Portarlington is a relaxed coastal town on the Bellarine Peninsula, popular with families and sea-changers drawn to its beaches, ferry access to Melbourne, and a strong sense of community. For owners of a four-bedroom, free-standing home in this pocket of Victoria, understanding what you should be paying for home and contents insurance — and why — can make a real difference to your budget.

This article breaks down a recent home and contents insurance quote for a property in Portarlington (postcode 3223), benchmarks it against local, state, and national data, and offers practical tips for getting the best value on your cover.

---

Is This Quote Fair?

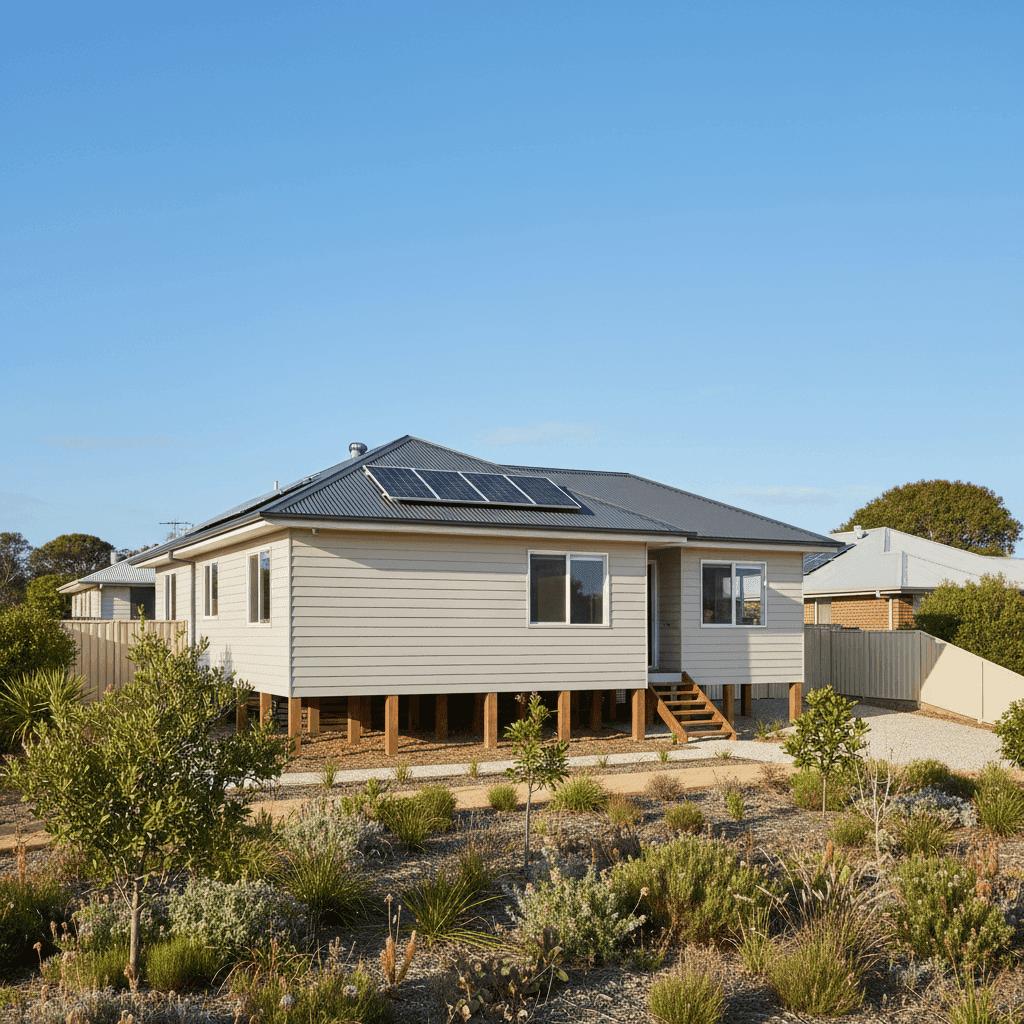

The quote in question came in at $3,262 per year (or $313 per month) for a four-bedroom, three-bathroom free-standing home, with a building sum insured of $1,100,000 and contents cover of $235,000. Both the building and contents excesses are set at $2,000.

Our price rating for this quote is FAIR — Around Average, which is a reasonable outcome for a property of this size and specification. It's not the sharpest price on the market, but it's well within the normal range for comparable homes in the area.

The $1,100,000 building sum insured is notable — this is the amount it would cost to fully rebuild the home, not its market value. For a 214 sqm home with above-average fittings, a timber floor, ducted climate control, and solar panels, a rebuild figure in this range is entirely plausible, particularly given the rising cost of construction materials and labour across regional Victoria.

---

How Portarlington Compares

To put this quote in context, here's how it stacks up against the benchmarks we track at CoverClub:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $3,262 |

| Portarlington suburb average | $2,794 |

| Portarlington suburb median | $2,791 |

| Portarlington 25th percentile | $1,992 |

| Portarlington 75th percentile | $3,348 |

| VIC state average | $3,000 |

| VIC state median | $2,718 |

| National average | $5,347 |

| National median | $2,764 |

| Greater Geelong LGA average | $1,754 |

A few things stand out here. First, this quote sits above the Portarlington suburb average of $2,794, but comfortably within the 75th percentile of $3,348 — meaning roughly three quarters of quotes in the suburb come in cheaper, and about a quarter are in this range or higher. That's consistent with a "Fair / Around Average" rating.

Compared to the VIC state average of $3,000, this quote is modestly higher, which makes sense given the larger-than-average home size and higher sum insured. Against the national average of $5,347, it looks quite competitive — a reminder that many parts of Australia, particularly in Queensland and Northern Australia, face significantly elevated premiums due to cyclone, flood, and storm risk.

The Greater Geelong LGA average of $1,754 is notably lower than the Portarlington suburb average, suggesting that Portarlington carries slightly more risk or attracts higher-value properties than the broader LGA. You can explore the full Portarlington suburb insurance data here.

---

Property Features That Affect Your Premium

Several characteristics of this property directly influence what insurers charge. Understanding these can help you make sense of your quote — and potentially reduce it.

Weatherboard Timber Walls

Weatherboard construction is common in coastal Victoria and has a certain charm, but insurers typically view it as a higher risk than brick veneer or double brick. Timber is more susceptible to fire and, over time, to moisture damage and rot. This can push premiums up compared to masonry-walled homes of similar size.

Steel / Colorbond Roof

Good news here — a Colorbond steel roof is generally well-regarded by insurers. It's durable, fire-resistant, and performs well in high-wind conditions. This is likely a neutral-to-positive factor in the premium calculation.

Stump Foundation

Homes on stumps (also called pier or post foundations) are common in older coastal areas and can be a factor in premium pricing. Stumps can be vulnerable to subsidence, pest damage, and storm impact, so some insurers apply a modest loading for this construction type.

Timber and Laminate Flooring

Timber floors add to the rebuild cost and can be expensive to replace if damaged by water or fire. With above-average fittings throughout, the overall replacement cost of the home's interior is higher than a standard build, which is reflected in the $235,000 contents value and the premium.

Solar Panels

Solar panels add value to a property but also add to the insured rebuild cost. Importantly, most home insurance policies cover rooftop solar as part of the building sum insured — it's worth confirming this with your insurer to avoid being underinsured.

Ducted Climate Control

Ducted heating and cooling systems are expensive to repair or replace, and their inclusion pushes up the overall cost to rebuild. This is another reason why a higher building sum insured — and a slightly higher premium — is justified for this property.

---

Tips for Homeowners in Portarlington

1. Review Your Building Sum Insured Annually

Construction costs in regional Victoria have risen significantly in recent years. If your sum insured hasn't kept pace, you could face a significant shortfall in the event of a total loss. Use a building cost calculator or speak to a quantity surveyor to make sure your cover reflects today's rebuild costs.

2. Consider Your Excess Level

This quote carries a $2,000 excess on both building and contents. Opting for a higher excess — say $2,500 or $5,000 — can meaningfully reduce your annual premium. Just make sure you're comfortable covering that amount out of pocket in the event of a claim.

3. Maintain Your Weatherboard Exterior

Insurers can reduce or deny claims if damage is linked to a lack of maintenance. Keeping your weatherboard cladding painted, sealed, and free from rot not only protects the home but also keeps you on the right side of your policy's maintenance obligations.

4. Shop Around at Renewal Time

A "Fair" rating means there may be room to improve. The spread between the 25th percentile ($1,992) and 75th percentile ($3,348) in Portarlington is wide, suggesting different insurers price this suburb quite differently. Comparing quotes at renewal — rather than simply accepting an automatic rollover — could save you hundreds of dollars a year.

---

Compare Your Home Insurance Options

Whether you're reviewing an existing policy or shopping for cover on a new home, comparing quotes is the single most effective way to make sure you're not overpaying. CoverClub makes it easy to benchmark your premium against real data from your suburb and state.

Get a home insurance quote today and see how your current cover stacks up.