If you own a free standing home in Pelican Waters, QLD 4551, you're living in one of the Sunshine Coast's most appealing coastal suburbs — and like many Queensland homeowners, you're probably wondering whether your home insurance premium is fair. This article breaks down a recent home and contents insurance quote for a four-bedroom brick veneer property in Pelican Waters, comparing it against suburb, state, and national benchmarks so you can make a more informed decision.

---

Is This Quote Fair?

The quote in question comes in at $1,613 per year (or roughly $158 per month) for combined home and contents cover, with a building sum insured of $648,000 and contents valued at $50,000. The building excess is $3,000 and the contents excess is $1,000.

Our pricing analysis rates this quote as CHEAP — below average for the area. That's a meaningful distinction. Based on 125 quotes collected for Pelican Waters, the suburb average premium sits at $3,838 per year, with a median of $3,686. That means this quote is saving the homeowner over $2,200 annually compared to what most locals are paying — a significant sum by any measure.

Even when stacked against the 25th percentile of suburb quotes ($2,576/yr), this premium still comes in comfortably below the cheapest quarter of the market. In short, this is a genuinely competitive result.

---

How Pelican Waters Compares

To put things in perspective, here's how premiums in Pelican Waters sit relative to broader benchmarks:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Pelican Waters (4551) | $3,838/yr | $3,686/yr |

| Queensland | $4,547/yr | $3,931/yr |

| National | $2,965/yr | $2,716/yr |

| Sunshine Coast LGA | $4,608/yr | — |

A few things stand out here. First, Queensland premiums are substantially higher than the national average — a reflection of the state's elevated exposure to weather-related risks including storms, flooding, and hail. The Sunshine Coast LGA average of $4,608/yr is even higher than the state figure, underlining that coastal and near-coastal properties in this region attract significant insurer attention.

Pelican Waters itself tracks slightly below the broader Sunshine Coast LGA average, which is a positive sign for homeowners in the suburb. Still, at $3,686–$3,838 on average, locals are paying well above the national median of $2,716. The quote analysed here — at $1,613 — is nearly 60% below the suburb average, making it an exceptional outcome.

---

Property Features That Affect Your Premium

Several characteristics of this property likely contribute to its favourable premium. Understanding these factors can help you assess your own situation.

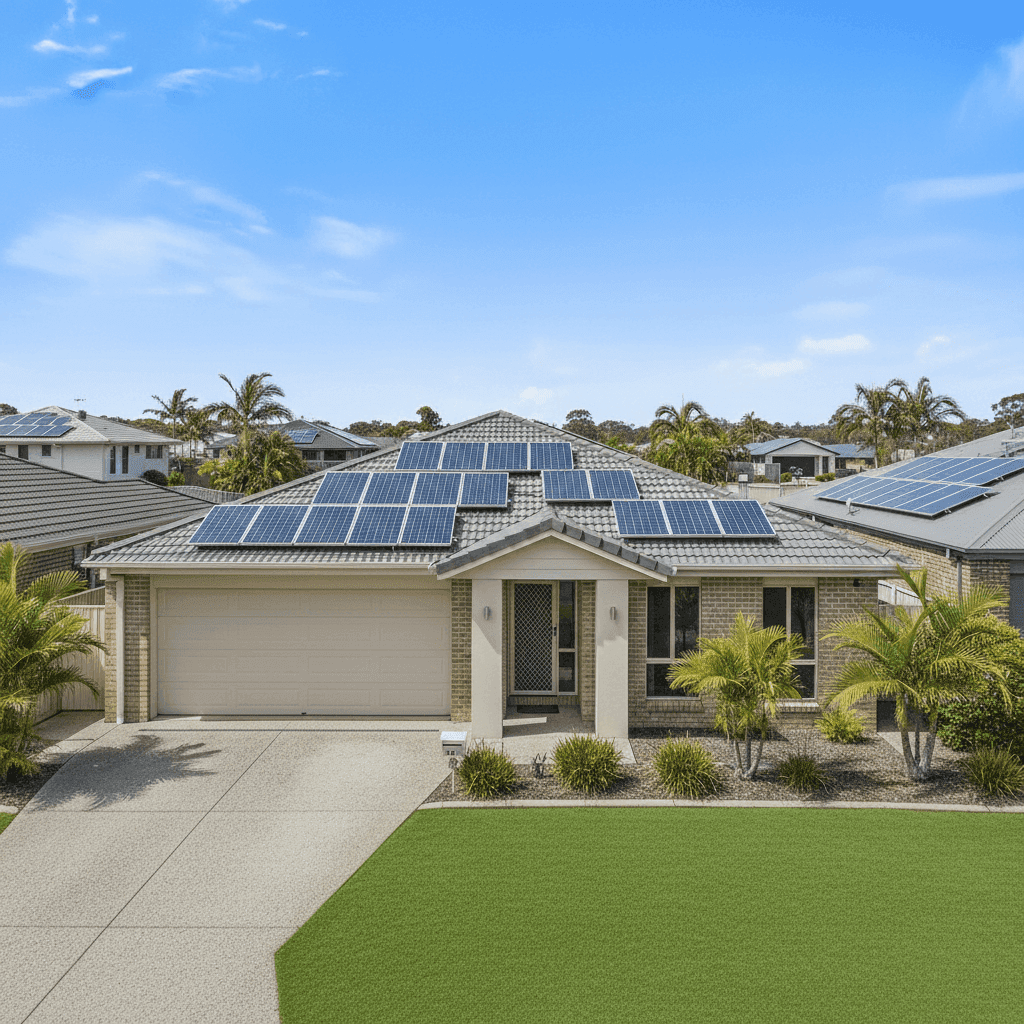

Brick Veneer Construction Brick veneer walls are generally viewed favourably by insurers. They offer solid resistance to fire and wind compared to timber-framed cladding, which can translate to lower rebuild risk and, in turn, lower premiums.

Tiled Roof Concrete or terracotta tiles are a durable roofing choice that tends to perform well in hail and wind events — a key consideration for Queensland properties. Tile roofs typically attract better pricing than corrugated iron or older materials in storm-prone regions.

Slab Foundation A concrete slab foundation is one of the most stable and insurer-friendly foundation types. It eliminates the underfloor space associated with stumped or suspended floors, reducing exposure to moisture, pests, and structural movement.

Built in 2005 At roughly 20 years old, this home sits in a sweet spot for insurers — modern enough to meet contemporary building codes (which improved significantly after cyclone and flood events of the 1990s) but not so new as to carry a premium for cutting-edge finishes.

Solar Panels The presence of rooftop solar panels adds a modest layer of complexity for insurers, as panels need to be covered for damage and can affect roof repair costs. However, they're now extremely common and most policies accommodate them without dramatic premium increases.

No Pool, No Cyclone Risk Zone The absence of a pool removes a source of liability and potential damage claims. Importantly, Pelican Waters falls outside designated cyclone risk areas, which is a meaningful pricing advantage compared to properties further north in Queensland.

Standard Fittings With standard-quality fittings throughout, the cost to rebuild or repair this home is more predictable and moderate compared to properties with high-end or bespoke finishes, keeping the sum insured — and the premium — grounded.

---

Tips for Homeowners in Pelican Waters

Whether you're reviewing an existing policy or shopping for new cover, here are some practical steps worth considering.

1. Review Your Sum Insured Annually Construction costs in Queensland have risen sharply over recent years. A building sum insured of $648,000 for a 244 sqm home is a reasonable starting point, but it's worth checking against current per-square-metre rebuild costs in your area each year. Being underinsured at claim time can be a costly mistake.

2. Consider Your Excess Carefully This quote carries a $3,000 building excess and a $1,000 contents excess. A higher excess typically lowers your premium, but make sure you could comfortably cover that amount out of pocket in the event of a claim. If cash flow is a concern, a lower excess with a slightly higher premium may offer better peace of mind.

3. Don't Assume Loyalty Pays Many homeowners in Pelican Waters are paying well above the suburb median without realising it. The wide spread between the 25th percentile ($2,576/yr) and the 75th percentile ($4,549/yr) shows just how much premiums vary. Shopping around — even just once a year — can uncover significant savings.

4. Check What's Covered for Storm and Water Damage Given the Sunshine Coast's exposure to severe weather, it's worth reading your Product Disclosure Statement carefully to understand how your policy handles storm surge, rainwater ingress, and flash flooding. These distinctions matter enormously when a claim arises.

---

Compare Your Own Quote

Curious how your current premium stacks up? CoverClub makes it easy to benchmark your home insurance costs against real data from your suburb and state. Whether you're in Pelican Waters or anywhere else in Australia, you can get a quote and compare in minutes — no jargon, no pressure. Explore the full Pelican Waters insurance stats to see exactly where you stand.