Port Noarlunga is a coastal suburb sitting about 35 kilometres south of Adelaide's CBD, known for its scenic estuary, surf beach, and a mix of older character homes alongside more recent builds. For owners of a free-standing home in this part of South Australia, understanding what drives your building insurance premium — and whether the number on your quote is genuinely competitive — can make a real difference to your household budget.

This article breaks down a recent building-only insurance quote for a four-bedroom, one-bathroom free-standing home in Port Noarlunga (postcode 5167), and puts that figure into context using suburb, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question comes in at $1,582 per year (or $152 per month) for building-only cover, with a $1,000 building excess and a sum insured of $643,000.

Our price rating for this quote is Expensive — Above Average.

To understand why, it helps to look at what other homeowners in the same suburb are paying. Based on Port Noarlunga insurance data on CoverClub, the suburb average sits at $1,268 per year, with a median of $1,286. The 25th percentile — meaning a quarter of quotes come in below this figure — is $1,051, while the 75th percentile is $1,480.

At $1,582, this quote lands above the 75th percentile for the suburb. That means roughly three out of four comparable quotes in Port Noarlunga are cheaper. It's not wildly out of range, but it does suggest there's meaningful room to shop around.

That said, context matters. The sum insured here is $643,000, which may be higher than what some neighbours have nominated — and a higher rebuild cost naturally pushes the premium up. Still, the "above average" rating is a useful signal that it's worth comparing alternatives before renewing or accepting this figure.

---

How Port Noarlunga Compares

One of the most reassuring things about insuring a home in Port Noarlunga is how the suburb stacks up against broader benchmarks.

| Benchmark | Annual Premium |

|---|---|

| This quote | $1,582 |

| Suburb average | $1,268 |

| Suburb median | $1,286 |

| LGA (Onkaparinga) average | $1,431 |

| SA state average | $2,433 |

| SA state median | $1,679 |

| National average | $5,347 |

| National median | $2,764 |

Even at $1,582 — which is above average for the suburb — this quote is still well below the South Australian state average of $2,433 and dramatically cheaper than the national average of $5,347. Much of that national figure is skewed by high-risk areas in Queensland and Western Australia, where cyclones, floods, and bushfires push premiums into the thousands.

Port Noarlunga benefits from a relatively benign risk profile compared to many parts of the country. It's not in a designated cyclone risk zone, and while bushfire risk exists in parts of the Onkaparinga region, coastal suburbs like Port Noarlunga tend to attract more moderate premiums than their Hills counterparts.

The LGA average for Onkaparinga sits at $1,431 — meaning this quote is about $150 above what's typical across the broader council area. Again, not alarming, but worth noting.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on what insurers charge.

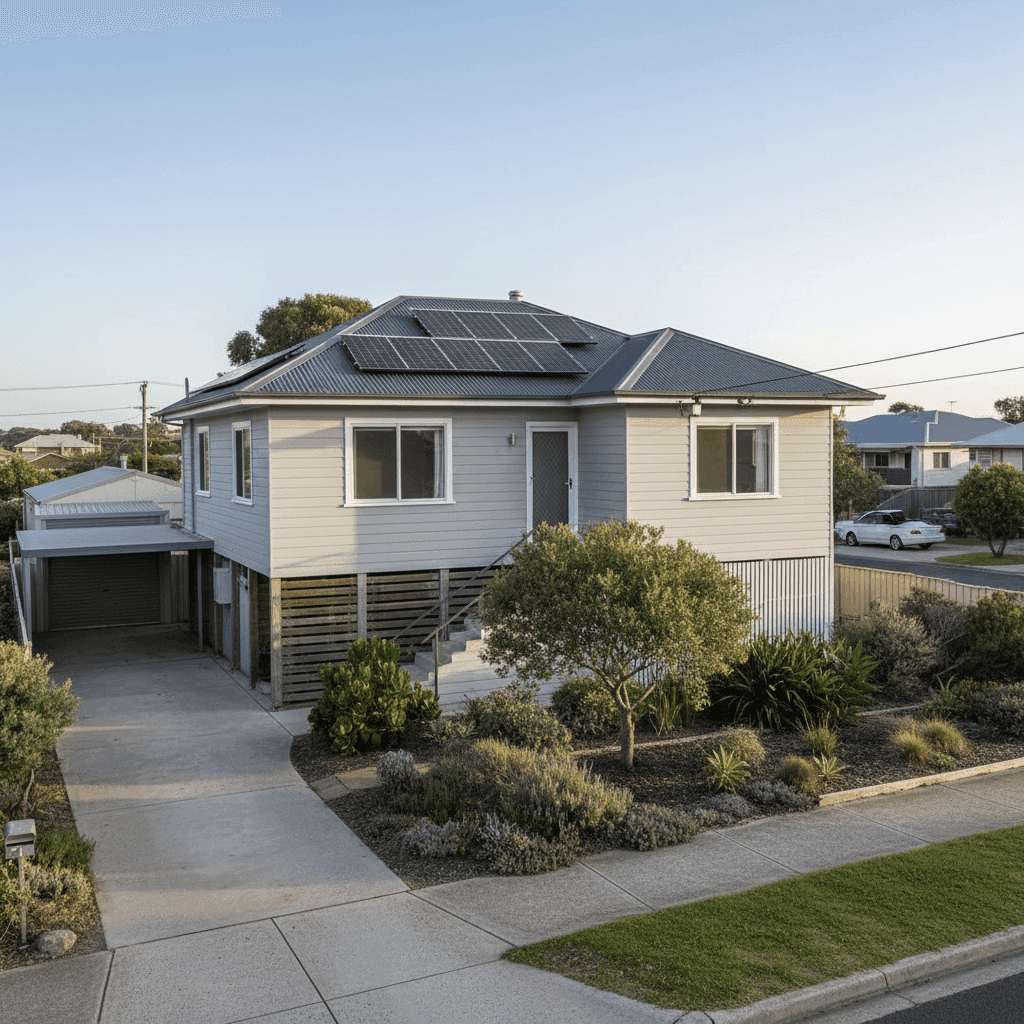

Hardiplank/Hardiflex cladding is a fibre cement product that's common in homes of this era and is generally viewed favourably by insurers. It's non-combustible, resistant to termites, and holds up well in coastal environments — all positives when it comes to risk assessment.

Steel/Colorbond roofing is another tick in the right column. Colorbond is durable, low-maintenance, and performs well in fire-prone conditions. Insurers typically price metal roofs more competitively than older tile or asbestos roofing, which can be costly to replace.

Stump foundations are characteristic of homes built in the mid-20th century across South Australia. While stumps can be a flag for subsidence or settlement risk — particularly in clay-heavy soils — they're well understood by local insurers and don't automatically attract a loading. That said, the condition of the stumps matters, and any signs of movement or deterioration should be addressed.

Solar panels add value to the property but also add complexity to a claim. Most building policies cover rooftop solar as part of the structure, but it's worth confirming this with your insurer and ensuring the sum insured reflects the panels' replacement cost.

Ducted climate control is another feature that increases the overall rebuild cost and contributes to the sum insured. Systems like these can be expensive to replace, and it's important they're factored into your building sum insured rather than left out and underinsured.

The home was built in 1960, which means it's over 60 years old. Older homes can carry higher premiums due to the cost of sourcing period-appropriate materials and the potential for electrical or plumbing systems to be ageing. Keeping these systems updated can help manage risk — and potentially your premium.

---

Tips for Homeowners in Port Noarlunga

1. Review your sum insured carefully At $643,000 for a 130 sqm home, the sum insured works out to roughly $4,946 per square metre. That's on the higher end, though it may reflect the ducted climate control, solar panels, and the cost of rebuilding an older home with appropriate materials. Use a building cost calculator to sense-check this figure — being overinsured costs you in premiums, while being underinsured can be devastating at claim time.

2. Shop around at renewal This quote sits above the 75th percentile for the suburb, which is a strong signal to compare alternatives. Insurers price risk differently, and a policy that's expensive with one provider may be competitively priced with another. Use CoverClub to compare quotes before your renewal date rather than auto-renewing.

3. Consider your excess A $1,000 building excess is fairly standard, but opting for a higher voluntary excess can reduce your annual premium. If you're a careful homeowner unlikely to make small claims, a higher excess can be a cost-effective trade-off.

4. Keep maintenance records For a home built in 1960, demonstrating that you've kept up with maintenance — stumps, roof, gutters, electrical — can support your position in the event of a claim and may help you access better rates over time. Some insurers offer loyalty or claims-free discounts that reward well-maintained properties.

---

Compare Your Options with CoverClub

Whether you're reviewing an existing policy or shopping for the first time, it pays to see what the market looks like before you commit. CoverClub makes it easy to compare home insurance quotes for properties across Port Noarlunga and the wider Onkaparinga area. Get a quote today and find out if you could be paying less for the same level of cover.