularly re-price their books, and loyalty doesn't always pay. Make a habit of comparing at least two or three quotes each year before automatically renewing.

---

Compare Your Own Quote

Curious how your home insurance stacks up? CoverClub makes it easy to compare real quotes from multiple insurers in one place. Whether you're in Paterson or anywhere else in Australia, you can get a personalised home insurance quote in minutes — and see exactly how your premium compares to your neighbours'. Don't pay more than you need to.