Port Kennedy, nestled along the southern shores of the Rockingham coast in Western Australia, is a popular suburb for families seeking that relaxed coastal lifestyle without straying too far from Perth's urban conveniences. If you own a free standing home here, understanding what you should be paying for home and contents insurance — and why — can make a real difference to your household budget.

This article takes a close look at a recent insurance quote for a four-bedroom, two-bathroom free standing home in Port Kennedy (postcode 6172), breaking down whether the price is reasonable, how it compares to local and national benchmarks, and what you can do to make sure you're getting the best value.

---

Is This Quote Fair?

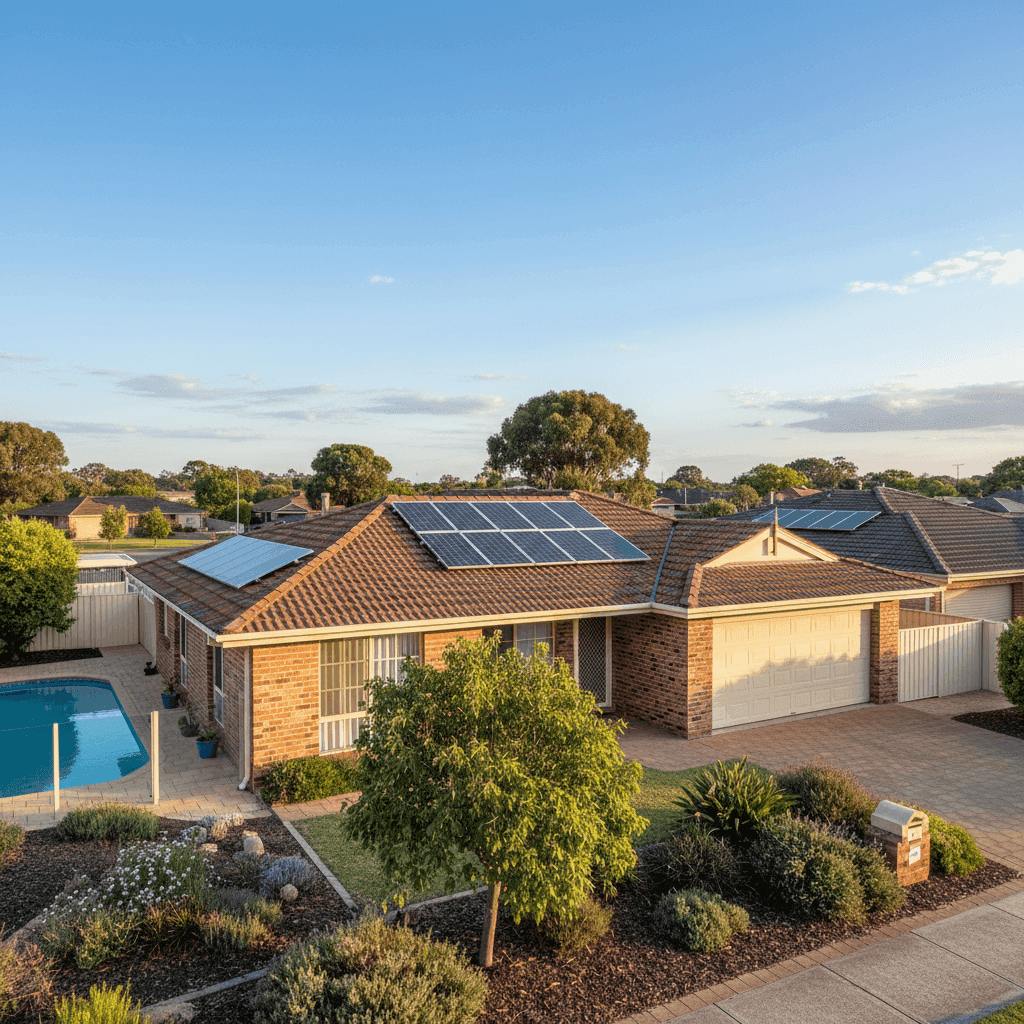

The quote in question comes in at $2,122 per year (or roughly $203 per month) for combined home and contents cover, with a building sum insured of $669,000 and contents valued at $104,000. Both the building and contents excess are set at $1,000.

Based on CoverClub's pricing data, this quote has been rated Fair — Around Average. That's a reasonable outcome, though it's worth unpacking what "average" actually means in this context.

Looking at the Port Kennedy suburb data, the suburb average premium sits at $1,616 per year, with a median of $1,364. At $2,122, this quote lands above both of those figures — but it's important to remember that averages can be skewed by lower-coverage policies. The 75th percentile for the suburb is $2,224, which means this quote sits comfortably within the upper-middle range of what Port Kennedy homeowners are paying. Given the above-average fittings, pool, solar panels, and ducted climate control included in this property's profile, a premium above the suburb median is entirely expected.

Within the Rockingham LGA, the average premium is $1,561 — again lower, but reflective of a broader mix of property types and coverage levels across the area.

---

How Port Kennedy Compares

To put this quote in proper perspective, here's how it stacks up across different geographic benchmarks:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Port Kennedy (6172) | $1,616/yr | $1,364/yr |

| Rockingham LGA | $1,561/yr | — |

| Western Australia | $2,811/yr | $2,127/yr |

| National | $5,347/yr | $2,764/yr |

At $2,122, this quote sits below both the WA state average and the national average — a genuinely positive sign. Compared to the WA state average of $2,811, this homeowner is paying around $689 less per year. Against the national average of $5,347, the savings are even more dramatic, though it's worth noting that national averages are heavily influenced by high-risk regions such as North Queensland, where cyclone and flood exposure pushes premiums significantly higher.

Port Kennedy's relatively benign risk profile — no cyclone risk zone designation, low flood exposure, and a well-established suburban environment — helps keep premiums competitive compared to many other parts of Australia.

---

Property Features That Affect Your Premium

Several characteristics of this particular property have a meaningful influence on what insurers are willing to charge.

Double brick construction is generally viewed favourably by insurers. It's durable, fire-resistant, and holds up well in storms — all factors that reduce the likelihood of a large claim. Combined with a tiled roof, which is similarly resilient and low-maintenance compared to alternatives like Colorbond or fibrous cement, this home presents a solid risk profile from an underwriting perspective.

The slab foundation is standard for WA homes of this era and doesn't introduce any particular concerns. Likewise, tiled flooring throughout is considered a durable, low-risk finish that won't be easily damaged by minor water ingress.

The above-average fittings quality is one factor that pushes the premium higher. High-end kitchens, quality bathroom fixtures, and premium finishes cost more to repair or replace — and insurers price accordingly. This is reflected in the $669,000 building sum insured, which is a substantial figure and appropriate for a well-appointed 244 sqm home.

The swimming pool adds both value and liability exposure. Pools require specific coverage considerations, including public liability for guests and visitors. The solar panel system also needs to be factored into the building sum insured, as panels can be costly to replace following storm or hail damage. And the ducted climate control system — another above-average inclusion — represents a significant replacement cost if it were to be damaged or destroyed.

Built in 1995, this home is at an age where some building components (roofing, plumbing, electrical) may be approaching the end of their serviceable life, which can subtly influence risk assessments by some insurers.

---

Tips for Homeowners in Port Kennedy

1. Review your building sum insured regularly Construction costs have risen sharply in recent years across WA. A sum insured of $669,000 may be appropriate today, but it's worth getting a professional building replacement cost estimate every few years to ensure you're not underinsured. CoverClub's quoting tool can help you explore updated estimates.

2. Check your solar panel and pool coverage explicitly Not all standard home insurance policies automatically cover solar panels or pools to the same extent. Read your Product Disclosure Statement carefully to confirm these are included in your building cover — and at what limit.

3. Consider your excess level strategically Both excesses are set at $1,000, which is fairly standard. Opting for a higher voluntary excess (say, $1,500 or $2,000) can reduce your annual premium meaningfully. If you rarely make small claims, this trade-off can save you money over the long run.

4. Compare quotes at renewal time Insurance loyalty doesn't always pay off. Insurers frequently offer better rates to new customers, and the market can shift significantly from year to year. Even if your current quote is rated "Fair," running a comparison at renewal could reveal a materially cheaper option with equivalent or better coverage.

---

Ready to Compare?

Whether you're reviewing your current policy or shopping for cover on a new property, CoverClub makes it easy to compare home and contents insurance quotes across Australia's leading insurers. Get a personalised quote today and see how much you could save — without compromising on the cover that matters most.