Pottsville is a laid-back coastal town tucked into the far north of New South Wales, just south of the Queensland border. It's the kind of place where demand for quality housing has grown steadily — and so has the importance of making sure your home is properly protected. If you own a free-standing home in Pottsville, understanding what you should expect to pay for home and contents insurance is a smart first step toward getting genuine value from your policy.

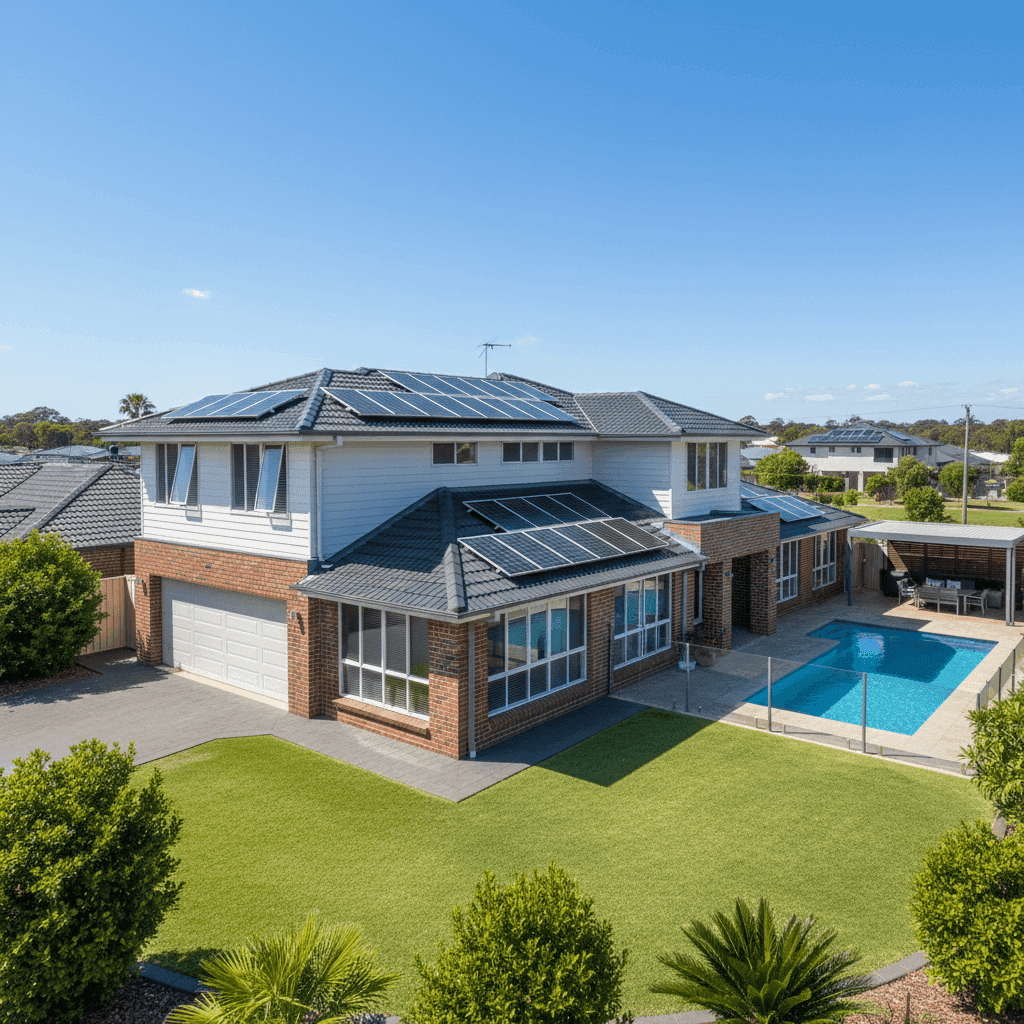

This article breaks down a real insurance quote for a 4-bedroom, 2-bathroom brick veneer home in Pottsville (postcode 2489), built in 2017, with a building sum insured of $707,000 and contents cover of $100,000. The annual premium came in at $3,461 (or roughly $339/month). Here's what that figure actually means in context.

---

Is This Quote Fair?

The short answer: yes, broadly speaking. CoverClub's pricing analysis rates this quote as Fair — Around Average, which means it sits within a reasonable range when benchmarked against comparable properties in the area.

At $3,461 per year, this premium lands above the Pottsville suburb average of $2,924/yr and the suburb median of $2,953/yr — but it's well within the suburb's interquartile range (25th percentile: $1,491/yr; 75th percentile: $4,066/yr). In other words, 50% of quotes sampled in Pottsville fall between roughly $1,491 and $4,066, so this premium is comfortably inside that band.

It's also worth noting that this quote is actually below the NSW state average of $3,801/yr, which is a meaningful positive signal. Homeowners in New South Wales tend to pay more than the national average, so coming in under the state benchmark is a reasonable outcome for a well-built, modern home.

The $3,000 building excess and $1,000 contents excess are on the higher side and will have helped reduce the headline premium. If you'd prefer lower out-of-pocket costs at claim time, adjusting the excess downward would likely push the annual premium up.

---

How Pottsville Compares

To put this quote in proper perspective, here's how Pottsville stacks up against broader benchmarks:

| Benchmark | Average Premium |

|---|---|

| Pottsville (suburb average) | $2,924/yr |

| Pottsville (suburb median) | $2,953/yr |

| NSW state average | $3,801/yr |

| NSW state median | $3,410/yr |

| National average | $2,965/yr |

| National median | $2,716/yr |

| Tweed LGA average | $4,680/yr |

A few things stand out here. First, the Tweed LGA average of $4,680/yr is significantly higher than the Pottsville suburb average — suggesting that other parts of the Tweed region (which includes areas with greater flood and storm exposure) are pulling that LGA figure upward. Pottsville itself appears to be a relatively more affordable pocket within the LGA.

Second, while Pottsville's suburb average sits close to the national average of $2,965/yr, NSW as a whole runs notably higher at $3,801/yr. This reflects the elevated risk profile of many NSW postcodes, including coastal and flood-prone areas across the state.

The sample size for Pottsville is 45 quotes — a reasonable dataset that gives us reasonable confidence in these local figures, though it's always worth shopping around to find where your specific property sits.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct influence on what insurers charge. Here's how the key features play out:

Brick Veneer Walls & Tiled Roof This is a favourable combination from an insurer's perspective. Brick veneer is considered a resilient external wall material, offering good resistance to fire and general wear. Tiled roofs are similarly well-regarded — more durable than Colorbond in some hail scenarios, and a standard feature on quality NSW homes. Together, these materials typically attract more competitive premiums than timber-framed or fibro construction.

Slab Foundation A concrete slab foundation is the norm for homes built in this era and is generally viewed positively by insurers. It reduces the risk of subsidence and pest-related structural damage compared with older raised foundations.

Constructed in 2017 Modern builds benefit from compliance with contemporary building codes, including improved cyclone and wind-load standards, better waterproofing, and updated electrical systems. A 2017 construction date is a genuine pricing advantage — newer homes tend to attract lower premiums than older stock.

Swimming Pool A pool adds to the insured value of the property and introduces some liability considerations, which can nudge premiums upward. Insurers will want to know the pool is fenced to code — a legal requirement in NSW regardless of insurance.

Solar Panels Solar panels are increasingly common on Australian homes, and most insurers now include them under building cover. However, they do add to the replacement cost of the structure, which is reflected in the sum insured. At $707,000, the building cover here appears to account for this.

Ducted Climate Control Ducted air conditioning systems are a significant fixed asset — they're expensive to repair or replace and are typically covered under building insurance. Their inclusion supports the higher sum insured and is a reasonable factor in the overall premium.

214 sqm Floor Area At 214 square metres, this is a sizeable family home. Larger homes cost more to rebuild, which directly influences the sum insured and, in turn, the premium.

---

Tips for Homeowners in Pottsville

1. Review your sum insured annually Building costs in coastal NSW have risen considerably in recent years. Make sure your $707,000 sum insured still reflects the actual cost of rebuilding your home — not just its market value. Underinsurance is one of the most common and costly mistakes homeowners make.

2. Consider your excess carefully This policy carries a $3,000 building excess and a $1,000 contents excess. While higher excesses reduce your premium, they mean more out of pocket if you need to claim. Think about what you could comfortably afford in the event of a storm or accidental damage event, and adjust accordingly.

3. Don't overlook flood cover Parts of the Tweed region have flood exposure, and while Pottsville's coastal position is different from riverine flood zones, it's worth confirming whether your policy includes flood cover — and understanding exactly what it covers. This is especially relevant given the LGA's elevated average premiums, which partly reflect flood risk in the broader area.

4. Shop around at renewal time Loyalty doesn't always pay in insurance. Insurers often offer sharper pricing to new customers, so comparing quotes annually — particularly around renewal — can yield real savings. With a spread of $1,491 to $4,066 in Pottsville alone, there's clearly a wide range of pricing in the market for similar properties.

---

Compare Your Home Insurance with CoverClub

Whether you're renewing your policy or buying cover for the first time, it pays to know where your quote stands. CoverClub makes it easy to benchmark your premium against real data from your suburb, state, and across Australia. Get a quote today at CoverClub and find out if you're getting a fair deal — or if there's a better option waiting for you.