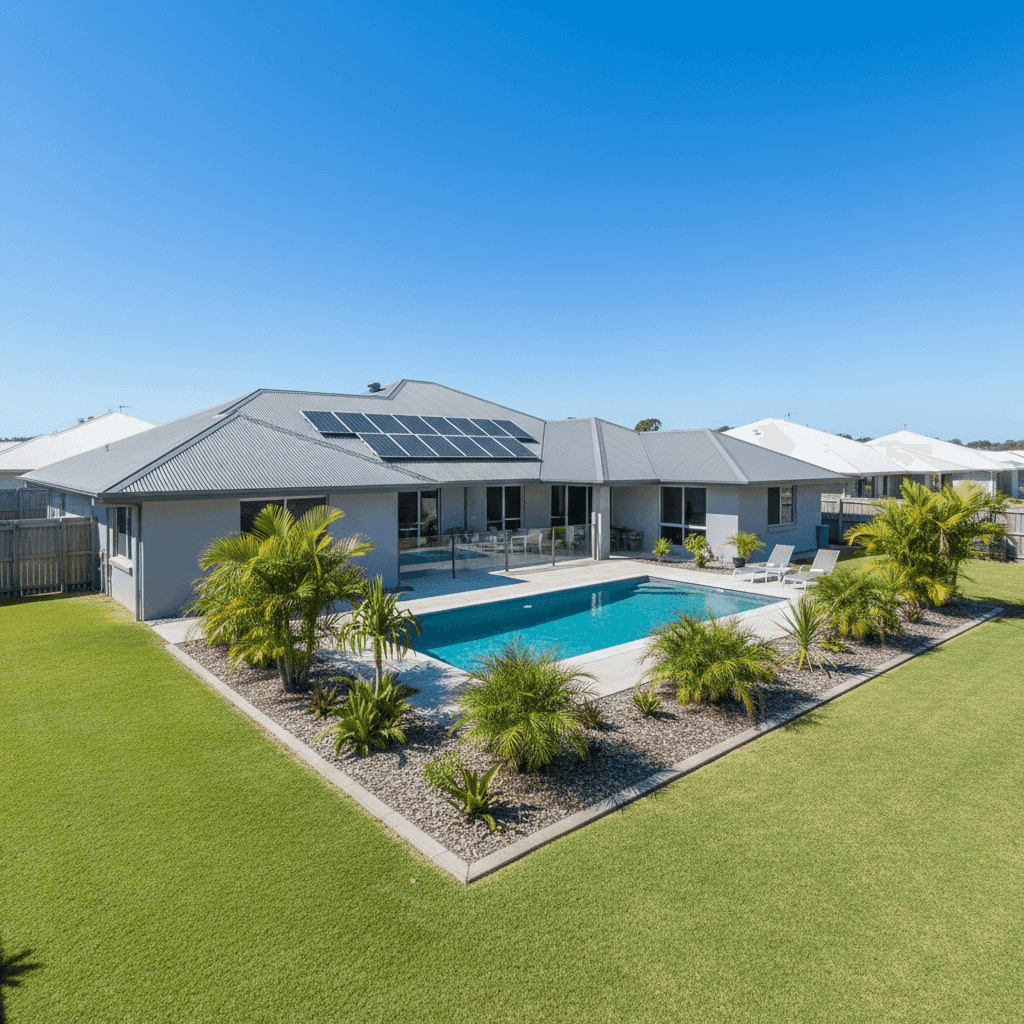

Rangewood is a quiet residential suburb in the Charters Towers region of Queensland, and like much of North Queensland, it comes with its own unique set of insurance considerations. If you own a free standing home here — particularly a larger five-bedroom property — understanding what drives your premium and how it stacks up against the market can save you real money. This article breaks down a recent home and contents insurance quote for a five-bedroom, two-bathroom home in Rangewood (postcode 4817) and puts it in context with suburb, state, and national data.

---

Is This Quote Fair?

The quote in question sits at $5,196 per year (or $471/month) for combined home and contents cover, with a building sum insured of $900,000 and contents valued at $200,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is FAIR — Around Average, and the data backs that up. Within Rangewood itself, the suburb average premium is $4,701/yr and the median sits at $4,160/yr. This quote lands above both of those figures, but it's worth noting that the 75th percentile for the suburb is $5,373/yr — meaning roughly a quarter of comparable quotes in the area cost even more. At $5,196, this premium is comfortably within the upper-middle range, not an outlier.

For a property of this size — 214 sqm, five bedrooms, a pool, and solar panels — a higher-than-median premium is entirely expected. The building sum insured of $900,000 is substantial, and the $200,000 contents figure adds meaningful coverage on top of that. When you factor in the cyclone risk designation for this area (more on that below), the pricing holds up as reasonable.

---

How Rangewood Compares

To truly appreciate where this quote sits, it helps to zoom out and look at the broader picture.

| Benchmark | Premium |

|---|---|

| This Quote | $5,196/yr |

| Rangewood Suburb Average | $4,701/yr |

| Rangewood Suburb Median | $4,160/yr |

| LGA (Charters Towers) Average | $4,457/yr |

| QLD State Average | $9,129/yr |

| QLD State Median | $3,903/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

(Based on 13 quotes sampled in the Rangewood suburb. View full [Rangewood suburb stats](https://coverclub.com.au/stats/QLD/4817/rangewood), [QLD state stats](https://coverclub.com.au/stats/QLD), and [national stats](https://coverclub.com.au/stats/national).)

A few things stand out here. The QLD state average of $9,129/yr is extraordinarily high compared to both the national average and what Rangewood homeowners are actually paying. This is largely driven by high-risk coastal and cyclone-prone postcodes in Far North Queensland, which pull the state average up significantly. The state median of $3,903/yr is a far more representative figure for typical Queensland homeowners, and this quote sits above that — which is appropriate given the property's size and features.

Compared to the national average of $5,347/yr, this quote of $5,196/yr is actually slightly below — a positive sign for Rangewood homeowners. The national median of $2,764/yr reflects how many Australian properties are smaller, lower-risk, or located in less hazard-prone areas, so it's not a meaningful comparison for a large North Queensland home.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on what insurers charge. Understanding them helps you make sense of your quote — and potentially identify areas to improve.

Cyclone Risk Area

This is arguably the single biggest factor. Rangewood falls within a designated cyclone risk zone, and insurers price this in. Policies in cyclone-prone regions of Queensland typically include specific cyclone excess clauses and higher base premiums to account for the elevated risk of wind and storm damage. This is non-negotiable based on geography, but it's important to ensure your policy explicitly covers cyclone damage and that you understand any separate cyclone excess that may apply.

Construction: Concrete Walls & Colorbond Roof

Concrete external walls are generally viewed favourably by insurers — they're fire-resistant, durable, and hold up well in high-wind events. A steel/Colorbond roof is also a solid choice in cyclone-prone areas, as it's lightweight and less likely to cause catastrophic structural failure compared to heavier roofing materials. Together, these construction materials may actually help moderate your premium relative to a timber-framed home.

Slab Foundation

A concrete slab foundation is standard and generally low-risk from an insurer's perspective. It reduces the risk of subsidence and pest-related structural damage, both of which can complicate claims.

Swimming Pool

Pools add to the replacement cost of your property and are factored into the building sum insured. They also introduce a liability consideration. Make sure your policy includes pool-related structures (fencing, pumps, filtration equipment) within the building cover.

Solar Panels

Solar panels are an increasingly common feature and most modern home insurance policies cover them as part of the building. However, it's worth confirming this explicitly with your insurer, as some policies treat panels as a separate item or exclude damage caused by electrical faults in the system.

Timber & Laminate Flooring

While aesthetically appealing, timber and laminate flooring can be more susceptible to water damage than tiles — a relevant consideration in a region that experiences heavy rainfall and cyclone events. Ensuring your policy covers water ingress and flood damage (check whether flood is included or optional) is particularly important here.

---

Tips for Homeowners in Rangewood

1. Check your cyclone excess carefully Many policies in cyclone-prone areas have a separate, higher excess for cyclone-related claims — sometimes 1–2% of the sum insured. On a $900,000 building, that could mean a $9,000–$18,000 out-of-pocket cost before your insurer pays out. Read the Product Disclosure Statement (PDS) closely and compare cyclone excess terms across insurers.

2. Review your building sum insured annually Construction costs in Queensland have risen sharply in recent years. A sum insured of $900,000 for a 214 sqm home may be appropriate today, but it's worth recalculating your rebuild cost each year using a building cost estimator. Being underinsured at claim time can be a costly mistake.

3. Confirm solar panels and pool equipment are covered Ask your insurer specifically whether solar panels are included in the building definition and whether pool equipment (pumps, filters, fencing) is covered. If not, you may need to list these as additional items.

4. Compare quotes before renewal Insurance loyalty rarely pays in Australia. Insurers often offer better rates to new customers, and the market can shift significantly year to year. With the suburb's 25th percentile sitting at $3,614/yr, there may be room to reduce your premium by shopping around — without necessarily sacrificing coverage quality.

---

Ready to Compare?

Whether you're reviewing your current policy or shopping for the first time, comparing multiple quotes is the best way to ensure you're getting value. Get a home insurance quote at CoverClub and see how your options stack up — it takes just a few minutes and could save you hundreds of dollars a year.