If you own a free standing home in Pelaw Main, NSW 2327, you're likely no stranger to the charm of the Hunter Valley region — but you may be wondering whether you're getting a fair deal on your home insurance. This article breaks down a real home and contents insurance quote for a three-bedroom property in the area, compares it against local, state, and national benchmarks, and offers practical advice to help you make the most of your cover.

---

Is This Quote Fair?

The annual premium for this quote comes in at $3,398 per year (or $328 per month), covering both building and contents for a sum insured of $553,000 on the building and $20,000 on contents. CoverClub's pricing engine has rated this quote as CHEAP — below average for the area.

That's genuinely good news for the homeowner. In a market where insurance premiums have been climbing sharply across Australia due to extreme weather events, reinsurance costs, and inflationary pressures on building materials, landing a below-average premium is worth acknowledging. The $5,000 excess on both building and contents is on the higher side, which does contribute to keeping the premium down — but for homeowners who are comfortable self-insuring smaller claims, this is a reasonable trade-off.

---

How Pelaw Main Compares

To put this quote in proper context, here's how the $3,398 annual premium stacks up against available benchmarks:

| Benchmark | Annual Premium |

|---|---|

| This quote | $3,398 |

| Cessnock LGA average | $2,462 |

| NSW state median | $3,770 |

| NSW state average | $9,528 |

| National median | $2,764 |

| National average | $5,347 |

A few things stand out here. The quote sits below the NSW state median of $3,770 and well below the NSW state average of $9,528 — though that average is heavily skewed by high-risk properties in flood-prone and coastal areas across the state. Against the NSW state average data, this premium looks very competitive.

Compared to the national picture, the quote is above the national median of $2,764, which makes sense given the property's features — a pool, solar panels, and ducted climate control all add to the replacement cost and risk profile. It's also worth noting that the Cessnock LGA average of $2,462 is lower than this quote, but that figure likely reflects a broader mix of properties, including smaller or older homes with fewer features and lower sum insured values.

You can explore more localised data for the postcode on the Pelaw Main suburb stats page.

---

Property Features That Affect Your Premium

Several characteristics of this particular property play a meaningful role in how insurers calculate the premium.

Construction Era and Materials

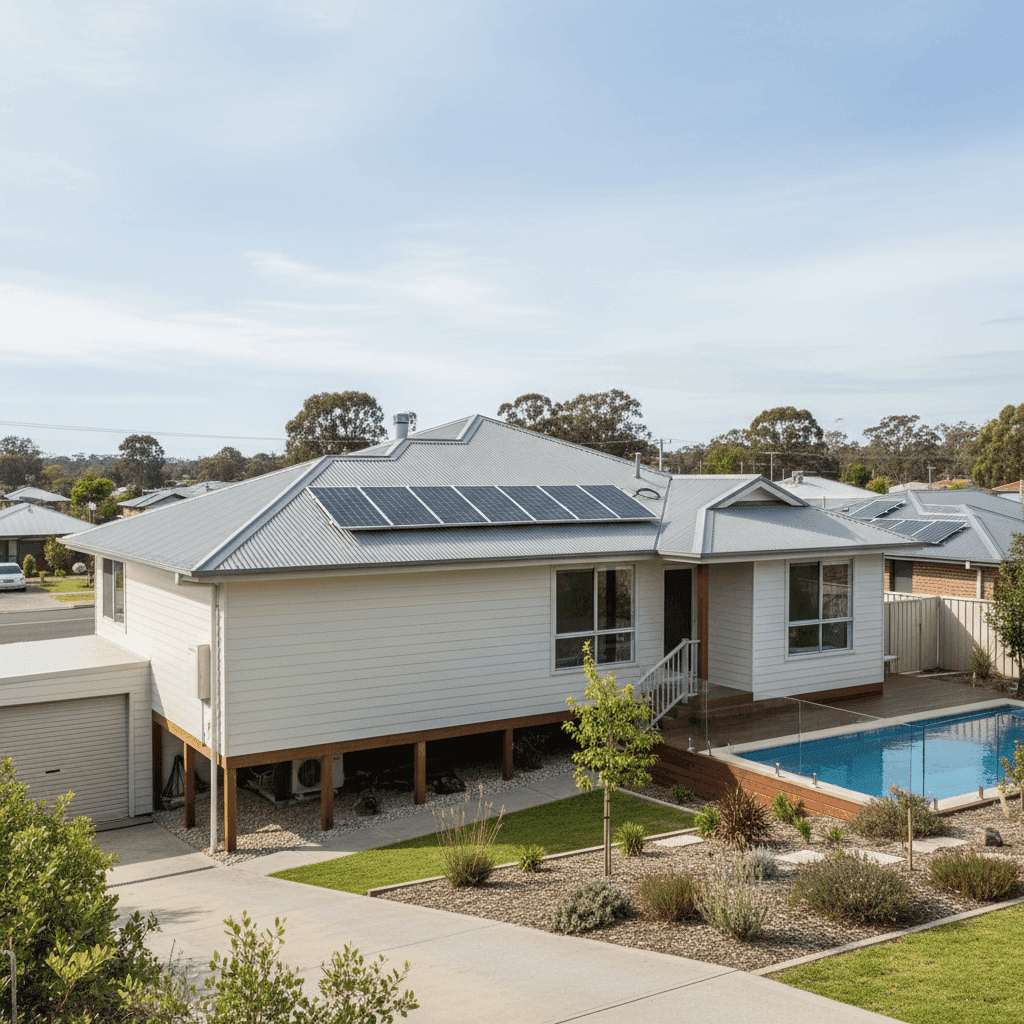

Built in 1940, this home is over 80 years old. Older homes often attract higher premiums because they may have outdated wiring, plumbing, or structural elements that increase the risk of claims. However, the Hardiplank/Hardiflex external walls are a genuine positive — this fibre cement cladding is fire-resistant, durable, and widely accepted by insurers as a lower-risk material compared to weatherboard or timber. The Colorbond steel roof is similarly well-regarded for its longevity and resistance to fire and weather.

Stump Foundation

The home sits on stumps, which is common for properties of this era in regional NSW. Stump foundations can be a flag for some insurers, particularly in areas with reactive soils, as they may be associated with subsidence or pest damage risk. It's worth confirming your policy covers structural movement or damage related to the foundation type.

Swimming Pool

A pool adds to both the replacement cost of the property and the liability risk, which flows through to the premium. Pools require fencing compliance under NSW law, and insurers will expect these standards to be met.

Solar Panels

With solar panels installed, the building sum insured needs to account for the cost of replacing the system — something that's easy to underestimate. At current installation costs, a quality solar system can run to $8,000–$15,000 or more, so it's important this is reflected in your $553,000 sum insured.

Ducted Climate Control

Ducted air conditioning is a significant fixed asset and contributes to the overall replacement cost of the home. Like solar panels, it's often overlooked when homeowners estimate their sum insured — but it should absolutely be factored in.

Flooring and Fittings

With carpet flooring and standard fittings, the interior fit-out is unlikely to push the replacement cost dramatically, which helps keep the overall sum insured — and therefore the premium — more manageable.

---

Tips for Homeowners in Pelaw Main

1. Review Your Sum Insured Annually

Building costs in regional NSW have risen significantly over the past few years. With a 1940s home featuring modern additions like solar and ducted air conditioning, it's easy for your sum insured to fall behind actual replacement costs. Underinsurance is one of the most common — and costly — mistakes homeowners make. Use a building cost calculator or speak with a local builder to sanity-check your $553,000 figure each year.

2. Understand What Your Excess Means in Practice

A $5,000 excess on both building and contents means you'll be covering the first $5,000 of any claim yourself. For smaller incidents — a broken window, minor storm damage, or a stolen appliance — you may find it's not worth claiming at all. Make sure you have a financial buffer to cover this amount if a larger event does occur.

3. Keep Pool and Solar Documentation Up to Date

Insurers may ask for evidence that your pool fencing meets NSW compliance standards, and some will want to know the make, model, and value of your solar system. Keeping these records handy can smooth the claims process and ensure you're not caught short if you need to make a claim.

4. Compare Quotes at Renewal Time

Even if this quote is competitively priced, the insurance market shifts constantly. Premiums can vary significantly between providers for the same property — sometimes by hundreds or even thousands of dollars. Don't let your policy roll over automatically without shopping around first.

---

Ready to Compare?

Whether you're happy with your current quote or wondering if you can do better, CoverClub makes it easy to compare home and contents insurance options for your Pelaw Main property. Get a quote today and see how your premium stacks up against the market in just a few minutes.