Port Macquarie is one of the Mid North Coast's most sought-after places to call home — a relaxed coastal town with a strong sense of community and a property market that continues to attract both owner-occupiers and investors. If you own a free standing home in the 2444 postcode, understanding what you should be paying for building insurance is an important part of protecting your most valuable asset. This article breaks down a recent building-only insurance quote for a 2-bedroom, 1-bathroom free standing home in Port Macquarie and puts the numbers into context against suburb, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question sits at $2,845 per year (or $273 per month) for building-only cover with a $1,000 excess and a sum insured of $403,000. Our analysis rates this as FAIR — Around Average.

To understand what "fair" means in practice, it helps to look at where this premium sits within the local distribution of quotes. Based on 219 quotes collected for the Port Macquarie 2444 area:

- 25th percentile: $1,773/yr

- Median: $2,646/yr

- 75th percentile: $3,876/yr

At $2,845, this quote lands just above the suburb median and comfortably within the interquartile range — meaning it's broadly in line with what most Port Macquarie homeowners are paying. It's not the sharpest price available, but it's far from the most expensive either. About half of comparable properties in the area are quoted below $2,646, so there is some room to explore whether a lower premium is achievable without sacrificing coverage quality.

It's also worth noting just how wide the spread is in this suburb. The suburb average premium is a striking $8,890 per year — dramatically higher than the median. This kind of gap between mean and median is a strong signal that a relatively small number of very high-risk or high-value properties are pulling the average upward. For a typical homeowner, the median is a more meaningful yardstick.

---

How Port Macquarie Compares

Zooming out from the suburb level paints an interesting picture. Here's how the Port Macquarie 2444 median stacks up against broader benchmarks:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Port Macquarie 2444 | $8,890/yr | $2,646/yr |

| Port Macquarie-Hastings LGA | $7,001/yr | — |

| NSW State | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. The NSW state median of $3,770/yr is noticeably higher than Port Macquarie's local median of $2,646 — suggesting that, on the whole, homeowners in this part of the Mid North Coast are paying less than many of their counterparts elsewhere in the state. This likely reflects the fact that Port Macquarie sits outside designated cyclone risk zones and has relatively manageable flood and bushfire exposure compared to parts of regional and western NSW.

At the national level, the median of $2,764/yr is close to Port Macquarie's local figure, reinforcing that this is a reasonably typical market when it comes to building insurance costs. The national average of $5,347/yr, like the suburb average, is skewed upward by high-risk and high-value properties across the country — particularly in cyclone-prone Queensland and flood-affected regions.

---

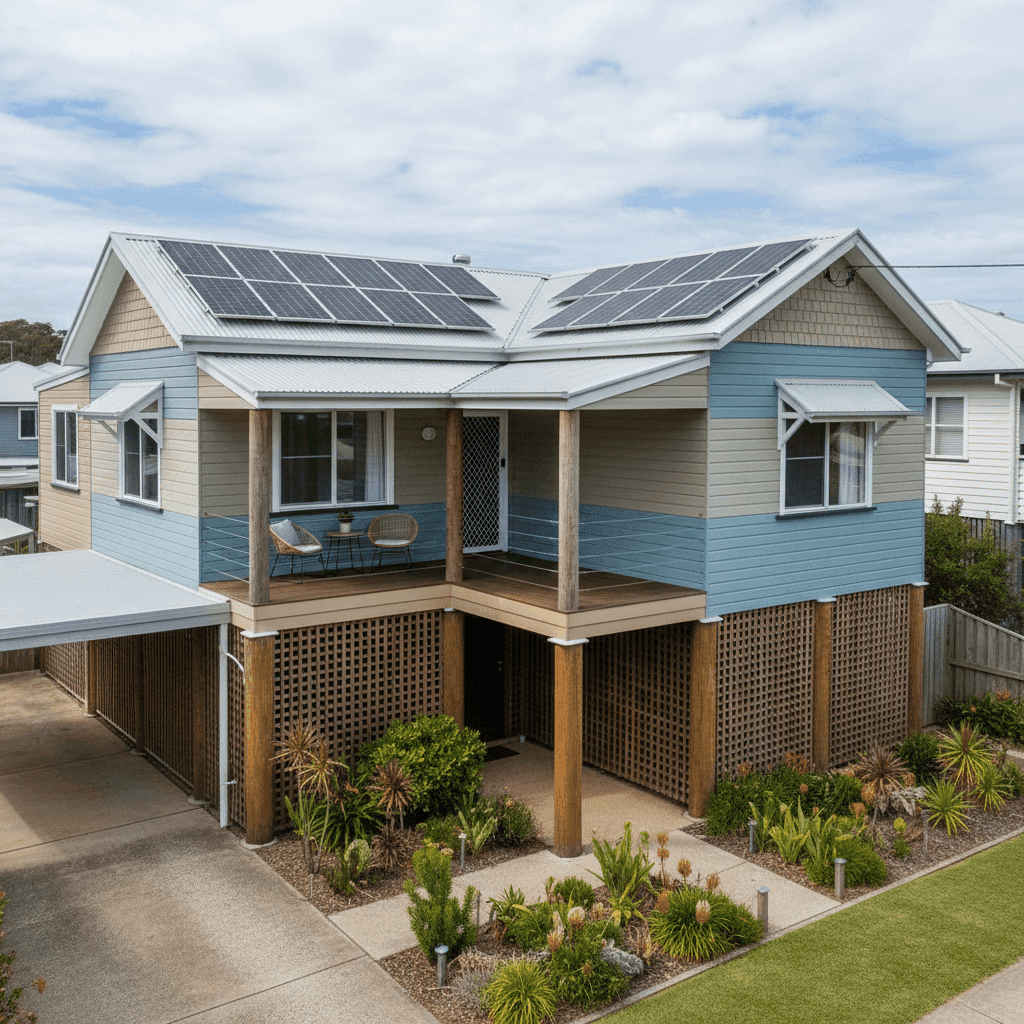

Property Features That Affect Your Premium

Several characteristics of this particular property are worth examining through an insurance lens.

Hardiplank/Hardiflex external walls are a popular choice in coastal and subtropical climates. As a fibre cement product, Hardiflex is generally viewed favourably by insurers — it's resistant to rot, termites, and moisture, and holds up well in coastal conditions. This may contribute to a more competitive premium compared to older weatherboard or brick veneer constructions.

Steel/Colorbond roofing is another positive factor. Colorbond is durable, lightweight, and performs well in high-wind events. Insurers typically regard it as lower risk than older tile roofs, which can crack, lift, or allow water ingress more readily.

Elevated foundations (stumps, at least 1 metre) are a double-edged sword. On one hand, elevation provides meaningful protection against inundation in flood or storm surge events — a real consideration in coastal NSW. On the other, elevated homes can be more vulnerable to wind damage and may cost more to repair or rebuild due to the complexity of the subfloor structure. The $403,000 sum insured should account for this.

Solar panels add replacement value to the building and can slightly increase premiums, as they represent an additional asset that needs to be covered. It's worth confirming with your insurer that your solar system is explicitly included in your building cover.

Ducted climate control similarly adds to the replacement cost of the home. Systems of this type can be expensive to repair or replace, and their inclusion in the sum insured calculation is important to get right.

Timber and laminate flooring can be more susceptible to water damage than tile alternatives, which is worth bearing in mind given the coastal location and elevated foundation style.

---

Tips for Homeowners in Port Macquarie

1. Review your sum insured regularly. Construction costs have risen significantly in recent years, and a sum insured set even two or three years ago may no longer reflect the true cost of rebuilding your home. At $403,000 for a 105 sqm home, this figure equates to roughly $3,838 per sqm — which is broadly reasonable for 2025 build costs in regional NSW, but worth validating with a quantity surveyor or an online rebuild cost calculator.

2. Confirm solar panels and ducted systems are covered. Not all building policies automatically cover solar panel arrays or ducted air conditioning as part of the standard building definition. Check your Product Disclosure Statement (PDS) carefully, and contact your insurer if you're unsure.

3. Shop around — even if your current quote seems fair. A "fair" rating means this premium is around average, not that it's the best available. Premiums for the same property can vary significantly between insurers based on their individual risk models. Comparing multiple quotes takes only a few minutes and could save you hundreds of dollars a year.

4. Consider the excess trade-off. This policy carries a $1,000 building excess. Opting for a higher excess — say, $2,000 — can meaningfully reduce your annual premium. If your property is well-maintained and you're unlikely to make small claims, a higher excess can be a smart financial decision.

---

Compare Your Home Insurance Today

Whether you're a first-time buyer or a long-term Port Macquarie local, it pays to make sure your building insurance is working as hard as you are. CoverClub makes it easy to compare quotes from multiple insurers in minutes — so you can see exactly where your premium sits and whether a better deal is available. Get a quote now at CoverClub and take the guesswork out of home insurance.