If you own a free standing home in Peregian Springs, QLD 4573, you're living in one of the Sunshine Coast's most sought-after residential pockets. Nestled within the Noosa local government area, Peregian Springs is a master-planned community popular with families — and like any homeowner, keeping your insurance costs in check matters. This article breaks down a real home and contents insurance quote for a 3-bedroom, 2-bathroom brick veneer home in the suburb, and puts the numbers into context so you can judge whether you're getting a fair deal.

---

Is This Quote Fair?

The annual premium for this property came in at $2,570 per year (or $246 per month), covering both building ($850,000 sum insured) and contents ($150,000). Based on CoverClub's pricing data, this quote is rated CHEAP — below the suburb average.

To put that in plain terms: this homeowner is paying less than most of their neighbours for comparable cover. The building excess and contents excess are both set at $5,000, which is on the higher side and is a key reason the premium is lower. A higher excess means you're agreeing to cover more of any claim yourself, which reduces the insurer's risk and, in turn, your upfront cost. It's a legitimate strategy — just make sure you could comfortably cover that $5,000 out of pocket if something went wrong.

Overall, at $2,570 annually, this quote represents solid value for a well-built modern home in a low-risk coastal suburb.

---

How Peregian Springs Compares

Understanding where your premium sits relative to local and broader benchmarks is one of the most useful things you can do as a homeowner. Here's how this quote stacks up:

| Benchmark | Premium |

|---|---|

| This quote | $2,570/yr |

| Suburb average (Peregian Springs) | $3,113/yr |

| Suburb median | $3,125/yr |

| Suburb 25th percentile | $2,603/yr |

| Suburb 75th percentile | $3,615/yr |

| QLD state average | $9,129/yr |

| QLD state median | $3,903/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

| LGA average (Noosa) | $18,770/yr |

Based on 31 quotes collected for the Peregian Springs 4573 postcode.

A few things stand out here. First, this quote sits just below the suburb's 25th percentile — meaning it's cheaper than roughly 75% of quotes in the area. That's a genuinely competitive result.

Second, while the QLD state average of $9,129 per year might seem alarming, it's heavily skewed by high-risk areas in Far North Queensland — regions prone to cyclones, flooding, and severe weather events. The QLD median of $3,903 is a far more representative figure for south-east Queensland suburbs like Peregian Springs.

Third, the Noosa LGA average of $18,770 per year is eye-watering, but again reflects the significant coastal and flood exposure that affects many properties across the broader Noosa region. Peregian Springs, being an inland master-planned estate, tends to attract more moderate premiums by comparison.

You can explore suburb-level data in more detail on the Peregian Springs insurance stats page, or check out national home insurance benchmarks to see how Queensland compares to the rest of Australia.

---

Property Features That Affect Your Premium

Insurance pricing isn't arbitrary — every detail of your home feeds into the risk calculation. Here's how the features of this particular property influence its premium:

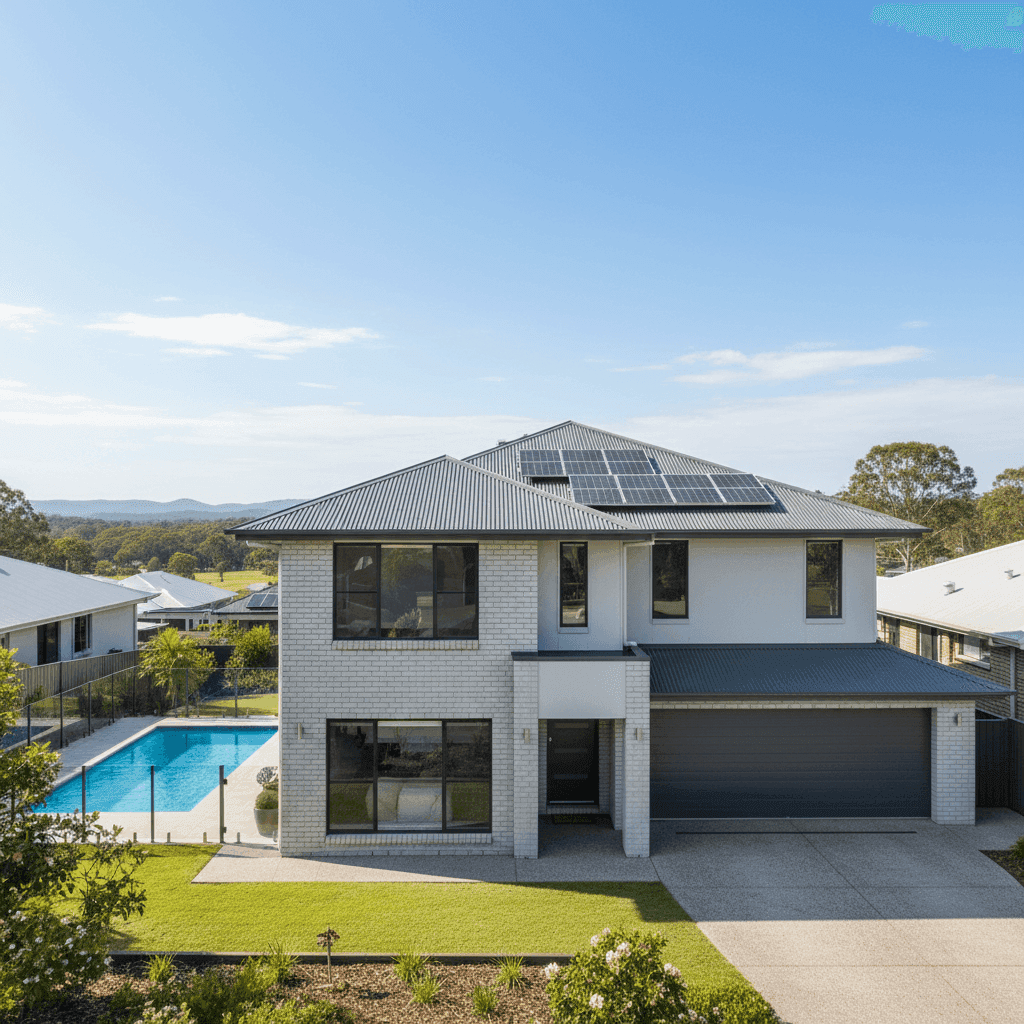

Brick veneer walls and Colorbond roof This is a strong combination from an insurer's perspective. Brick veneer offers solid structural integrity and good fire resistance, while steel/Colorbond roofing is durable, low-maintenance, and performs well in high-wind conditions. Homes with these materials typically attract lower premiums than those with timber frames or terracotta tiles.

Slab foundation A concrete slab foundation is the standard for homes built in Queensland from the 1990s onwards. It's considered a stable, low-risk foundation type — no subfloor cavity means fewer pest and moisture concerns for insurers.

Tile flooring and standard fittings Tiled flooring throughout is practical and relatively inexpensive to replace compared to hardwood timber or premium stone. Standard-quality fittings also keep the replacement cost estimate grounded, which helps avoid over-insurance.

Built in 2005 At roughly 20 years old, this home is modern enough to meet contemporary building codes but old enough that some wear is expected. Insurers generally view homes from this era favourably — they're past the "new build" warranty period but not yet at the age where major structural concerns arise.

Swimming pool A pool adds some liability exposure and increases the overall replacement cost of the property, which can nudge premiums upward slightly. It's worth ensuring your policy explicitly covers pool infrastructure (fencing, pumps, filtration systems) under the building sum insured.

Solar panels Solar systems are increasingly common in Queensland and most modern home insurance policies cover them under the building sum insured — but it's worth confirming this with your insurer. Panels are expensive to replace and can be damaged by hail or storm events.

No cyclone risk Peregian Springs falls outside designated cyclone risk zones, which is a meaningful premium advantage. Cyclone cover is a major cost driver for properties in Far North Queensland, so homeowners in the south-east corner of the state benefit from its absence.

---

Tips for Homeowners in Peregian Springs

1. Review your sum insured annually Construction costs have risen significantly in recent years. The $850,000 building sum insured on this policy should be reviewed each year to ensure it reflects current rebuild costs — not the original purchase price or market value. Underinsurance is one of the most common and costly mistakes homeowners make.

2. Understand your excess before you commit A $5,000 excess is helping keep this premium low, but it's not the right choice for everyone. If a $5,000 out-of-pocket expense would be a stretch, consider adjusting your excess to a more manageable level — even if it means a slightly higher annual premium.

3. Confirm solar panels and pool equipment are covered Ask your insurer specifically whether your solar system and pool equipment are included under the building sum insured. Some policies treat these as optional extras or have sub-limits. Getting clarity now avoids nasty surprises at claim time.

4. Compare quotes at renewal — every year Insurers regularly adjust their pricing models, and loyalty doesn't always pay. Even if your current premium feels reasonable, it's worth running a fresh comparison at each renewal. The difference between the cheapest and most expensive quotes in Peregian Springs spans over $1,000 per year — that's real money.

---

Ready to Compare Home Insurance in Peregian Springs?

Whether you're renewing an existing policy or insuring a new purchase, CoverClub makes it easy to see how your quote stacks up against real data from your suburb. Get a home insurance quote today and find out if you're paying a fair price — or leaving money on the table.