If you own — or are thinking of buying — a free standing home in Pelican Waters, QLD 4551, understanding what you should be paying for building insurance is one of the smartest financial moves you can make. Premiums in coastal Queensland can vary enormously, and knowing where your quote sits relative to the market can mean the difference between a great deal and quietly overpaying for years.

This article breaks down a real building insurance quote for a four-bedroom, two-bathroom free standing home in Pelican Waters — and puts it in context against suburb, state, and national benchmarks.

---

Is This Quote Fair?

The short answer: yes — exceptionally so.

This property received an annual building-only premium of $1,930 per year (or $189 per month), with a building excess of $2,000. CoverClub's pricing engine rates this as CHEAP — below average for the area, and the data backs that up strongly.

The suburb average for Pelican Waters sits at $3,838 per year, based on a sample of 125 quotes. That means this particular quote comes in at roughly half the local average — a saving of nearly $1,900 annually compared to what many neighbours are likely paying.

Even against the 25th percentile — meaning the cheapest quarter of quotes in the suburb — this premium of $1,930 still undercuts the $2,576 benchmark. In other words, this is among the most competitively priced quotes recorded for this postcode, not just below average.

For context, Queensland as a whole is one of the most expensive states for home insurance in the country, with a state average of $4,547 per year. This quote sits at less than half that figure — a remarkable outcome for a Sunshine Coast property.

---

How Pelican Waters Compares

To appreciate just how well-priced this quote is, it helps to zoom out and look at the broader picture.

| Benchmark | Annual Premium |

|---|---|

| This quote | $1,930 |

| Pelican Waters 25th percentile | $2,576 |

| Pelican Waters median | $3,686 |

| Pelican Waters average | $3,838 |

| Pelican Waters 75th percentile | $4,549 |

| Sunshine Coast LGA average | $4,608 |

| QLD state average | $4,547 |

| QLD state median | $3,931 |

| National average | $2,965 |

| National median | $2,716 |

What stands out here is that even the national average of $2,965 is comfortably above this quote. Queensland consistently attracts higher premiums than the rest of Australia due to its exposure to severe weather events — cyclones, storms, and flooding — which makes a sub-$2,000 annual premium in this region genuinely unusual.

The Sunshine Coast LGA average of $4,608 further underscores how well this property has fared. Homeowners across the broader local government area are paying more than double what this quote reflects.

---

Property Features That Affect Your Premium

Several characteristics of this property likely contribute to its favourable pricing:

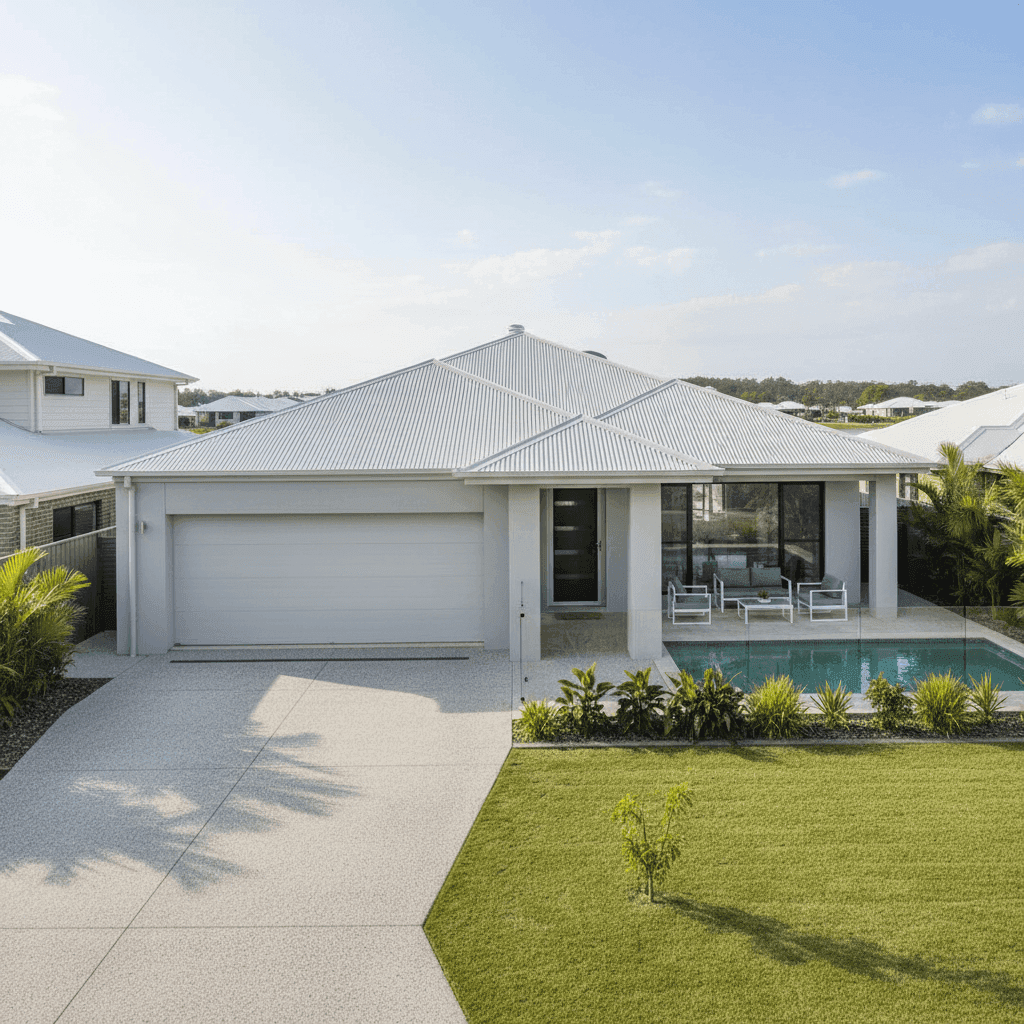

Hebel external walls Hebel (autoclaved aerated concrete) panels are highly regarded by insurers. They offer excellent fire resistance, are structurally robust, and perform well in high-wind conditions — all factors that reduce the likelihood of a major claim. This is a meaningful advantage over older brick veneer or weatherboard construction.

Colorbond steel roof Steel roofing is durable, low-maintenance, and performs well in storms. Colorbond in particular is a well-understood product for Australian insurers, and its longevity reduces the risk of weather-related roof damage claims compared to terracotta tiles or ageing materials.

Concrete slab foundation Slab foundations are considered low-risk by most underwriters. They are resistant to subsidence and moisture ingress, and are the standard for modern Queensland construction.

New build (2025) A brand-new home carries none of the legacy risks associated with ageing properties — no deteriorating wiring, no worn plumbing, no outdated construction methods. Insurers price new builds more favourably because the probability of structural and mechanical failure is significantly lower.

No cyclone risk classification While Pelican Waters is coastal, it falls outside the formal cyclone risk zone that affects properties further north in Queensland. This is a major pricing factor — cyclone-rated premiums can add thousands of dollars to annual costs.

Pool on property A swimming pool does introduce a modest liability consideration, which can nudge premiums slightly upward. However, given the overall profile of this property, it clearly hasn't had a significant impact on the final premium.

Tiled flooring and ducted climate control These features influence the sum insured ($1,090,000) more than the premium directly, but an accurate sum insured is critical — underinsurance at claim time can be financially devastating.

---

Tips for Homeowners in Pelican Waters

1. Review your sum insured annually Construction costs in South East Queensland have risen sharply in recent years. A sum insured of $1,090,000 for a 214 sqm home built in 2025 is reasonable today, but building costs can shift quickly. Use a quantity surveyor's estimate or an online calculator to verify your coverage each year at renewal.

2. Don't assume loyalty pays Many insurers quietly increase premiums at renewal without any change to your risk profile. Even if your current premium is competitive, it's worth running a comparison every 12 months. CoverClub makes this straightforward — get a fresh quote here to see where the market sits at renewal time.

3. Understand your excess structure This policy carries a $2,000 building excess. A higher excess generally lowers your premium, but make sure it's an amount you could comfortably cover out of pocket in the event of a claim. If cash flow is a concern, consider whether a lower excess option is worth the additional premium cost.

4. Keep documentation of your home's features Insurers may ask for evidence of construction materials, particularly for newer builds using non-standard materials like Hebel. Keep copies of your building contract, specifications, and any council approvals. This can streamline the claims process and support your case if a dispute arises.

---

Compare Your Own Quote

Whether you're a new homeowner in Pelican Waters or coming up for renewal, it pays to know what the market looks like. The data is clear — premiums in this suburb and across Queensland vary dramatically, and the difference between the cheapest and most expensive quotes can be thousands of dollars per year.

CoverClub aggregates real quote data to help Australian homeowners make informed decisions. Start a quote today at CoverClub and see how your premium stacks up against your neighbours — you might be surprised by what you find.