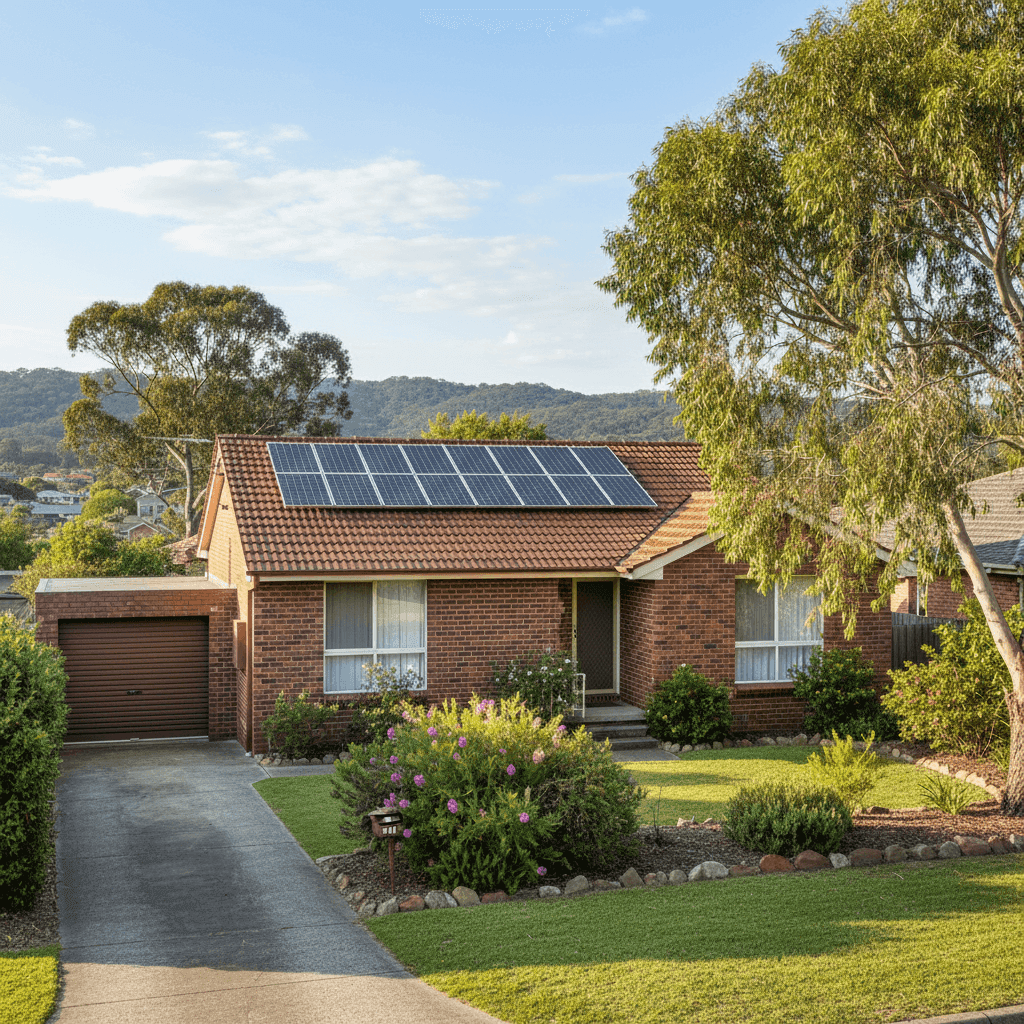

If you own a free standing home in Point Clare, NSW 2250, you're living in one of the Central Coast's most pleasant residential pockets — a quiet, leafy suburb nestled between Brisbane Water and the M1 Pacific Motorway. But pleasant surroundings don't always mean pleasant insurance bills. This article breaks down a real home and contents insurance quote for a four-bedroom brick veneer home in the area, so you can understand what's driving the price and whether there's room to save.

---

Is This Quote Fair?

The quote in question comes in at $5,016 per year (or $474/month) for combined home and contents cover, with a building sum insured of $800,000 and contents valued at $101,000. Both the building and contents excess sit at $1,000.

Our rating for this quote is Expensive — above average.

To put that in perspective, the average home and contents premium across Point Clare sits at just $2,111 per year, with a median of $1,858. This quote is more than double the local average. Even the 75th percentile for the suburb — meaning 75% of quotes come in below this figure — is only $2,349 per year.

So why is this quote so high? A few factors are likely at play. The building sum insured of $800,000 is substantial and will directly drive up the building component of the premium. The property is also 268 sqm — a generous footprint for the area — and was built in 1980, which can attract higher rebuild cost estimates and slightly elevated risk assessments from insurers. The presence of solar panels and ducted climate control also adds to the replacement value insurers need to account for.

That said, it's always worth shopping around. A quote that's expensive with one insurer may be priced very differently with another.

---

How Point Clare Compares

Understanding where Point Clare sits in the broader insurance landscape is useful context for any homeowner. You can explore the full suburb breakdown on the Point Clare insurance stats page.

| Benchmark | Premium |

|---|---|

| This quote | $5,016/yr |

| Point Clare suburb average | $2,111/yr |

| Point Clare suburb median | $1,858/yr |

| NSW state average | $9,528/yr |

| NSW state median | $3,770/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

| Hawkesbury LGA average | $10,350/yr |

A few things stand out here. While this quote looks expensive compared to the Point Clare suburb average, it's actually sitting just below the national average of $5,347/year and well below the NSW state average of $9,528/year. The Hawkesbury LGA average of $10,350/year is even higher, which speaks to the elevated flood and bushfire risk that affects many parts of regional NSW.

Point Clare itself benefits from relatively moderate risk compared to many other NSW postcodes. Its suburban location, proximity to water without significant flood plain exposure, and non-cyclone classification all contribute to a more manageable baseline risk. Compared to national benchmarks, the suburb's average premium of $2,111 is quite competitive.

The takeaway? This particular quote is on the expensive side for Point Clare, but it's not out of step with what you might expect nationally for a large, well-appointed home with a high sum insured.

---

Property Features That Affect Your Premium

Several characteristics of this property have a meaningful impact on what insurers charge. Here's how they stack up:

Brick veneer construction and tiled roof — This is generally considered a favourable combination by Australian insurers. Brick veneer offers solid fire resistance and structural durability, while tiled roofs are seen as more resilient than corrugated iron or Colorbond in many risk assessments. These features can work in your favour when it comes to pricing.

Slab foundation — Concrete slab foundations are standard across much of suburban NSW and don't typically attract a risk loading. They're considered stable and low-maintenance compared to older pier-and-beam setups.

Timber and laminate flooring — While stylish and common in homes of this era, timber flooring can be more susceptible to water damage than tiles. Insurers may factor this into contents and building assessments, particularly for water-related claims.

Construction year: 1980 — Homes built in the late 1970s and early 1980s are now over 40 years old. While brick veneer construction from this period is generally solid, insurers may apply a modest loading to account for older wiring, plumbing, and roofing materials that could be more prone to failure.

Solar panels — The presence of a solar system adds to the replacement value of the property. Insurers need to account for the cost of replacing panels and associated inverter equipment, which can run into several thousand dollars. Make sure your sum insured reflects this.

Ducted climate control — Similarly, a ducted air conditioning system is a significant fixed asset. At replacement costs of $10,000–$25,000 or more depending on the system, this is another item that can push your building sum insured — and therefore your premium — higher.

No pool, no cyclone risk zone — The absence of a pool removes a common liability and maintenance risk that some insurers price into premiums. Being outside a cyclone risk zone is also a meaningful advantage for NSW Central Coast homeowners.

---

Tips for Homeowners in Point Clare

1. Review your sum insured carefully An $800,000 building sum insured is significant. Make sure it reflects the actual cost to rebuild your home from scratch — not its market value. Over-insuring can mean unnecessarily high premiums, while under-insuring can leave you badly exposed at claim time. Tools like the Cordell Sum Sure Calculator can help you estimate rebuild costs accurately.

2. Compare multiple insurers This quote is rated expensive relative to the local market. With a suburb average of $2,111/year, there may be meaningful savings available by comparing policies. Different insurers price the same risk quite differently — get a quote through CoverClub to see what's available for your specific property.

3. Consider a higher excess to lower your premium Both the building and contents excess on this policy are set at $1,000. Increasing your excess — say to $2,500 or $5,000 — can reduce your annual premium noticeably. This strategy works well if you have a solid emergency fund and are primarily seeking cover for major, catastrophic events rather than minor claims.

4. Bundle and ask about discounts Some insurers offer discounts when you hold multiple policies (e.g., home, contents, and car) with them. It's worth asking whether a bundled arrangement could bring down the overall cost, particularly given the combined premium here is over $5,000 per year.

---

Ready to Compare?

Insurance pricing varies enormously between providers, and a quote that's expensive with one insurer could be significantly cheaper elsewhere — for the same level of cover. If you're a homeowner in Point Clare or anywhere on the NSW Central Coast, it pays to compare.

Visit CoverClub to compare home and contents insurance quotes for your property. It takes just a few minutes, and you might be surprised how much you can save.