Pelican Waters is one of the Sunshine Coast's most sought-after residential pockets — a master-planned canal community in postcode 4551 known for its waterfront lifestyle, modern infrastructure, and strong property values. If you own a free standing home here, understanding what you should be paying for home and contents insurance is just as important as knowing your property's market value. This article breaks down a real insurance quote for a four-bedroom, two-bathroom home in Pelican Waters and puts the numbers into context against suburb, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question comes to $2,474 per year (or $254/month) for combined home and contents cover, with a building sum insured of $700,000 and contents valued at $80,000. The building excess sits at $3,000, while the contents excess is a more modest $500.

Our price rating for this quote is FAIR — around average for the suburb. That's actually a meaningful result. In a state like Queensland, where extreme weather events and elevated rebuild costs push premiums well above the national norm, landing near the suburb average is a reasonable outcome — particularly for a well-built brick veneer home on a slab foundation.

It's worth noting that "fair" doesn't necessarily mean you can't do better. It means this quote is competitive relative to what most comparable Pelican Waters homeowners are paying, but there may still be room to shop around.

---

How Pelican Waters Compares

To understand whether $2,474 is genuinely competitive, it helps to zoom out and look at the broader data. Based on 130 quotes collected for Pelican Waters (4551):

| Benchmark | Premium |

|---|---|

| Suburb 25th percentile | $2,241/yr |

| This quote | $2,474/yr |

| Suburb median | $3,243/yr |

| Suburb average | $3,758/yr |

| Suburb 75th percentile | $4,202/yr |

| LGA (Sunshine Coast) average | $7,249/yr |

| QLD state average | $9,129/yr |

| QLD state median | $3,903/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

This quote sits just above the suburb's 25th percentile and well below the suburb median of $3,243 — meaning it's cheaper than more than half of all quotes in the area. Compared to the Sunshine Coast LGA average of $7,249 and the Queensland state average of a staggering $9,129, this premium looks very attractive indeed.

The Queensland state average is heavily skewed by high-risk coastal and flood-prone areas further north, which is why the median ($3,903) is a more representative figure for most homeowners. Even so, this quote beats the state median by around $1,400 per year — a significant saving.

At the national level, the average premium of $5,347 reflects the diversity of risk profiles across Australia, from bushfire-prone regions in Victoria and NSW to cyclone corridors in Far North Queensland. The national median of $2,764 is the closest comparable figure to this quote, suggesting Pelican Waters homeowners with well-rated properties can achieve premiums broadly in line with the national middle ground.

---

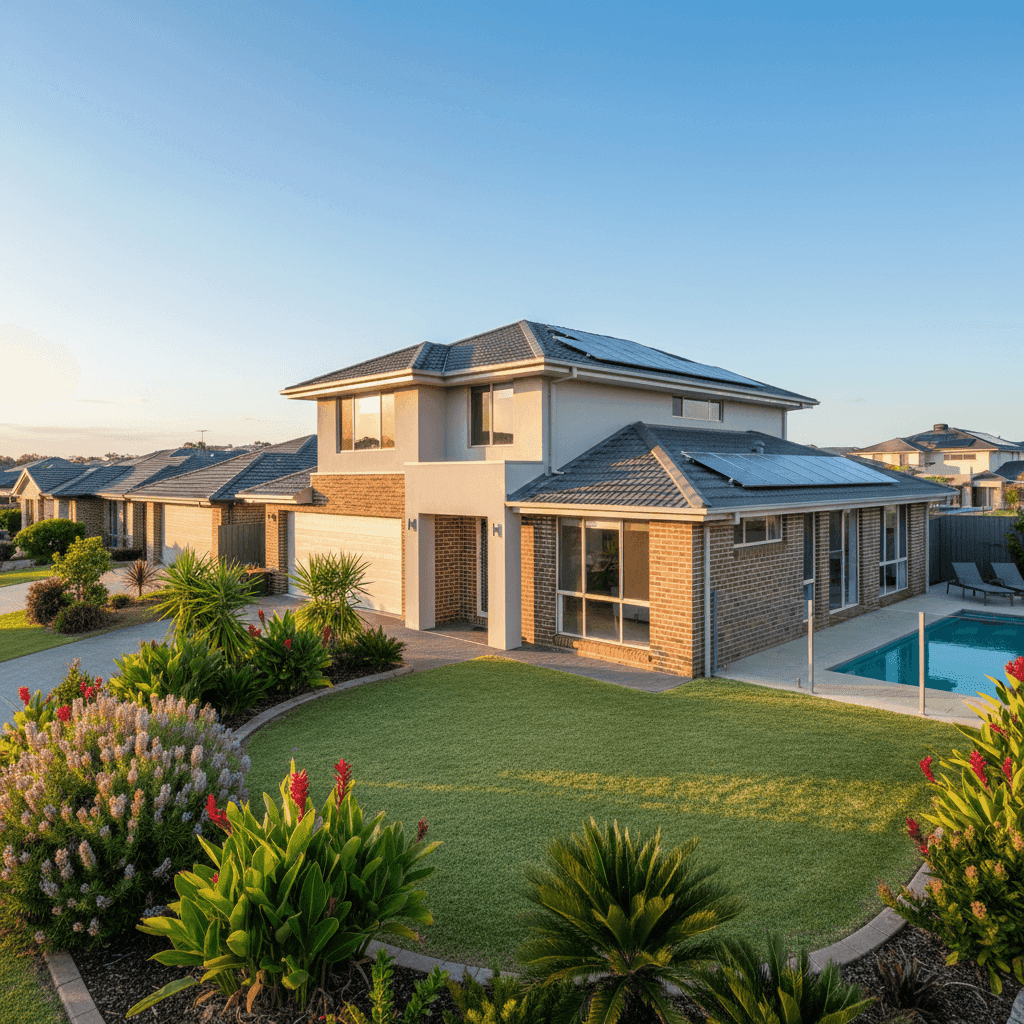

Property Features That Affect Your Premium

Several characteristics of this property work in its favour from an insurance pricing perspective.

Brick veneer construction is generally viewed favourably by insurers. It offers solid fire resistance and structural durability compared to lightweight cladding or weatherboard, which can translate to lower premiums.

Tiled roof is another positive. Terracotta and concrete tiles are considered more resilient than colorbond in certain weather scenarios and are a standard, well-understood material for insurers to price.

Slab foundation eliminates the underfloor risks associated with raised or stumped homes — such as moisture damage, pest ingress, or structural movement — which can otherwise inflate premiums.

Tiled flooring throughout reduces the risk of water damage claims compared to timber or carpet, and is particularly practical in a coastal Queensland climate.

Swimming pool adds a degree of liability exposure and increases the overall replacement cost of the property, which is reflected in the sum insured. Pools also require specific coverage consideration to ensure pumps, filtration systems, and surrounds are adequately protected.

Solar panels are an increasingly common feature in Southeast Queensland and add to the building's replacement value. It's important to confirm with your insurer that panels are explicitly included in your building cover — some policies treat them as an optional extra or may apply sub-limits.

Ducted climate control is a significant fixed asset in the home. As with solar, it's worth checking whether your policy covers the full replacement cost of a ducted system, which can run into tens of thousands of dollars.

Notably, this property is not located in a cyclone risk zone, which is a meaningful factor in keeping the premium lower than many comparable Queensland properties. Homes in cyclone-designated areas — particularly north of Bundaberg — face substantially higher premiums due to the engineering requirements and claim frequency associated with tropical weather systems.

---

Tips for Homeowners in Pelican Waters

1. Review your building sum insured regularly Construction costs have risen sharply in recent years across Southeast Queensland. A $700,000 sum insured may have been appropriate at policy inception, but it's worth cross-checking against a current building cost estimator to ensure you're not underinsured. Underinsurance can leave you significantly out of pocket in the event of a major claim.

2. Confirm solar and pool equipment are fully covered Ask your insurer specifically whether solar panels and pool equipment (including pumps, filters, and heating systems) are covered under the standard building definition or whether they require separate endorsement. Don't assume — get it in writing.

3. Consider your excess structure carefully This quote carries a $3,000 building excess, which is on the higher side. A higher excess typically reduces your annual premium, but it means more out-of-pocket cost at claim time. Think about what you could comfortably afford to self-insure before accepting a high excess in exchange for a lower premium.

4. Compare quotes annually Even if your current quote is competitive, the insurance market shifts each year. Insurers reprice based on claims experience, reinsurance costs, and risk modelling updates. Running a fresh comparison at renewal through CoverClub takes only a few minutes and could reveal a materially better deal.

---

Get a Quote for Your Pelican Waters Home

Whether you're renewing your existing policy or insuring a property for the first time, it pays to compare. CoverClub makes it easy to see what multiple insurers would charge for your specific home — no jargon, no pressure, just clear comparisons. Start your free quote today and find out where your premium really sits.