Pitt Town is a quiet semi-rural suburb tucked into the Hawkesbury region of New South Wales, known for its wide blocks, heritage streetscapes, and a growing number of modern family homes. If you own a free standing home here — particularly a newer, larger build — understanding what you should be paying for home and contents insurance is an important part of protecting one of your biggest assets. This article breaks down a real quote for a five-bedroom property in Pitt Town (postcode 2756) and puts it into context against local, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question comes in at $3,189 per year (or $286/month) for a combined home and contents policy, covering a building sum insured of $1,141,000 and $100,000 in contents. Both the building and contents excess are set at $1,000.

Our price rating for this quote is CHEAP — below average — which is genuinely good news for the homeowner. To put that in perspective:

- The suburb median for Pitt Town is $12,319/yr

- The NSW state median is $3,770/yr

- The national median is $2,764/yr

At $3,189/yr, this quote sits comfortably below the Pitt Town suburb median, slightly below the NSW state median, and only modestly above the national median — all while covering a high-value property with a $1.14 million building sum insured. For a home of this size and specification, that represents strong value.

It's worth noting that the suburb average premium is a striking $61,583/yr — heavily skewed by outlier quotes in the dataset (the sample size is 20 quotes). The 25th percentile sits at $5,383/yr and the 75th at $17,600/yr, which gives a more realistic picture of what Pitt Town homeowners are paying. This quote falls well below even the 25th percentile, making it an exceptionally competitive result.

---

How Pitt Town Compares

Insurance pricing varies enormously depending on location, and Pitt Town is an interesting case. As part of the Hawkesbury LGA (grouped here with Lithgow for statistical purposes), the local average premium is $11,842/yr — nearly four times what this quote costs.

Here's a quick snapshot of how the numbers line up:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $3,189 |

| Pitt Town Suburb Median | $12,319 |

| Pitt Town 25th Percentile | $5,383 |

| NSW State Median | $3,770 |

| National Median | $2,764 |

| NSW State Average | $9,528 |

| National Average | $5,347 |

| LGA Average | $11,842 |

You can explore more detailed pricing data for this postcode at the Pitt Town suburb stats page, or zoom out to see how NSW compares on the NSW state stats page. For a broader view, the national home insurance stats show how Australian premiums vary from coast to coast.

One key takeaway: averages can be misleading. The Pitt Town suburb average is dramatically inflated by a small number of very high quotes, which is common in areas with mixed property types, flood-affected land, or high-value rural holdings. The median is a far more reliable guide — and against that measure, this quote looks very competitive.

---

Property Features That Affect Your Premium

Several characteristics of this property work in the homeowner's favour when it comes to pricing — and a few add complexity. Here's what's likely influencing the premium:

Factors That May Reduce Risk (and Premium)

- Built in 2021: A recently constructed home benefits from modern building codes, better materials, and up-to-date safety standards. Insurers generally view newer builds as lower risk.

- Concrete external walls: Concrete is one of the most resilient wall materials available, offering excellent resistance to fire, impact, and the elements. This is a significant positive from an underwriting perspective.

- Steel/Colorbond roof: Colorbond roofing is highly regarded by insurers for its durability and resistance to weather events. It's also non-combustible, which reduces fire risk.

- Slab foundation: A concrete slab foundation is stable, low-maintenance, and generally preferred by insurers over older subfloor construction types.

- Not in a cyclone risk area: Properties in cyclone-prone regions of Australia attract significantly higher premiums. Being outside that zone is a meaningful cost advantage.

Features That Add Value (and Sum Insured)

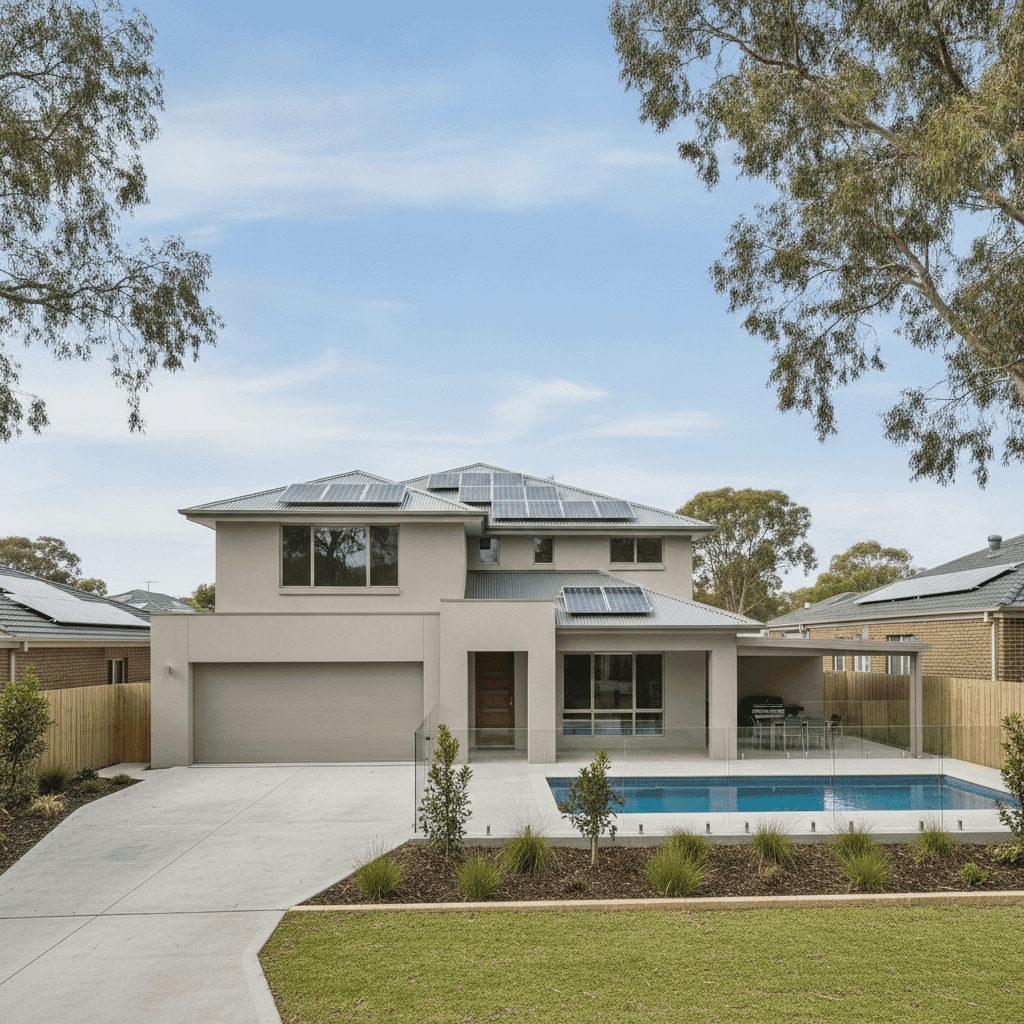

- 286 sqm building size with 5 bedrooms and 3 bathrooms: This is a substantial home, which is reflected in the $1.14 million building sum insured. Above-average fittings quality also pushes replacement costs higher — but the premium remains well-managed.

- Timber/laminate flooring: A popular and practical flooring choice that adds to the overall rebuild cost but is generally straightforward for insurers to assess.

- Swimming pool: Pools add to the insured value of the property and can introduce liability considerations, but they're a common feature in Hawkesbury homes and well understood by insurers.

- Solar panels: Rooftop solar systems add to the replacement cost of a home and should always be explicitly included in your sum insured. Most modern policies cover them, but it's worth confirming.

- Ducted climate control: A whole-home ducted system is a significant asset — both in terms of comfort and rebuild cost. It's another reason why accurately calculating your sum insured matters.

- Slightly elevated (less than 1m): A modest elevation can help with drainage and reduce flood exposure, which is particularly relevant in the Hawkesbury region.

---

Tips for Homeowners in Pitt Town

Whether you're reviewing your existing policy or shopping for a new one, here are four practical steps to make sure you're getting the best deal.

- Review your sum insured annually. Building costs in NSW have risen sharply over recent years. A home built in 2021 for a certain cost may now be significantly more expensive to rebuild. Use a building cost calculator and update your sum insured each year to avoid being underinsured — especially with above-average fittings.

- Check your flood and storm cover. The Hawkesbury region has a well-documented history of flooding. Make sure your policy explicitly covers flood events, not just storm damage. These are often separate definitions in policy documents, and the distinction matters enormously at claim time.

- Bundle home and contents for savings. This quote covers both home and contents under a single policy — a common way to reduce overall premium costs. If you currently hold separate policies, it's worth comparing a combined quote to see if bundling saves you money.

- Don't over-insure contents, but don't under-insure either. A $100,000 contents sum is modest for a five-bedroom home with above-average fittings. Do a room-by-room estimate of your belongings — furniture, appliances, clothing, electronics, and jewellery — to make sure you're adequately covered without paying for more than you need.

---

Ready to Compare?

If you're a homeowner in Pitt Town or anywhere in the Hawkesbury region, it pays to shop around. Premiums can vary dramatically between insurers for the exact same property — as the suburb data here clearly shows. Get a home insurance quote at CoverClub to see how your current policy stacks up, and make sure you're not paying more than you need to for the cover you deserve.