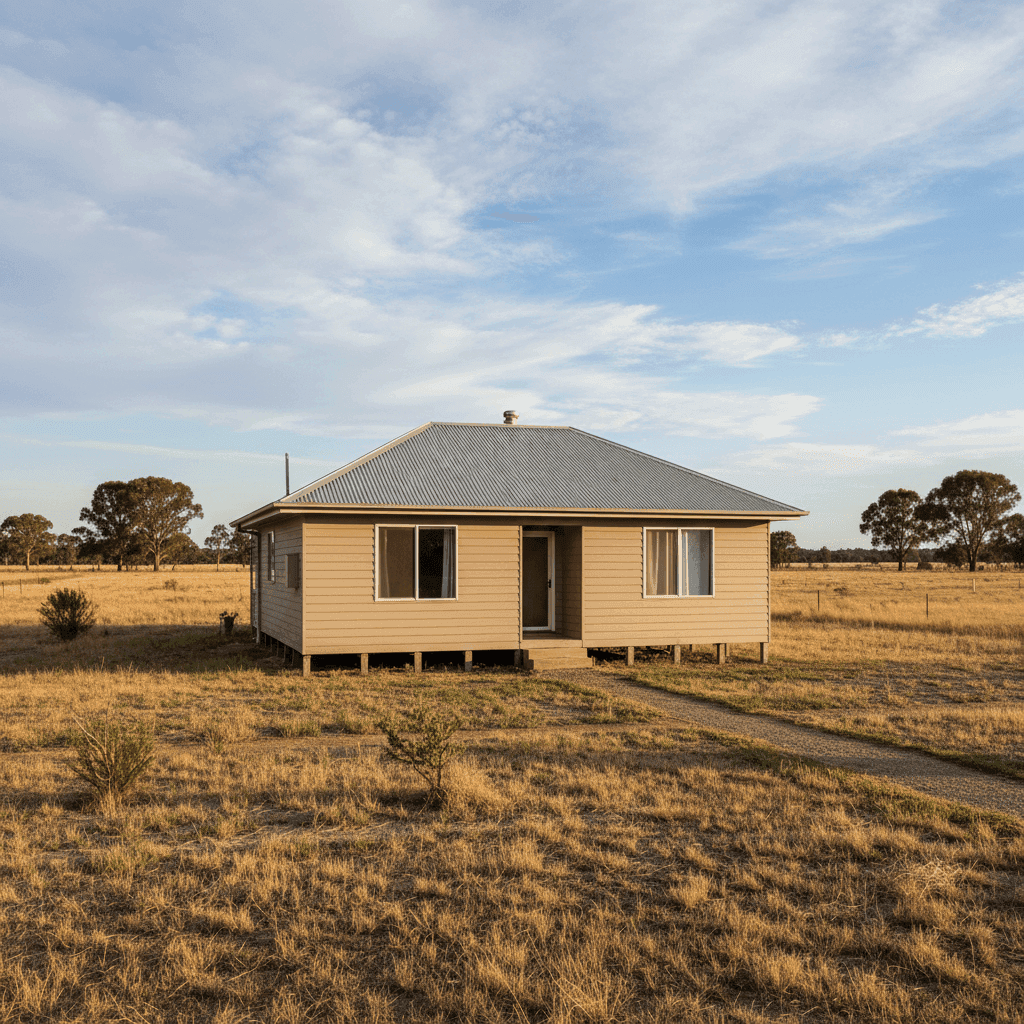

If you own a free standing home in Quambatook, VIC 3540, you've probably noticed that home insurance premiums can vary quite a bit — even within the same postcode. Quambatook is a small agricultural town in the Gannawarra Shire of north-western Victoria, and like many rural communities, it comes with its own unique set of risk factors that insurers weigh carefully. This article breaks down a real home and contents insurance quote for a 3-bedroom, 2-bathroom weatherboard home in the area, and puts the numbers into context so you can make a more informed decision.

---

Is This Quote Fair?

The quote in question comes in at $2,268 per year (or $222/month) for combined home and contents cover, with a building sum insured of $380,000 and contents valued at $20,000. Both the building and contents excess are set at $1,000.

Based on our pricing data, this quote is rated Expensive — above the suburb average. Here's what that means in practice:

- The suburb average for Quambatook is $1,686/yr, and the median sits at $1,746/yr

- This quote is approximately $522 above the suburb average — a difference of roughly 31%

- It also sits above the suburb's 75th percentile of $1,926/yr, meaning it's more expensive than at least three-quarters of comparable quotes in the area

That said, "expensive" is relative. The sum insured here ($380,000 for the building) may be higher than what neighbours are insuring for, which naturally pushes the premium up. Likewise, the age and construction type of the property (more on that below) can cause certain insurers to price more conservatively.

---

How Quambatook Compares

To understand whether this quote is genuinely out of step, it helps to zoom out and look at the broader picture. You can explore the full data on our Quambatook insurance stats page.

| Benchmark | Annual Premium |

|---|---|

| Quambatook suburb average | $1,686 |

| Quambatook suburb median | $1,746 |

| This quote | $2,268 |

| VIC state average | $3,000 |

| VIC state median | $2,718 |

| Gannawarra LGA average | $3,536 |

| National average | $5,347 |

| National median | $2,764 |

Viewed through a state and national lens, this quote actually looks quite reasonable. The Victorian state average sits at $3,000/yr, meaning this quote comes in roughly $732 below the state average. And compared to the national average of $5,347/yr, it's less than half the cost.

The Gannawarra LGA average of $3,536/yr is particularly telling — it suggests that across the broader local government area, insurers are pricing risk at a notably higher level, possibly reflecting flood-prone properties or higher-value homes nearby. By that benchmark, $2,268 is actually on the lower end.

So while this quote is above the local suburb average, it's well within a reasonable range when considered against state and national figures. The 16-quote sample size for Quambatook is relatively small, which means the suburb averages may not fully capture the range of property types and risk profiles in the area.

---

Property Features That Affect Your Premium

Several characteristics of this property are worth understanding from an insurance perspective.

Weatherboard timber construction is one of the most significant factors. Weatherboard homes — particularly those built in 1944 — are more susceptible to fire and general wear than modern brick veneer or double-brick homes. Insurers typically apply a higher risk weighting to timber-framed and timber-clad homes, which contributes to elevated premiums.

The 1944 construction year adds another layer of complexity. Older homes often have ageing electrical wiring, plumbing, and structural components that can increase the likelihood of claims. Rebuilding an older home to current Australian Building Codes can also be significantly more expensive per square metre, which may justify the $380,000 sum insured for a 130 sqm home.

Stump foundations are common in older Victorian homes and can be a flag for some insurers, particularly if the stumps are original timber rather than concrete or steel replacements. Subfloor access issues, pest risk, and potential for movement are all factors that may influence pricing.

Timber and laminate flooring throughout the home is another consideration — these materials can be costly to replace if water damage or fire occurs, and they're factored into the contents and building valuation.

On the positive side, this property has a Colorbond steel roof, which is considered a lower-risk roofing material compared to terracotta tiles or older iron roofing. It's durable, fire-resistant, and less prone to storm damage — factors that work in the homeowner's favour. The absence of a pool and solar panels also simplifies the risk profile and keeps the premium lower than it might otherwise be.

---

Tips for Homeowners in Quambatook

1. Shop around — especially if you're above the suburb average With this quote sitting above the local median, it's worth getting at least two or three competing quotes. Insurers price risk differently, and a property with weatherboard construction and a 1944 build date will be assessed very differently depending on the insurer's underwriting model.

2. Review your sum insured carefully At $380,000 for a 130 sqm home, the building sum insured works out to roughly $2,923/sqm — which is on the higher side, but may be appropriate given the age and construction type. Use a building cost calculator to verify you're not over-insured (which increases premiums unnecessarily) or under-insured (which can leave you significantly out of pocket at claim time).

3. Consider updating high-risk components If your stump foundations are original timber, replacing them with concrete stumps can reduce your risk profile. Similarly, if your home has older wiring (common in pre-1970s homes), having it inspected or upgraded may not only improve safety but could also result in lower premiums over time.

4. Ask about bundling discounts and excess adjustments Increasing your excess from $1,000 to $2,500 can meaningfully reduce your annual premium. If you have a solid emergency fund and are unlikely to make small claims, a higher excess is often a smart trade-off. Also ask your insurer whether bundling home and contents (as this policy does) is delivering the best possible discount.

---

Compare Your Options with CoverClub

Whether you're renewing your policy or shopping for the first time, comparing quotes is the single most effective way to ensure you're not overpaying. CoverClub makes it easy to see how your premium stacks up against others in Quambatook and across Victoria. Get a quote today and find out if there's a better deal waiting for you.