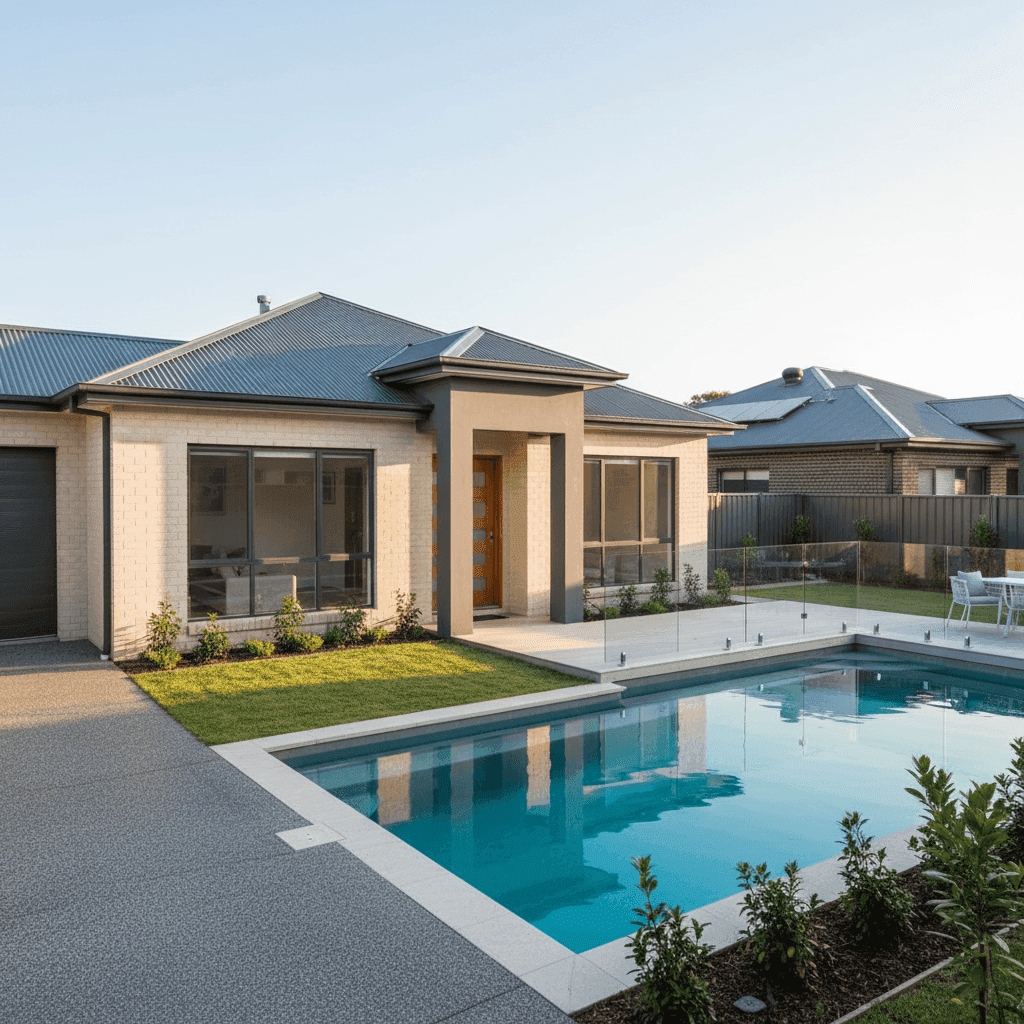

Picnic Point is a quiet, leafy suburb in Sydney's south-west, sitting along the Georges River in the Canterbury-Bankstown local government area. It's a popular spot for families, and properties here tend to be well-established — though newer builds like this 2015 semi detached are becoming more common. If you own or are considering insuring a home in this area, understanding what a fair premium looks like can save you hundreds of dollars a year.

This article breaks down a real home and contents insurance quote for a four-bedroom, three-bathroom semi detached in Picnic Point, and puts it in context against suburb, state, and national benchmarks.

---

Is This Quote Fair?

The annual premium for this property came in at $1,511 per year (or $149/month), covering a building sum insured of $800,000 and contents valued at $80,000. The building excess is $2,000 and the contents excess is $600.

Our price rating for this quote is CHEAP — below average for the area. That's a meaningful result. Based on data from 37 quotes collected in the Picnic Point postcode, the suburb average sits at $3,574 per year and the median at $3,400 per year. This quote comes in at less than half the local average — a significant saving of over $2,000 annually compared to what many neighbours are paying.

To put it plainly: if you're paying anywhere near the suburb average for a similar property, there's a strong case for shopping around.

---

How Picnic Point Compares

It's worth zooming out to understand how premiums in this suburb sit relative to broader benchmarks.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Picnic Point (2213) | $3,574/yr | $3,400/yr |

| NSW State | $3,801/yr | $3,410/yr |

| National | $2,965/yr | $2,716/yr |

| Canterbury-Bankstown LGA | $9,344/yr | — |

A few things stand out here. First, Picnic Point premiums are broadly in line with the NSW state average of $3,801/yr, which suggests the suburb doesn't carry any dramatic risk loading compared to the rest of the state. Second, both the suburb and state averages sit noticeably above the national average of $2,965/yr — a reflection of the higher property values and associated rebuild costs in greater Sydney.

The Canterbury-Bankstown LGA average of $9,344/yr is strikingly high, which likely reflects the diversity of property types, flood-affected areas, and high-value homes across the broader council area pulling that figure up. Picnic Point, sitting at the river's edge, may attract some flood or storm water risk loading for certain properties — though this particular quote doesn't appear to reflect that.

The 25th to 75th percentile range for Picnic Point runs from $2,919 to $3,986 per year, meaning three-quarters of quotes collected fall within this band. At $1,511, this quote sits well below even the cheapest quarter of the market — an exceptional result.

---

Property Features That Affect Your Premium

Insurers assess a wide range of property characteristics when calculating your premium. Here's how the features of this particular home are likely working in its favour — or against it.

Brick Veneer Walls Brick veneer is one of the most common external wall materials in Australian suburban homes, and insurers generally view it favourably. It offers good fire resistance and structural durability, which can help keep premiums in check compared to timber-framed or cladded homes.

Steel / Colorbond Roof Colorbond roofing is lightweight, durable, and highly resistant to corrosion and fire. It's a strong performer in storm conditions and tends to attract lower premiums than older materials like terracotta tiles or fibrous cement sheeting.

Concrete Slab Foundation Slab-on-ground construction is considered a stable and low-risk foundation type by most insurers. It's less susceptible to subsidence or pest-related damage than elevated or timber-stumped foundations.

Tile Flooring Hard flooring like tiles is generally seen as a lower-risk choice than carpet or timber boards, particularly in wet areas. It's less prone to water damage and easier to replace like-for-like.

Swimming Pool A pool adds value to a property but also introduces some liability and maintenance considerations. Most insurers will factor in the pool when calculating your premium — it's worth confirming your policy covers pool equipment and associated structures like fencing and pumps.

Ducted Climate Control Ducted air conditioning systems are a significant fixed asset and should be properly accounted for in both your building sum insured and contents cover, depending on how your insurer classifies them. Confirm with your insurer whether the system is covered under building or contents — misclassification can leave you underinsured.

2015 Construction Year A relatively modern build works in your favour. Newer homes are typically constructed to current building codes, which include improved fire safety, structural integrity, and weather-resistance standards. This reduces the likelihood of claims and is reflected in lower premiums.

---

Tips for Homeowners in Picnic Point

1. Don't assume your current insurer is competitive As this quote demonstrates, premiums for similar properties in Picnic Point can vary enormously — from under $1,600 to nearly $4,000 per year. Loyalty doesn't always pay in insurance; comparing quotes annually is one of the simplest ways to avoid overpaying.

2. Review your sum insured carefully With a building sum insured of $800,000, it's important this figure reflects the actual cost to rebuild — not the market value of the property. Rebuild costs include labour, materials, demolition, and council fees. Underinsurance is a common and costly mistake; use a building calculator or speak to a quantity surveyor if you're unsure.

3. Check your flood and stormwater coverage Picnic Point sits along the Georges River, and parts of the surrounding area carry flood risk. Even if your specific property isn't in a designated flood zone, stormwater and storm surge events can affect riverside suburbs. Read your Product Disclosure Statement (PDS) carefully to understand whether flood is included or excluded from your cover.

4. Secure your pool area properly Beyond the legal requirements for pool fencing in NSW, ensuring your pool area is well-maintained and compliant can reduce your liability exposure. Some insurers may ask about pool safety features during the quoting process — being able to confirm compliance may support a lower premium.

---

Compare Home Insurance Quotes in Picnic Point

Whether you're renewing your policy or buying for the first time, it pays to see what the market offers before you commit. CoverClub makes it easy to compare home and contents insurance quotes tailored to your property and postcode.

Get a quote for your Picnic Point home today and see how your current premium stacks up — you might be surprised at what you could save.