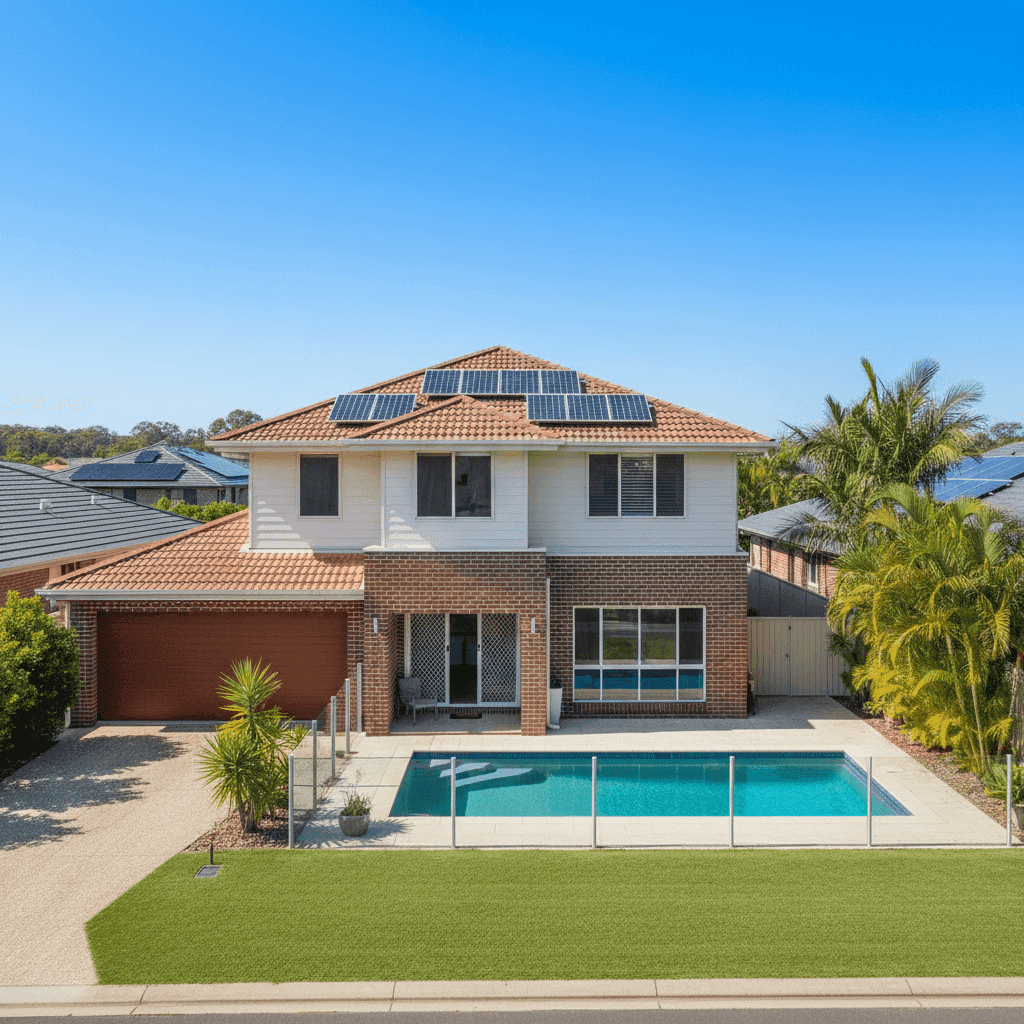

If you own a free standing home in Pelican Waters, QLD 4551, you're living in one of the Sunshine Coast's most sought-after residential pockets — a waterfront suburb known for its canals, golf course, and relaxed coastal lifestyle. But like any homeowner, you'll want to know whether your building insurance premium is reasonable, or whether you're paying more than you should be.

This article breaks down a real building-only insurance quote for a 3-bedroom, 2-bathroom free standing home in Pelican Waters, comparing it against local, state, and national benchmarks to help you make an informed decision.

---

Is This Quote Fair?

The quote in question comes in at $1,849 per year (or $181/month) for building-only cover with a $700,000 sum insured and a $3,000 building excess. CoverClub's pricing engine rates this as CHEAP — below average for the area.

To put that in perspective: the average home insurance premium across Pelican Waters sits at $3,838 per year, with a median of $3,686. This quote is roughly 52% below the suburb average — a substantial saving that's hard to ignore. Even compared to the 25th percentile of quotes in the suburb ($2,576/yr), this premium is still meaningfully lower, placing it well into the most competitive tier of pricing available in this postcode.

In short: yes, this is a genuinely competitive quote. Homeowners comparing options in this area should treat any premium in this range as a strong benchmark.

---

How Pelican Waters Compares

Understanding where Pelican Waters sits in the broader insurance landscape is useful context — especially given the Sunshine Coast's exposure to weather-related risks.

Based on data from 125 quotes analysed for Pelican Waters (QLD 4551):

| Benchmark | Premium |

|---|---|

| This quote | $1,849/yr |

| Suburb 25th percentile | $2,576/yr |

| Suburb median | $3,686/yr |

| Suburb average | $3,838/yr |

| Suburb 75th percentile | $4,549/yr |

| QLD state average | $4,547/yr |

| QLD state median | $3,931/yr |

| National average | $2,965/yr |

| National median | $2,716/yr |

| Sunshine Coast LGA average | $7,249/yr |

A few things stand out here. First, Queensland premiums are significantly elevated compared to the national average — the state average of $4,547 is more than 53% higher than the national figure of $2,965. This reflects Queensland's heightened exposure to cyclones, flooding, storms, and hail events, all of which drive up insurer risk models across the state.

Second, the Sunshine Coast LGA average of $7,249 is strikingly high — more than double the national average. This is partly driven by higher-value properties in the region and the coastal risk profile of many suburbs within the LGA. Pelican Waters, while a canal-side suburb, benefits from its "No Cyclone Risk" classification, which likely contributes to more moderate premiums compared to other parts of the Sunshine Coast and Far North Queensland.

---

Property Features That Affect Your Premium

Several characteristics of this property work together to influence its insurance cost — some favourably, others adding complexity.

Construction type — Brick Veneer walls & tiled roof Brick veneer construction with a tiled roof is generally viewed positively by insurers. Both materials offer solid resistance to fire and wind, and tiled roofs in particular tend to have good longevity. This combination typically attracts lower premiums compared to timber-framed or Colorbond alternatives.

Slab foundation A concrete slab foundation is low-maintenance and resistant to moisture-related issues like subfloor rot or termite damage. Insurers generally consider slab homes lower risk than those on stumps or piers, particularly in Queensland's humid climate.

Relatively modern build (2016) At just under a decade old, this home is well within the age range that insurers consider favourably. Newer builds are more likely to comply with current building codes, use modern materials, and have up-to-date plumbing and electrical systems — all of which reduce claims risk.

Swimming pool A pool adds replacement value to the property and can influence the sum insured calculation. It also introduces some liability considerations, though these are typically more relevant for home and contents or landlord policies. Pool fencing compliance in Queensland is a legal requirement and may be assessed as part of the risk profile.

Solar panels Solar panels are now standard on many Queensland homes, but they do add to the insured value of the building. Panels are typically covered under building insurance for storm, hail, and fire damage. Ensuring your sum insured adequately accounts for the replacement cost of your solar system is important.

Ducted climate control Ducted air conditioning systems are a significant fixed asset in Queensland homes — and a common source of claims. Like solar, these should be factored into your sum insured to avoid being underinsured.

No cyclone risk classification This is a meaningful factor. Pelican Waters is not classified as a cyclone risk area, which removes one of the largest premium drivers for coastal Queensland properties. Suburbs further north — particularly in Far North Queensland — can see premiums two to three times higher purely due to cyclone loading.

---

Tips for Homeowners in Pelican Waters

1. Review your sum insured annually Construction costs have risen sharply in recent years. A $700,000 sum insured may be appropriate today, but it's worth recalculating your rebuild cost each year — especially given the cost of materials, labour, and the inclusion of features like solar panels and ducted air conditioning. Underinsurance is one of the most common and costly mistakes homeowners make.

2. Don't assume your pool and solar are fully covered Check your policy's Product Disclosure Statement (PDS) to confirm that your pool, solar panels, and associated equipment are explicitly covered — and at what limits. Some policies cap coverage on these items or exclude certain types of damage.

3. Compare quotes at renewal time Even with a competitive premium like this one, the insurance market changes every year. Insurers reprice based on claims experience, reinsurance costs, and risk modelling updates. What's cheap today may not be at your next renewal. Get a fresh comparison at CoverClub before you auto-renew.

4. Consider your excess carefully This policy carries a $3,000 building excess, which is on the higher end. A higher excess typically reduces your premium, but it means more out-of-pocket cost at claim time. Make sure you're comfortable with this trade-off — particularly for weather events where multiple claims might arise in a short period.

---

Compare Your Home Insurance Today

Whether you're reviewing your current policy or shopping for the first time, CoverClub makes it easy to see how your premium stacks up. We analyse quotes across dozens of insurers and benchmark them against real data from your suburb, state, and nationally — so you always know where you stand.

Get a home insurance quote for your Pelican Waters property →