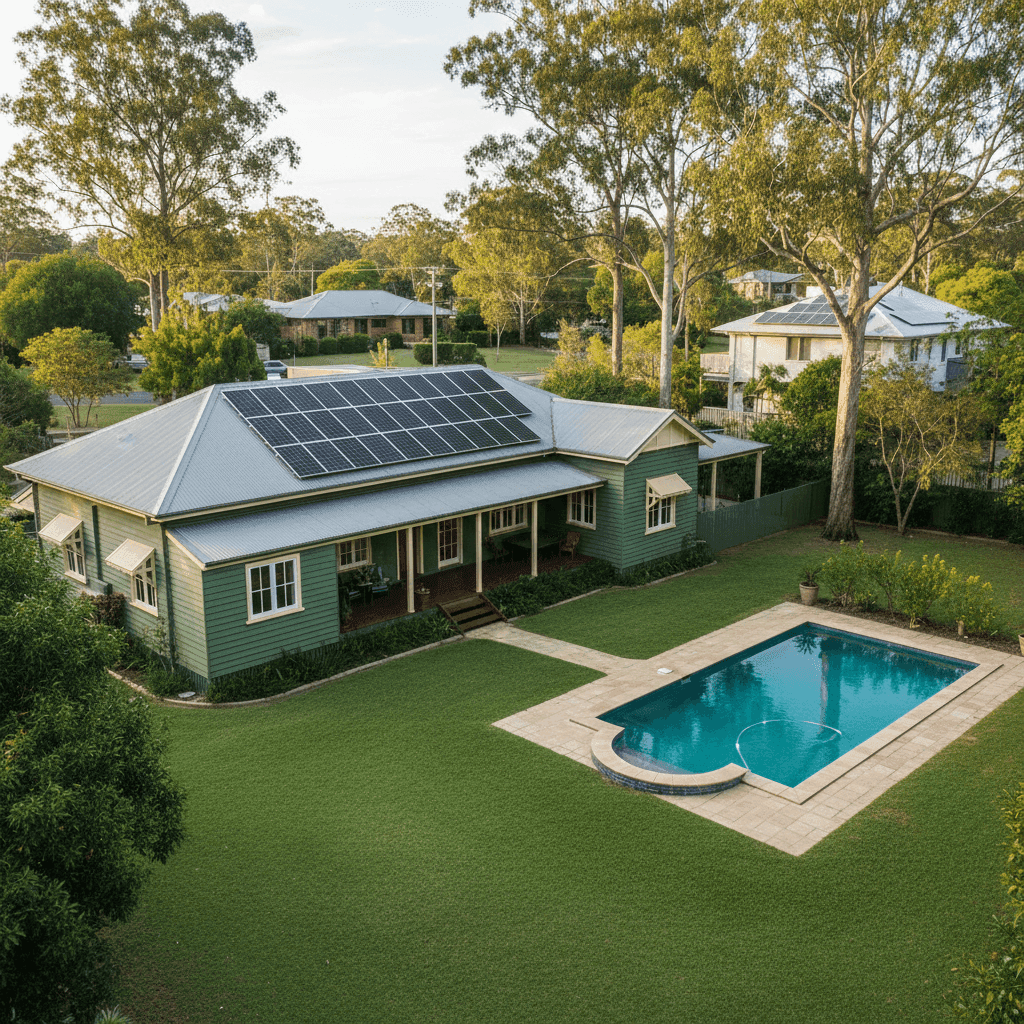

Pullenvale is one of Brisbane's most sought-after semi-rural suburbs — a leafy pocket of acreage living just 16 kilometres from the CBD. With large block sizes, established homes, and a strong sense of community, it's easy to see why homeowners here invest heavily in their properties. Protecting that investment with the right home and contents insurance is essential, and understanding whether you're paying a fair premium is a great place to start.

This article analyses a recent home and contents insurance quote for a six-bedroom, three-bathroom free standing home in Pullenvale (postcode 4069), comparing it against suburb, state, and national benchmarks to help you make an informed decision.

---

Is This Quote Fair?

The quote in question comes in at $4,335 per year (or $429/month) for a combined home and contents policy, covering a building sum insured of $1,890,000 and $100,000 in contents. Our analysis rates this as CHEAP — below average for the area.

That's a meaningful finding. With a suburb average of $7,094/year and a median of $6,702/year, this quote sits well below what most Pullenvale homeowners are paying for similar cover. In fact, it even falls below the suburb's 25th percentile of $4,877/year — meaning it's cheaper than at least three-quarters of comparable quotes we've seen in this postcode.

For a property of this size and value, landing a premium below the local 25th percentile is genuinely impressive. The building excess is set at $3,000 (higher than the standard $500–$1,000 you might see elsewhere), which does help reduce the annual premium — but even accounting for that, the overall cost represents strong value for a large, well-appointed home.

---

How Pullenvale Compares

To put this quote in proper context, it helps to look at the broader pricing landscape. You can explore the full data on the Pullenvale suburb stats page, but here's a quick summary:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $4,335 |

| Pullenvale Suburb Average | $7,094 |

| Pullenvale Suburb Median | $6,702 |

| Pullenvale 25th Percentile | $4,877 |

| Brisbane LGA Average | $4,485 |

| QLD State Average | $4,547 |

| QLD State Median | $3,931 |

| National Average | $2,965 |

| National Median | $2,716 |

A few things stand out here. Pullenvale premiums are significantly higher than both the Queensland state average and the national average. The suburb average of $7,094/year is nearly 2.4 times the national median — a reflection of the high property values, larger homes, and the unique risk profile of properties in this area.

It's worth noting that our suburb sample is based on 23 quotes, which provides a reasonable snapshot but may not capture every type of property in the area. Acreage properties with high replacement values, pools, and premium finishes naturally push the average up.

The fact that this particular quote tracks closer to the Brisbane LGA average ($4,485) than the Pullenvale suburb average suggests the insurer has priced this property competitively — or that the higher building excess is doing some heavy lifting.

---

Property Features That Affect Your Premium

Every property is different, and insurers weigh up dozens of variables when calculating your premium. Here's how the key features of this home are likely influencing the price:

Weatherboard timber walls are one of the most significant risk factors for insurers. Timber is more susceptible to fire, rot, and termite damage than brick veneer or double brick construction. Homes built with weatherboard cladding typically attract higher premiums, and this property is no exception.

Construction year (1964) adds another layer of complexity. A home built over 60 years ago may have ageing plumbing, electrical systems, and structural elements that increase the likelihood of a claim. Older homes can also be more expensive to repair or rebuild to modern building codes.

Slab foundation is generally viewed favourably by insurers — it's a stable, low-maintenance foundation type that doesn't carry the same subsidence or moisture risks as stumped or suspended timber floors.

Steel/Colorbond roof is a positive for insurers. Colorbond roofing is durable, fire-resistant, and performs well in severe weather events, which is particularly relevant in South East Queensland where storm activity is common.

Swimming pool adds to the insured value of the property and introduces some liability considerations, contributing modestly to the overall premium.

Solar panels are increasingly common in Queensland and are generally included in building cover, though they do add to the overall replacement cost of the home.

Above-average fittings quality means higher rebuild costs if something goes wrong. Kitchens, bathrooms, and fixtures of above-average quality are more expensive to replace, and insurers factor this into the sum insured and premium calculation.

The $1,890,000 building sum insured reflects the combination of a large 354 sqm home, premium finishes, and the cost of rebuilding an older timber property to current standards — all legitimate drivers of a higher-than-average sum insured.

---

Tips for Homeowners in Pullenvale

Whether you're reviewing an existing policy or shopping for new cover, here are four practical tips tailored to homeowners in this part of Brisbane:

- Review your sum insured regularly. Building costs have risen sharply in recent years. A sum insured that was adequate two or three years ago may no longer cover the full cost of rebuilding your home. Use a building cost calculator or speak with a quantity surveyor to verify your coverage amount annually.

- Consider your excess strategy carefully. This quote carries a $3,000 building excess, which is higher than average. A higher excess lowers your premium but means more out-of-pocket costs if you need to make a claim. Make sure the excess is an amount you could comfortably cover in an emergency.

- Protect your timber home proactively. Weatherboard homes benefit from regular maintenance — painting, sealing, and termite inspections can reduce the likelihood of claims and may even be viewed favourably by insurers. Some policies also offer discounts for homes with security systems or fire alarms.

- Don't overlook storm and water damage cover. Pullenvale sits in a region that experiences intense summer storms. Check that your policy explicitly covers storm surge, rainwater ingress, and falling trees — these are among the most common claims in South East Queensland.

---

Compare Your Home Insurance with CoverClub

Whether this quote is the right fit depends on your individual circumstances, risk tolerance, and what's included in the policy fine print. The best way to know if you're getting genuine value is to compare multiple quotes side by side.

Get a home insurance quote at CoverClub and see how your premium stacks up against the market in minutes. With transparent pricing data and suburb-level benchmarks, CoverClub makes it easy to shop smarter for home and contents insurance across Australia.