If you own a free standing home in Proston, QLD 4613, you've probably noticed that home insurance premiums in regional Queensland can vary enormously — and not always in ways that feel fair. This article breaks down a real building insurance quote for a three-bedroom, weatherboard home in Proston, compares it against local, state, and national benchmarks, and offers practical advice for homeowners looking to get better value from their cover.

---

Is This Quote Fair?

The quote in question comes in at $3,110 per year (or $298 per month) for building-only cover with a sum insured of $606,000 and a standard $500 building excess. Our analysis rates this quote as EXPENSIVE — above the suburb average.

To put that in perspective:

- The suburb average for Proston is $2,280/yr

- The suburb median sits at $2,004/yr

- The 75th percentile — meaning 75% of quotes in the area are cheaper — is just $2,283/yr

At $3,110, this quote is sitting well above the 75th percentile for the suburb. That means roughly fewer than 1 in 4 comparable quotes in Proston come in this high. While no two properties are identical, that gap is significant enough to warrant a closer look at what's driving the cost — and whether shopping around could yield meaningful savings.

---

How Proston Compares

Understanding where Proston sits in the broader insurance landscape helps put this quote in context. You can explore the full data on our Proston suburb stats page.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Proston (suburb) | $2,280/yr | $2,004/yr |

| South Burnett LGA | $2,940/yr | — |

| Queensland | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. First, Proston's suburb average of $2,280 is actually well below both the Queensland average and the national average — a reflection of the area's relatively lower cyclone risk, moderate flood exposure, and lower property values compared to coastal Queensland. You can dig into Queensland-wide insurance data or national comparisons to see just how wide that spread can be across the state.

The South Burnett LGA average of $2,940 sits closer to this particular quote, suggesting that while Proston itself trends cheaper, some properties in the broader region attract higher premiums based on individual risk factors.

What's notable is that the Queensland state average of $9,129 is dramatically inflated by high-risk coastal and cyclone-prone areas like Cairns, Townsville, and the Whitsundays. The median of $3,903 is a more useful reference point for inland Queensland towns like Proston — and even against that benchmark, the $3,110 quote is competitive, sitting below the state median.

---

Property Features That Affect Your Premium

Several characteristics of this property are likely influencing the premium, both upward and downward.

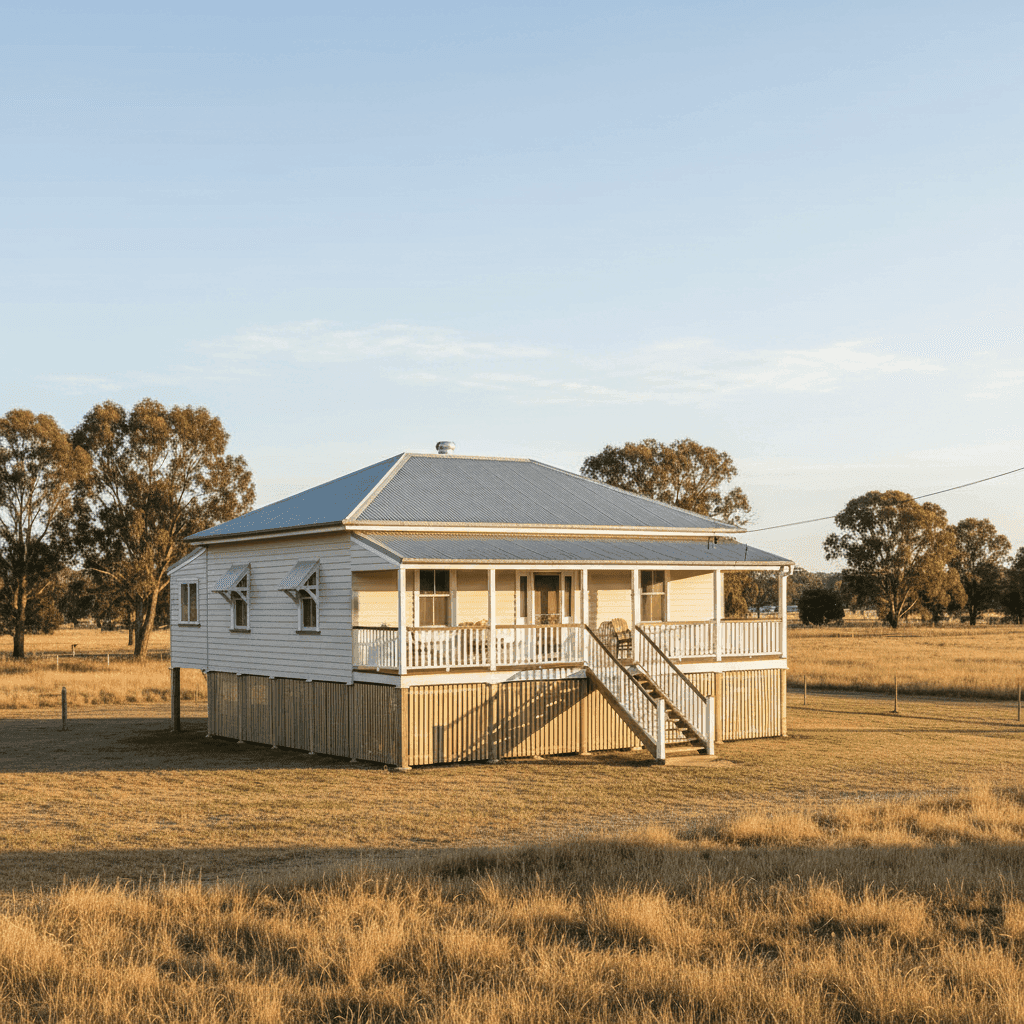

Weatherboard Timber Walls

Weatherboard construction is one of the most common wall types in older Queensland homes, but insurers tend to view it with some caution. Timber is more susceptible to fire, rot, and termite damage than brick or fibre cement, which can push premiums higher. Maintaining your weatherboards — keeping them painted, sealed, and free of pest damage — is not just good housekeeping; it can also support your claim eligibility.

Elevated on Stumps (At Least 1 Metre)

Being elevated by at least one metre is a genuine advantage in flood-prone inland Queensland. Homes on stumps allow floodwater to pass beneath the structure rather than inundating the living areas, which reduces the insurer's risk exposure. This feature may be partially offsetting what could otherwise be a higher premium.

Steel / Colorbond Roof

A Colorbond steel roof is generally viewed favourably by insurers. It's durable, fire-resistant, and holds up well in hail events — all of which reduce the likelihood of a costly claim. This is a positive factor for this property.

Construction Year: 1956

Older homes built before modern building codes can attract higher premiums. A 1956 build may have aging electrical wiring, older plumbing, and structural elements that don't meet contemporary standards. Insurers factor in the increased likelihood of maintenance-related claims for properties of this age.

Timber / Laminate Flooring

Timber flooring in an elevated home can be expensive to repair or replace following water ingress or structural movement. With a $606,000 sum insured, it's worth ensuring that figure accurately reflects the full cost of rebuilding — including flooring, fixtures, and the elevated subfloor structure.

Ducted Climate Control

The presence of ducted climate control adds to the replacement value of the home and is likely factored into the sum insured. This is a relatively modest premium driver but worth noting.

---

Tips for Homeowners in Proston

1. Shop Around — Seriously

With this quote sitting above the suburb's 75th percentile, there's a real chance you could find comparable cover for less. Insurers price risk differently, and a property with weatherboard walls and a 1956 build date will be assessed very differently across providers. Get a new quote at CoverClub to see what else is available for your address.

2. Review Your Sum Insured

At $606,000 for a 130 sqm home, the sum insured works out to roughly $4,660 per square metre — which is on the higher end for a standard-fit home in regional Queensland. Make sure your sum insured reflects the actual cost to rebuild (not the market value), including demolition, site clearance, and elevated subfloor reconstruction. Overinsuring unnecessarily inflates your premium.

3. Ask About Discounts for Home Maintenance

Some insurers offer discounts or more favourable underwriting for homes with recent roof replacements, updated electrical systems, or pest inspections. Given the age of this property, having documented evidence of recent maintenance work could make a difference when negotiating or renewing.

4. Consider Your Excess

This policy carries a $500 building excess, which is relatively low. Opting for a higher voluntary excess — say $1,000 or $2,000 — can meaningfully reduce your annual premium. If you have the savings buffer to cover a larger out-of-pocket cost in a claim, this trade-off often makes financial sense.

---

Find a Better Deal with CoverClub

Whether you're renewing your policy or buying cover for the first time, comparing quotes is the single most effective way to avoid overpaying. CoverClub makes it easy to see what multiple insurers would charge for your specific property in Proston — no obligation, no lengthy phone calls. Start your free quote comparison today and find out if you can do better than $3,110 a year.