Rapid Creek is a well-established suburb sitting just north of Darwin's CBD, known for its relaxed tropical lifestyle, proximity to the waterfront, and a strong community feel. It's also a suburb where home insurance premiums can vary significantly — largely due to the Northern Territory's unique climate risks. If you own a free standing home here, understanding what drives your premium is essential to making sure you're adequately covered without overpaying.

This article breaks down a real home and contents insurance quote for a four-bedroom, two-bathroom free standing home in Rapid Creek (NT 0810), examining whether the price stacks up and what factors are likely shaping it.

---

Is This Quote Fair?

The annual premium for this property comes in at $4,519 per year (or $426/month), covering a building sum insured of $782,000 and contents valued at $151,000, each with a $1,000 excess.

Based on CoverClub's pricing data, this quote is rated CHEAP — below the suburb average. That's genuinely good news for the homeowner. In a cyclone-prone region like Darwin where insurers price risk conservatively, landing a below-average premium on a comprehensive home and contents policy is a meaningful win.

To put it in perspective: the suburb average for Rapid Creek sits at $5,631 per year, with a median of $5,550. Even the 25th percentile — meaning the cheapest quarter of quotes in the area — comes in at $5,261. This quote at $4,519 sits well below all of those benchmarks, suggesting it represents strong value for the coverage on offer.

---

How Rapid Creek Compares

Understanding where your premium sits relative to broader markets helps paint a clearer picture of what you're actually paying for.

| Benchmark | Premium |

|---|---|

| This Quote | $4,519/yr |

| Rapid Creek Suburb Average | $5,631/yr |

| Rapid Creek Suburb Median | $5,550/yr |

| NT State Average | $10,773/yr |

| NT State Median | $3,402/yr |

| Darwin LGA Average | $15,687/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

A few things stand out here. The NT state average of $10,773 is extraordinarily high — more than double this quote — which reflects the extreme variability of premiums across the Territory. Properties in flood plains, remote areas, or higher cyclone-risk zones can attract eye-watering premiums, pulling the state average upward. The Darwin LGA average of $15,687 is particularly striking and likely reflects a mix of high-value properties and elevated risk ratings across parts of greater Darwin.

Compared to the national average of $5,347, this quote also comes in below par, which is notable given the additional cyclone risk that typically pushes NT premiums higher. The national median of $2,764 is lower, but that figure is heavily influenced by lower-risk states like Victoria and South Australia where premiums are far more modest.

In short: for a cyclone-risk suburb in Darwin's northern corridor, this is a competitive result.

---

Property Features That Affect Your Premium

Several characteristics of this property will be influencing the premium — some in the homeowner's favour, others adding to the risk profile that insurers must price.

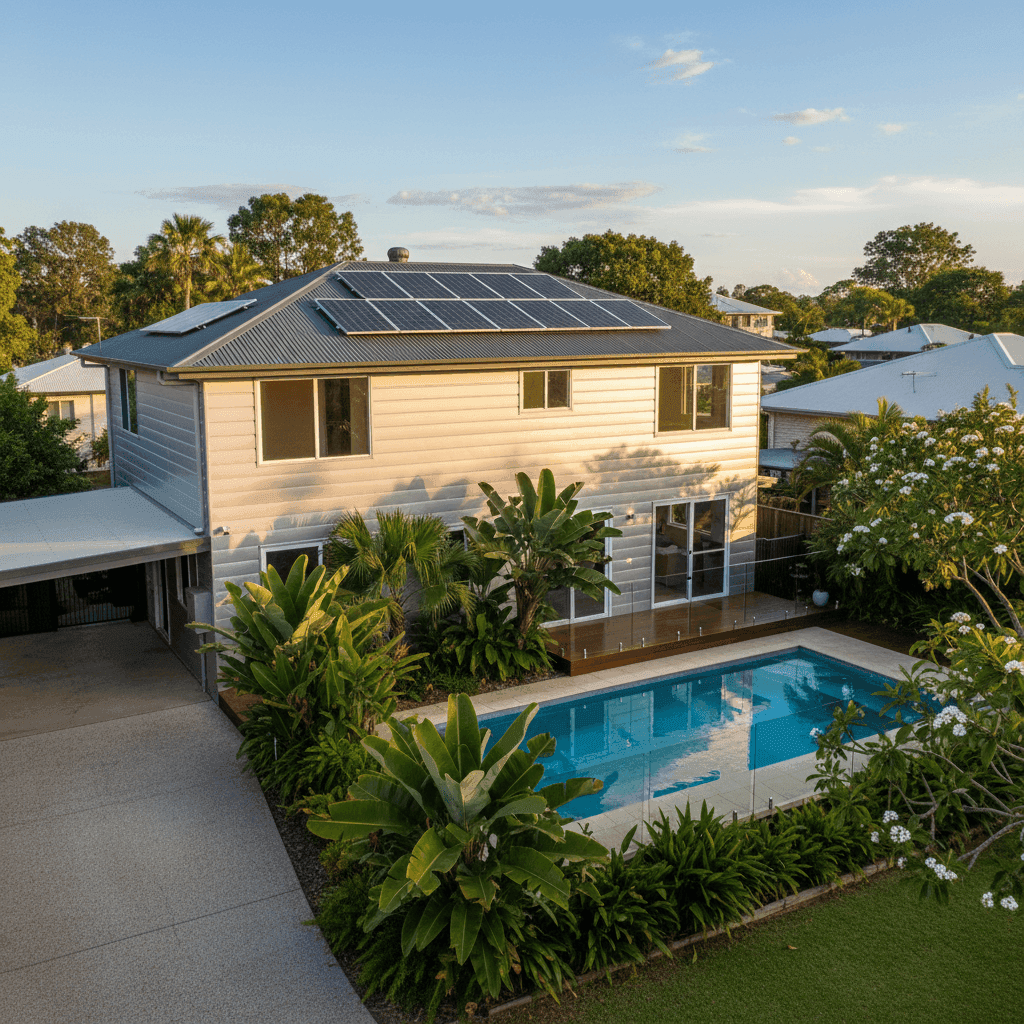

Cyclone Risk Zone This is the most significant factor. Rapid Creek falls within a designated cyclone risk area, and insurers apply specific loading to properties in these zones. Cyclone damage claims can be catastrophic, and the NT has experienced its share of major weather events. Expect this to be a meaningful component of any premium in this suburb.

Construction Type: Aluminium Walls & Colorbond Roof Aluminium-clad external walls and a steel Colorbond roof are actually well-regarded by insurers in tropical climates. Both materials are highly resistant to corrosion, moisture, and wind — all critical in Darwin's wet season. This combination can work in your favour at assessment time compared to, say, weatherboard or rendered brick.

Slab Foundation & Tile Flooring A concrete slab foundation is considered low-risk — there's no underfloor cavity for water or pests to accumulate, and it performs well in high-humidity environments. Tile flooring similarly holds up well in tropical conditions and is less susceptible to water damage than timber or carpet.

Above-Average Fittings Quality The property features above-average fittings, which contributes to the higher building sum insured of $782,000. Quality kitchen and bathroom fixtures, for example, cost more to repair or replace — and insurers factor this into their assessment of replacement cost.

Swimming Pool Pools add a small amount to premiums due to liability considerations and the cost of repair or replacement if damaged. They also need to be specifically noted in your policy to ensure coverage.

Solar Panels Solar panels are increasingly common in Darwin given the abundant sunshine, but they do add to the insurable value of the property. Make sure your building sum insured accounts for the full replacement cost of your solar system — it's a detail that's easy to overlook.

Ducted Climate Control A ducted air conditioning system is a significant fixed asset in the home. Like solar panels, it should be factored into your building sum insured to avoid being underinsured in the event of a major claim.

1980 Construction Homes built in 1980 are now over 40 years old. While this property has clearly been maintained and upgraded (given the above-average fittings), older homes can attract slightly higher premiums due to the age of structural elements, wiring, and plumbing. Some insurers will want to know if major systems have been updated.

---

Tips for Homeowners in Rapid Creek

1. Review Your Building Sum Insured Annually With a sum insured of $782,000, it's important to ensure this figure keeps pace with rising construction costs. Building costs in Darwin have climbed in recent years, and being underinsured — even by 10-15% — can significantly reduce your payout in a total loss scenario. Use a building cost calculator or speak with a local builder to validate your figure each year.

2. Cyclone-Proof Your Property Where Possible Insurers increasingly reward proactive risk mitigation. Securing loose outdoor items, checking roof fixings, and ensuring your home meets current cyclone-rating standards can all support your claim to a competitive premium. Some insurers offer discounts for properties with verified cyclone-rated construction.

3. Don't Underestimate Your Contents At $151,000, the contents value here is reasonable for a four-bedroom home with above-average fittings — but it's worth doing a room-by-room stocktake periodically. Electronics, jewellery, artwork, and outdoor furniture (including pool equipment) all add up quickly. Underinsuring contents is one of the most common mistakes Australian homeowners make.

4. Compare Quotes Before Renewal This quote is already rated below the suburb average, but that doesn't mean it can't be beaten at renewal time. Insurers adjust their risk models regularly, and the competitive landscape shifts. Running a fresh comparison through CoverClub at renewal takes minutes and could save you hundreds of dollars annually.

---

Find Your Best Rate with CoverClub

Whether you're a first-time buyer in Rapid Creek or a long-term homeowner reviewing your coverage, comparing quotes is the single most effective way to ensure you're not overpaying. CoverClub makes it easy to see how your premium stacks up against others in your suburb, your state, and across Australia. Get a quote today and find out if your current insurer is giving you a fair deal — or if it's time to switch.