If you own a four-bedroom free standing home in Rasmussen, QLD 4815, you already know that home insurance in this part of North Queensland isn't cheap. Sitting in the greater Townsville region, Rasmussen sits squarely in a designated cyclone risk zone — and that reality is baked into every premium you'll ever receive. This article breaks down a recent home and contents insurance quote for a property in this suburb, compares it against local, state, and national benchmarks, and offers practical advice for keeping your cover costs manageable.

---

Is This Quote Fair?

The quote in question comes in at $3,966 per year (or $380 per month) for combined home and contents cover, with a building sum insured of $772,000 and contents valued at $76,000. The building excess sits at $2,000 and the contents excess at $1,000.

Our price rating for this quote is Expensive (Above Average) — and the data backs that up. Compared to the suburb average of $3,079 per year and the suburb median of $2,737 per year, this quote is tracking notably higher than what most Rasmussen homeowners are paying. It sits just above the 75th percentile for the suburb ($3,848/yr), meaning roughly three-quarters of comparable quotes in the area come in lower.

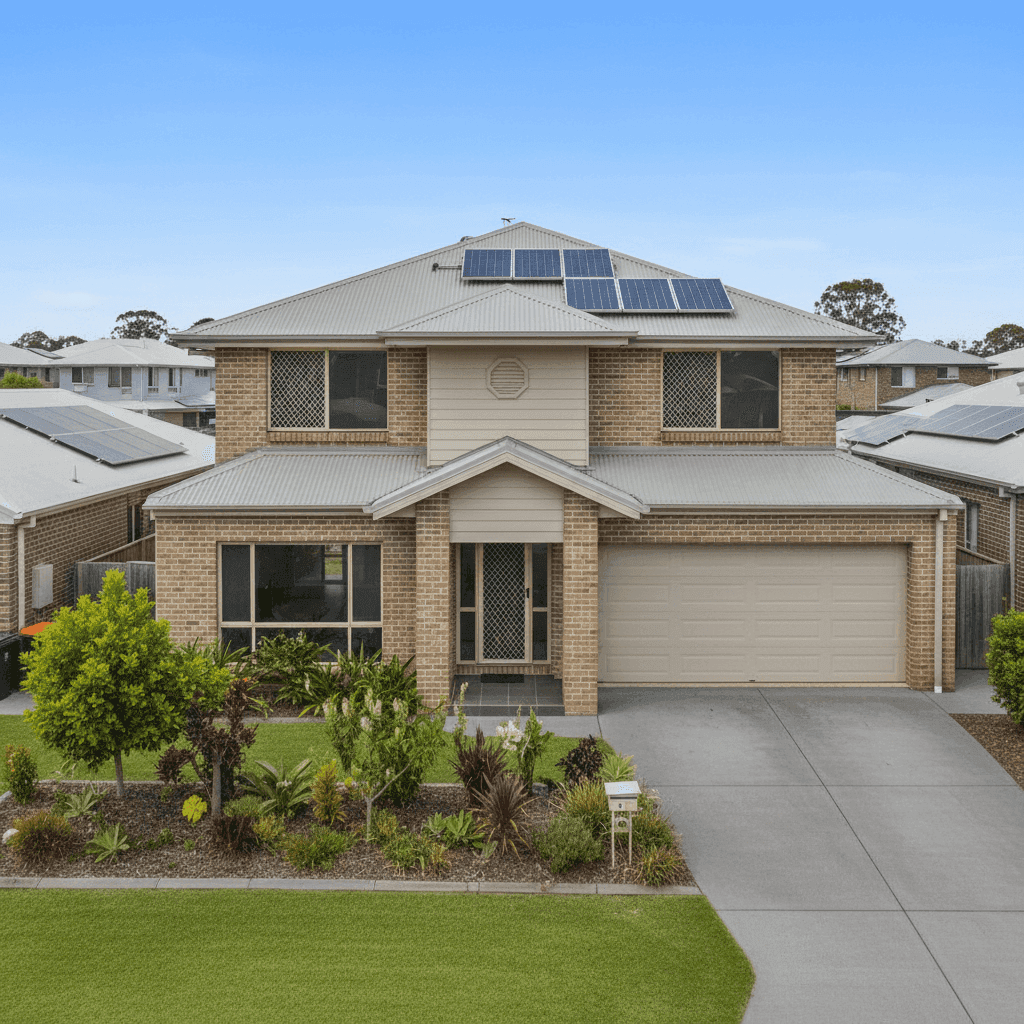

That said, "expensive" is relative. A 214 sqm double brick home with ducted climate control, solar panels, and a Colorbond roof — built in 2000 on a slab foundation — carries a reasonable rebuild cost, and a $772,000 building sum insured reflects that. If the sum insured is accurately calculated, the premium may simply be the market rate for this level of cover in a cyclone-prone postcode. The question worth asking is whether you're getting competitive value, not just whether the number feels high.

---

How Rasmussen Compares

Understanding where this quote sits in the broader landscape helps put the price in perspective. Here's a snapshot:

| Benchmark | Premium |

|---|---|

| This Quote | $3,966/yr |

| Rasmussen Suburb Average | $3,079/yr |

| Rasmussen Suburb Median | $2,737/yr |

| Rasmussen 75th Percentile | $3,848/yr |

| LGA (Townsville) Average | $7,340/yr |

| QLD State Median | $3,903/yr |

| QLD State Average | $9,129/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

A few things stand out here. First, this quote is above the suburb average and median, but it's actually below both the Townsville LGA average ($7,340/yr) and the Queensland state average ($9,129/yr) — which are dramatically elevated by higher-risk and higher-value properties across the region. Second, the QLD state average being so much higher than the median ($9,129 vs $3,903) signals a wide spread of premiums across the state, with some properties paying eye-watering amounts.

Nationally, the picture is similarly skewed: the average ($5,347) is nearly double the median ($2,764), reflecting the outsized influence of high-risk coastal and cyclone-prone areas — exactly the kind of market Rasmussen sits in.

You can explore more local data on the Rasmussen suburb insurance stats page, compare it against the Queensland state overview, or see how it stacks up on the national insurance stats page.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on what insurers charge. Here's how each one plays into the pricing:

Cyclone Risk Zone

This is the single biggest factor. Rasmussen falls within North Queensland's cyclone risk corridor, and insurers apply significant loadings to properties in these postcodes. Cyclone-related damage — from wind, flying debris, and storm surge — is statistically expensive to repair, and premiums reflect that exposure.

Double Brick Construction

Double brick is generally viewed favourably by insurers compared to timber or lightweight cladding. It offers strong resistance to wind and fire damage. In a cyclone zone, however, even solid brick homes aren't immune, so the benefit is relative.

Steel / Colorbond Roof

Colorbond roofing is a popular choice in Queensland for good reason — it's lightweight, durable, and performs well in heat. From an insurance perspective, it's generally considered lower risk than older tile roofs, which can crack or dislodge in high winds.

Slab Foundation

Concrete slab foundations are standard in Queensland and typically don't attract any premium loading. They're considered stable and resistant to subsidence in most conditions.

Solar Panels

Solar panels add replacement value to a property and are typically covered under building insurance. However, they do increase the overall sum insured, which flows through to a slightly higher premium. Make sure your insurer explicitly covers panels — not all policies do by default.

Ducted Climate Control

Ducted air conditioning is a significant fixed asset and is generally included in the building sum insured. It's an expensive item to replace, so its inclusion in the rebuild cost is appropriate and will contribute to the overall premium.

Building Size (214 sqm) and Age (Built 2000)

At 214 sqm, this is a comfortably sized family home. Properties built around 2000 are generally well-regarded by insurers — modern enough to meet cyclone-era building codes introduced in Queensland after Cyclone Tracy, but not so old as to raise concerns about ageing materials or outdated wiring.

---

Tips for Homeowners in Rasmussen

1. Shop Around — Seriously

With only 18 quotes in our suburb sample, the spread between the 25th percentile ($2,092/yr) and the 75th percentile ($3,848/yr) is significant. That's nearly $1,800 per year between the cheapest and most common upper-range quotes. Comparing multiple insurers is one of the most effective ways to reduce your premium without cutting cover.

2. Review Your Sum Insured Annually

Building costs in Queensland have risen sharply in recent years due to labour shortages and materials inflation. Make sure your $772,000 building sum insured reflects current rebuild costs — not what it cost to build in 2000. Underinsurance is a serious risk, particularly after a major weather event when builders are in high demand and prices spike.

3. Consider Your Excess Strategy

This quote carries a $2,000 building excess and a $1,000 contents excess. Opting for a higher excess is one of the most straightforward levers for reducing your annual premium. If you have the financial buffer to cover a larger out-of-pocket cost in the event of a claim, increasing your excess could meaningfully lower what you pay each year.

4. Confirm Solar Panel Cover

With solar panels on the roof, double-check your policy wording to confirm they're explicitly covered for storm, hail, and cyclone damage. Some insurers include them automatically; others require you to list them as a specified item. Given the cost of a full solar system, this is worth a five-minute phone call to your insurer.

---

Ready to Compare?

Whether this quote feels right or you suspect you could be paying less, the best next step is to see what the broader market has to offer. At CoverClub, you can compare home and contents insurance quotes for your Rasmussen property in minutes — helping you make sure you're covered at a price that actually makes sense.