Port Macquarie is one of the Mid North Coast's most sought-after places to live — and for good reason. With its coastal lifestyle, growing infrastructure, and mix of established and newer housing stock, it attracts families and sea-changers alike. But owning property here comes with real insurance considerations, and understanding what you're paying — and why — can make a meaningful difference to your budget. This article breaks down a recent home and contents insurance quote for a four-bedroom, three-bathroom free-standing home in Port Macquarie (postcode 2444), comparing it against local, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question comes in at $4,894 per year (or $469/month) for a combined home and contents policy, covering a building sum insured of $965,000 and contents valued at $84,000, each with a $1,000 excess.

Our price rating for this quote is Expensive (Above Average).

To put that in context: the median home insurance premium across Port Macquarie (postcode 2444) sits at $2,646 per year, based on 219 quotes collected in our dataset. At $4,894, this quote is roughly 85% above the suburb median — a significant gap that's worth unpacking.

That said, "expensive" doesn't automatically mean "wrong." A higher-than-median premium can be entirely justified by specific property characteristics — and as we'll explore below, this particular home has several features that insurers tend to price accordingly. The key question is whether the premium reflects genuine risk factors or whether there's room to find a better deal with a different provider.

---

How Port Macquarie Compares

To understand where this quote sits in the broader landscape, it helps to look at the numbers across different geographic levels. You can explore the full data on our Port Macquarie suburb stats page, the NSW state overview, and national insurance statistics.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Port Macquarie (2444) | $8,890/yr | $2,646/yr |

| Port Macquarie-Hastings LGA | $7,001/yr | — |

| NSW | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. First, the suburb average of $8,890 is dramatically higher than the median of $2,646 — a classic sign of a skewed distribution, where a subset of high-risk or high-value properties pulls the average up significantly. This means the median is a more reliable "typical" benchmark for most homeowners.

Second, at $4,894, this quote sits above the suburb median and the national median, but well below the suburb average, the LGA average, and the NSW average. It's also below the national average of $5,347. In that sense, while it's rated expensive relative to the typical Port Macquarie property, it's not out of line for a larger, well-appointed home with a higher sum insured.

The suburb's 75th percentile premium is $3,876 — meaning roughly a quarter of quotes in Port Macquarie come in above that figure. At $4,894, this quote falls in the upper range, but it's not an outlier by any means for a property of this size and specification.

---

Property Features That Affect Your Premium

Several characteristics of this home are likely contributing to the above-average premium. Here's how insurers typically view each one:

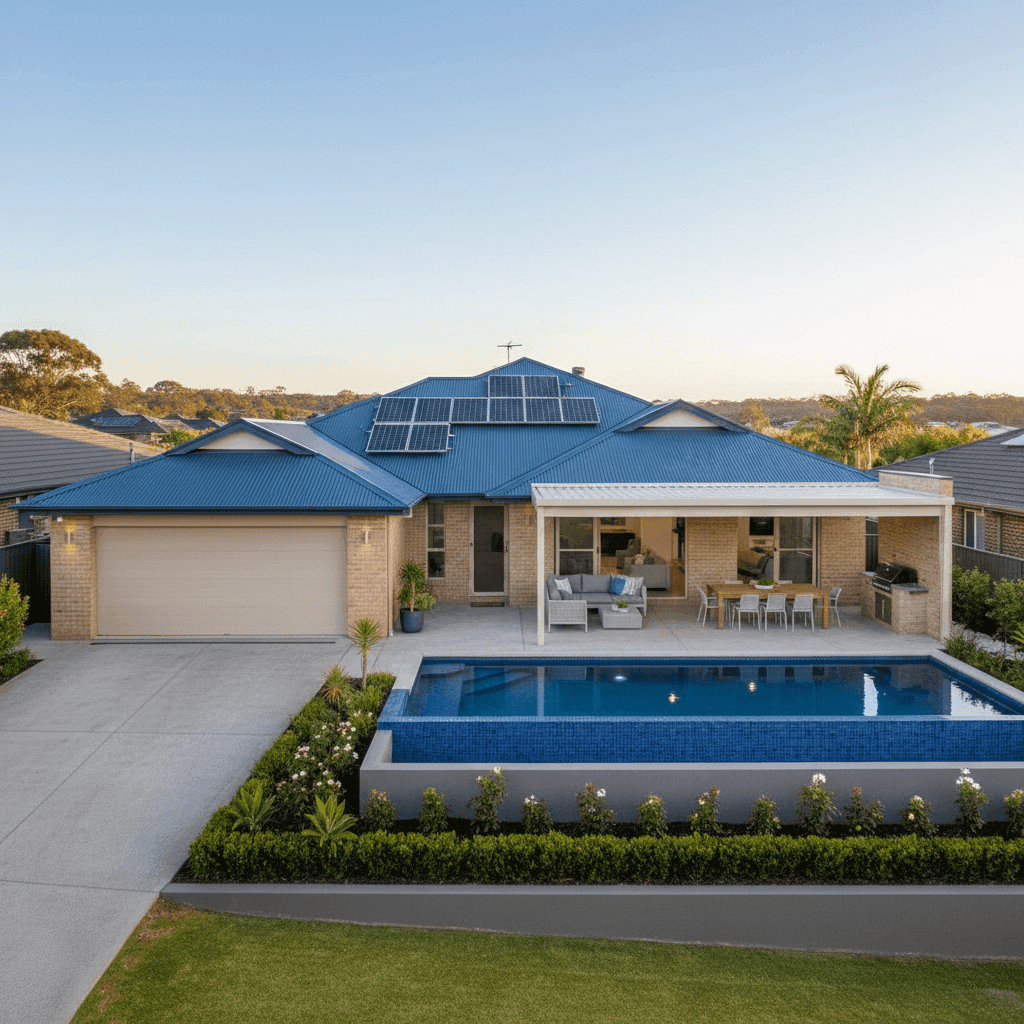

Building size and sum insured: At 315 sqm and a building sum insured of $965,000, this is a substantial home. Rebuild costs scale with size, and insurers price accordingly. A higher sum insured directly increases the premium.

Double brick construction: Generally viewed favourably by insurers due to its durability and resistance to fire and storm damage. Double brick can sometimes attract a modest discount compared to lightweight construction types.

Steel/Colorbond roof: Colorbond is widely regarded as one of the more resilient roofing materials in Australia — resistant to corrosion, fire, and high winds. This is typically a neutral-to-positive factor for pricing.

Elevated foundation (at least 1 metre): This is a notable risk mitigator in flood-prone or low-lying areas. Elevation reduces the likelihood of inundation damage to the structure, which can positively influence flood-related components of the premium.

Slab foundation: Concrete slab is a standard, low-maintenance foundation type that insurers are comfortable with in most Australian conditions.

Swimming pool: Pools add to the replacement cost of the property and can introduce liability considerations, contributing modestly to a higher premium.

Solar panels: Rooftop solar systems are insured as part of the building in most policies. With a growing number of panels on Australian homes, insurers factor in replacement costs — which can be significant — when setting the building sum insured and premium.

Ducted climate control: Ducted systems are expensive to replace and are typically included in the building sum insured, adding to the overall rebuild cost estimate.

No cyclone risk: Port Macquarie is not classified as a cyclone risk area, which removes one of the more significant premium loading factors seen in northern Queensland and parts of WA. This likely keeps the premium lower than it might otherwise be for a coastal property.

---

Tips for Homeowners in Port Macquarie

1. Review your sum insured carefully A building sum insured of $965,000 for a 315 sqm home works out to roughly $3,063 per sqm — which is at the higher end but not unreasonable for a well-finished double brick home with a pool, solar, and ducted air conditioning. Make sure your sum insured reflects current rebuild costs (not market value), and consider using an online building calculator to verify the figure annually.

2. Shop around — seriously The wide spread between Port Macquarie's 25th percentile ($1,773/yr) and average ($8,890/yr) tells you that insurers price this suburb very differently. What one insurer considers high-risk, another may view more favourably. Comparing multiple quotes is one of the most effective ways to reduce your premium without reducing your cover.

3. Consider a higher excess to reduce your premium Both the building and contents excess on this policy sit at $1,000. Increasing your excess — say, to $2,000 or $2,500 — can meaningfully reduce your annual premium. Just make sure you're comfortable covering that amount out of pocket in the event of a claim.

4. Check your contents sum insured $84,000 in contents cover is relatively modest for a four-bedroom, three-bathroom home with what appears to be quality fittings and furnishings. Underinsurance is a common problem in Australia — take the time to tally up your actual belongings to ensure you're not left short after a major event.

---

Compare Your Options with CoverClub

Whether you're renewing your policy or shopping for the first time, it pays to see what else is out there. CoverClub makes it easy to compare home and contents insurance quotes across multiple providers in minutes. Get a quote today and find out if you could be paying less — or getting more — for your Port Macquarie home.