Port Macquarie is one of the Mid North Coast's most sought-after places to call home — and with a brand-new four-bedroom, two-bathroom free standing home, it's easy to see the appeal. But alongside the lifestyle comes the practicality of protecting your investment. This article breaks down a recent home and contents insurance quote for a property in Port Macquarie (NSW 2444), rated Expensive (Above Average), and puts the numbers in context so you can make a more informed decision.

---

Is This Quote Fair?

The quote in question comes in at $5,393 per year (or $517 per month) for a building sum insured of $856,000 and $150,000 in contents cover, each with a $1,000 excess.

Our price rating for this quote is Expensive — Above Average, and the data backs that up. According to quotes collected for Port Macquarie (2444), the suburb median premium sits at $2,646/yr, meaning this quote is more than double what half of comparable properties in the area are paying. Even the 75th percentile — the upper end of the typical range — lands at $3,876/yr, still well below this quote's $5,393.

That said, context matters. This is a newly constructed home (2026 build) with above-average fittings, a pool, solar panels, and a substantial building sum insured of $856,000 — all factors that push premiums higher. The quote isn't necessarily unreasonable for what's being covered, but it does suggest there's room to shop around.

---

How Port Macquarie Compares

To understand where this quote sits in the broader landscape, here's a snapshot of average premiums across different geographies:

| Geography | Average Premium | Median Premium |

|---|---|---|

| Port Macquarie (2444) | $8,890/yr | $2,646/yr |

| Port Macquarie-Hastings LGA | $7,001/yr | — |

| New South Wales | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. The suburb and state averages are significantly higher than their medians, which tells us that a relatively small number of very high-premium properties are pulling the averages upward — likely larger homes, higher-risk locations, or those with more extensive cover. The median is generally a more reliable benchmark for the "typical" homeowner.

Interestingly, this quote of $5,393/yr sits above the national average of $5,347/yr and comfortably above the NSW state median of $3,770/yr. Compared to the national median of $2,764/yr, it's nearly double — though again, the level of cover and property features here are above average.

Port Macquarie-Hastings LGA average of $7,001/yr suggests that the broader region does carry elevated premiums relative to the national median, so some of this cost is simply the reality of insuring property on the Mid North Coast.

---

Property Features That Affect Your Premium

Several characteristics of this property are likely contributing to a higher-than-median premium:

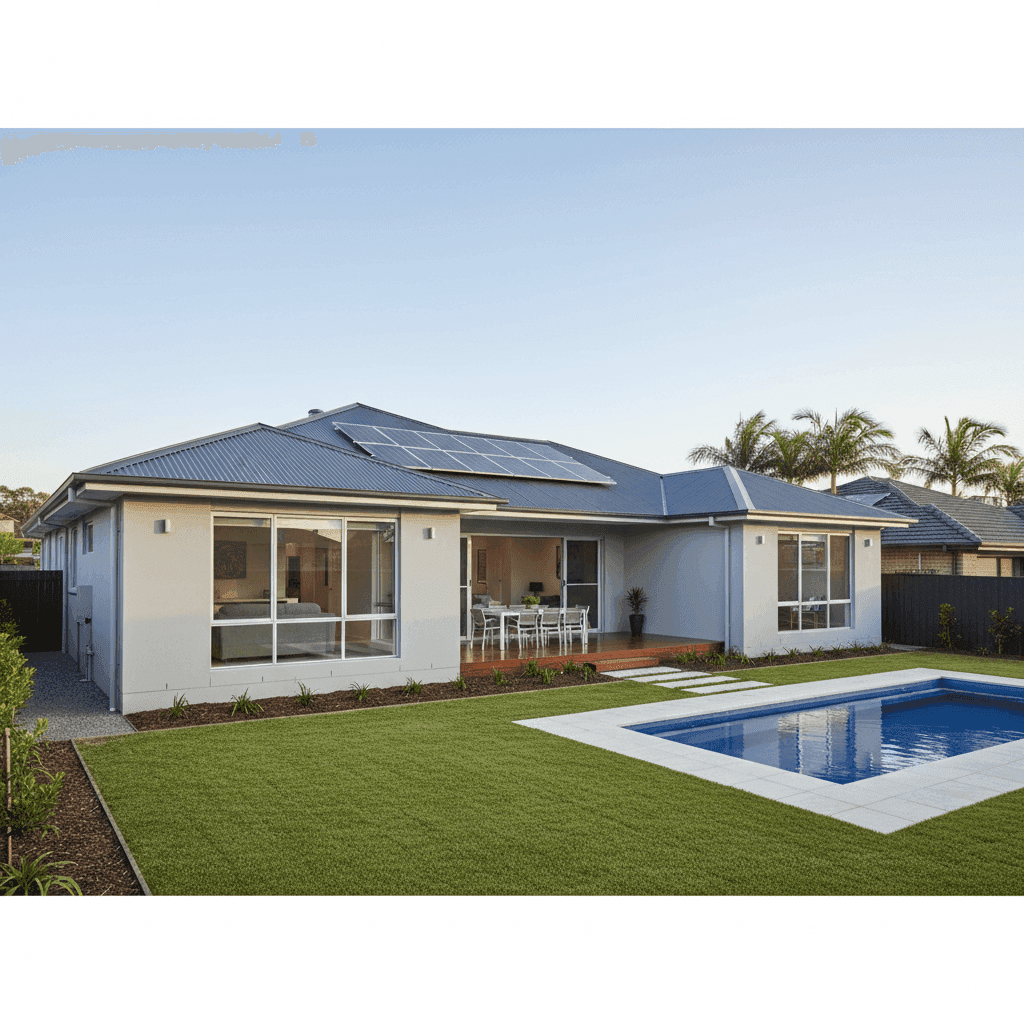

New Build (2026) Brand-new homes typically attract higher replacement costs, and a building sum insured of $856,000 for a 214 sqm home reflects above-average construction quality. Insurers price based on what it would cost to rebuild — not the market value — so a premium finish means a premium sum insured.

Above-Average Fittings Above-average fittings — think stone benchtops, quality cabinetry, premium fixtures — increase the cost to rebuild or repair. This is one of the most direct drivers of a higher building sum insured and, by extension, a higher premium.

Swimming Pool A pool adds both value and liability to a property. From an insurance perspective, it increases the cost of full reinstatement and may also attract additional liability considerations, nudging the premium upward.

Solar Panels Solar systems are now a standard feature on many Australian homes, but they do add to the replacement cost of the building. A rooftop solar installation can cost anywhere from $5,000 to $15,000+ to replace, which feeds into the building sum insured calculation.

Steel/Colorbond Roof On the positive side, a Colorbond steel roof is generally regarded favourably by insurers. It's durable, fire-resistant, and performs well in storms — all of which can help moderate premiums compared to tile or older roofing materials.

Slab Foundation & Timber/Laminate Flooring A concrete slab foundation is structurally sound and typically well-regarded by insurers. Timber and laminate flooring, while stylish, can be more costly to replace than tiles if water damage occurs — a factor worth keeping in mind.

---

Tips for Homeowners in Port Macquarie

1. Compare multiple quotes — every year Insurance premiums can vary dramatically between providers for the same property. With this quote rated as expensive relative to the suburb median, it's well worth running a comparison. Get a fresh quote at CoverClub to see what other insurers are offering for your specific property.

2. Review your sum insured carefully Overinsuring is a real cost — but so is underinsuring. Use a building cost calculator to verify that $856,000 accurately reflects the rebuild cost (not the market value) of your home. If your sum insured is higher than necessary, you may be paying more than you need to.

3. Consider a higher excess to reduce your premium Both the building and contents excess on this policy are set at $1,000. Opting for a higher voluntary excess — say $2,000 or $2,500 — can meaningfully reduce your annual premium. Just make sure you're comfortable covering that amount out of pocket in the event of a claim.

4. Bundle your building and contents cover This quote already combines home and contents insurance, which is a smart move. Many insurers offer a discount for bundling, and managing a single policy is simpler come renewal time. If you're not already bundled, it's worth exploring.

---

Start Comparing Today

Whether you're a new homeowner in Port Macquarie or approaching renewal on an existing policy, the best way to know if you're getting a fair deal is to compare. CoverClub aggregates real quote data from across Australia, so you can see exactly how your premium stacks up against your neighbours — and find a better deal if one exists.

Compare home insurance quotes for your Port Macquarie property →