If you own a free standing home in Pelican Waters, QLD 4551, you're likely no stranger to the balancing act of finding quality home insurance at a reasonable price. Situated on the Sunshine Coast, Pelican Waters is a sought-after coastal suburb where property values — and insurance premiums — can vary enormously. This article breaks down a real home and contents insurance quote for a four-bedroom property in the area, benchmarks it against local, state, and national data, and offers practical tips to help you get the most out of your cover.

---

Is This Quote Fair?

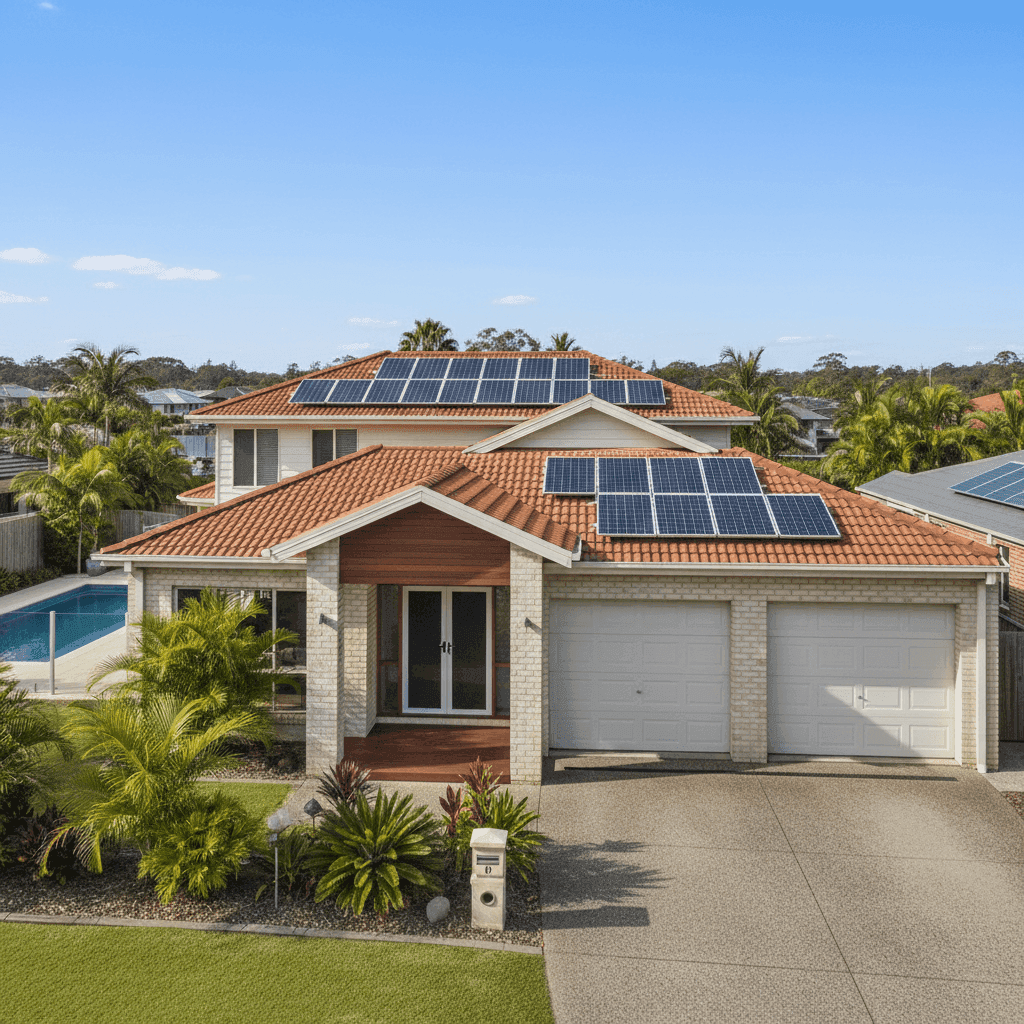

The annual premium for this quote comes in at $2,244 per year (or $224/month), covering both building and contents for a 4-bedroom, 3-bathroom brick veneer home with a building sum insured of $692,000 and contents valued at $50,000.

Our price rating for this quote is CHEAP — below average for the area. That's genuinely good news for the homeowner. Based on 125 quotes collected for Pelican Waters, the suburb average sits at $3,838/year and the median at $3,686/year. This quote lands well below even the 25th percentile of $2,576/year — meaning it's cheaper than at least 75% of comparable quotes in the suburb.

To put it plainly: if you're paying around $2,244 a year for this level of cover in Pelican Waters, you're doing better than most of your neighbours.

---

How Pelican Waters Compares

Pelican Waters sits within the Sunshine Coast LGA, where the average home insurance premium is a steep $4,608/year — one of the higher regional averages in Queensland. Zooming out to the state level, the Queensland average is $4,547/year with a median of $3,931/year, reflecting the elevated risk profile of many Queensland properties due to flooding, storms, and in some areas, cyclone exposure.

Compared to the national average of $2,965/year (median: $2,716/year), Queensland homeowners are paying significantly more — a gap that speaks to the state's challenging climate and geography.

| Benchmark | Annual Premium |

|---|---|

| This Quote | $2,244 |

| Pelican Waters 25th Percentile | $2,576 |

| Pelican Waters Median | $3,686 |

| Pelican Waters Average | $3,838 |

| Pelican Waters 75th Percentile | $4,549 |

| QLD State Average | $4,547 |

| National Average | $2,965 |

The fact that this quote sits below both the suburb median and the national average is notable. For a property of this size and specification on the Sunshine Coast, it represents strong value.

---

Property Features That Affect Your Premium

Several characteristics of this property play a meaningful role in determining its insurance premium.

Brick Veneer Construction

Brick veneer external walls are generally viewed favourably by insurers. They offer solid fire resistance and structural durability compared to timber or clad alternatives, which can translate to lower premiums. This property's brick veneer construction is likely contributing to its competitive rate.

Tiled Roof

A tiled roof is another feature that tends to attract more modest premiums. Tiles are durable, fire-resistant, and long-lasting — particularly relevant on the Sunshine Coast, where summer storms can be intense. That said, tiles can be more expensive to repair after hail events, so it's worth checking whether your policy includes storm and hail cover as standard.

Concrete Slab Foundation

Built on a slab foundation, this home avoids some of the underfloor moisture and pest-related risks associated with raised or timber-framed subfloors. Slab construction is common in Queensland and generally considered a neutral-to-positive factor by underwriters.

Swimming Pool

A pool adds both value and complexity to a home insurance policy. It increases the insured asset's replacement cost and can introduce liability considerations. Homeowners should confirm their policy explicitly covers pool infrastructure, including pumps, filters, and fencing, and check whether public liability cover extends to pool-related incidents.

Solar Panels

With solar panels installed, it's essential to verify that your building sum insured accounts for the full replacement cost of the system. Solar panels are typically covered as part of the building, but some policies have sub-limits or exclusions for panels. Given the rising cost of quality solar systems, under-insuring here could be a costly oversight.

2007 Build — A Sweet Spot

Constructed in 2007, this home benefits from relatively modern building standards without the premium loading that can sometimes apply to newer builds during the first few years. It's old enough to have a proven track record structurally, yet modern enough to meet contemporary safety codes.

No Cyclone Risk

Unlike parts of Far North Queensland, Pelican Waters is not classified as a cyclone risk area. This is a significant factor — cyclone premiums in high-risk zones can add hundreds or even thousands of dollars to an annual policy. The absence of this loading helps explain why this quote is competitive relative to the broader Queensland average.

---

Tips for Homeowners in Pelican Waters

1. Review Your Building Sum Insured Annually

Construction costs in South East Queensland have risen sharply in recent years. A sum insured of $692,000 for a 214 sqm home may be appropriate today, but it's worth recalculating each year using a building cost estimator to avoid being underinsured at claim time. Most insurers won't automatically adjust your sum insured to keep pace with inflation unless you opt into an indexed cover option.

2. Confirm Solar Panel and Pool Coverage

As noted above, both solar panels and swimming pools can fall into grey areas in standard policies. Before renewing, call your insurer and ask specifically: Are my solar panels covered for accidental damage and storm damage? Is my pool equipment included in the building sum insured? What is the public liability limit for pool-related incidents? Getting clear answers now prevents nasty surprises later.

3. Consider Your Excess Strategically

This policy carries a $3,000 building excess and a $1,000 contents excess. A higher excess typically lowers your premium, but it means more out-of-pocket costs at claim time. If a $3,000 outlay would be financially stressful, it may be worth requesting a quote with a lower excess — even if the annual premium increases slightly. Conversely, if you're financially comfortable absorbing that cost, the current excess structure is helping keep premiums down.

4. Compare at Renewal — Every Year

Even if you're happy with your current insurer, the home insurance market is competitive and premiums shift year to year. The fact that this quote is rated cheap for Pelican Waters doesn't mean it will remain the best deal at renewal. Loyalty doesn't always pay in insurance — shopping around annually is one of the most effective ways to keep your costs in check.

---

Get a Quote for Your Pelican Waters Home

Whether you're buying, renewing, or just curious about what you should be paying, CoverClub makes it easy to compare home and contents insurance quotes side by side. See how your premium stacks up against the suburb average — and find out if you're getting a fair deal. Get a quote at CoverClub today and take the guesswork out of home insurance.